Advanced Driver Assistance Systems (ADAS) Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By System Type (Adaptive Cruise Control, Blind Spot Detection System, Park Assistance, Lane Departure Warning System, Tire Pressure Monitoring System, Autonomous Emergency Braking, Adaptive Front Lights, Others); By Component (Processor, Sensors, Software, Others); By Vehicle Type (Passenger Cars, Commercial Vehicle, Light Commercial Vehicle, Heavy Commercial Vehicle); and Geography

2025-07-15

Automotive & Transportation (Mobility)

Description

ADAS Market Overview

The Global Advanced Driver

Assistance Systems (ADAS) Market is forecasted to grow from USD 33.6 billion in

2025 to USD 77.6 billion by 2033, expanding at a robust CAGR of 11.2% during

the forecast period. This market growth is primarily driven by rising demand

for vehicle safety, driver comfort, and regulatory mandates aimed at reducing

road fatalities.

ADAS technologies such as

adaptive cruise control, automatic emergency braking, lane departure warning,

blind-spot detection, and traffic sign recognition enhance the driving

experience while minimizing the risk of accidents. These systems use a combination

of cameras, radar, ultrasonic sensors, and LiDAR to monitor the environment

around vehicles, enabling semi-autonomous decision-making and improved reaction

times. Key market trends indicate a rapid integration of ADAS features not only

in luxury vehicles but also in mass-market passenger cars and commercial

vehicles. As OEMs respond to evolving NCAP safety ratings and consumer

expectations, the adoption of these technologies is becoming more mainstream.

Additionally, government regulations across North America, Europe, and parts of

Asia are mandating the inclusion of specific ADAS functionalities, which is

further accelerating market penetration. For instance, the European Union now

requires new vehicles to include features like lane-keeping assistance and

advanced emergency braking.

ADAS Market Drivers

and Opportunities

Increasing Regulatory Mandates for Vehicle Safety are anticipated to

lift the ADAS Market during the forecast period

An important driver for vehicular

safety is the strengthening regulatory environment for the global ADAS market.

Governments globally are enacting stringent regulations and safety norms to

reduce road traffic accidents and fatalities. For instance, the European Union

has mandated that each of the new vehicles include safety technologies as

emergency lane-keeping, smart speed assistance, together with advanced

emergency braking from 2022 onwards. Likewise, the United States National

Highway Traffic Safety Administration (NHTSA) still encourages ADAS adoption

using its New Car Assessment Program (NCAP) since such encouragement causes

manufacturers to add advanced safety systems to vehicles. Automakers gain a

competitive advantage through these regulatory frameworks that also set minimum

safety requirements. Automakers are exceeding those requirements for common

ADAS implementation to be encouraged. Based on the presence and performance,

Euro NCAP and ASEAN NCAP increasingly score vehicles as global crash testing

agencies. More features are now being integrated across segments by OEMs. These

features do include lane departure warning and blind-spot detection, and

adaptive cruise control; they are not just for luxury models. Since safety is

now a legal and commercial imperative, regulatory pressure shall continue as a

strong catalyst to promote market expansion, which then ensures further

integration of ADAS technologies in all vehicle types.

Rising Demand for Semi-Autonomous Driving Features Drives Global ADAS

Market

Consumer interest in intelligent

and convenient driving solutions is growing, significantly driving demand for

semi-autonomous features enabled by ADAS. Features such as adaptive cruise

control, lane-keeping assistance, traffic sign recognition, and automated

parking offer enhanced driving comfort while reducing driver fatigue and

errors. These functionalities form the core foundation of Level 1 and Level 2

autonomy, which are rapidly becoming standard in premium as well as mid-range

vehicles. The evolution of ADAS technologies is largely fueled by advancements

in real-time sensor fusion, AI-based decision-making algorithms, and robust

onboard computing power. As consumer lifestyles become increasingly fast-paced

and tech-savvy, expectations around in-vehicle safety, automation, and driver

assistance are also rising. The COVID-19 pandemic further emphasized the need

for contactless and autonomous solutions, which have created long-term

behavioral shifts favoring self-reliant vehicles. Moreover, the integration of

infotainment and safety features through centralized vehicle architecture is

transforming ADAS into a value proposition for both OEMs and end users. As the

automotive sector moves toward full autonomy, ADAS technologies are playing a

critical transitional role by building consumer trust in intelligent systems

while enhancing convenience and safety, thereby driving continued market

adoption.

Opportunity for the ADAS Market

Development of Full-Stack ADAS Platforms for Tier-1 Suppliers and OEMs

is a significant opportunity in the global ADAS Market

There is a growing opportunity

for Tier-1 suppliers and automotive OEMs to develop and offer full-stack ADAS

platforms comprising hardware, software, and cloud-based analytics under one

integrated ecosystem. As vehicles become increasingly software-defined, the

demand for holistic, scalable ADAS solutions is intensifying. OEMs are seeking

partnerships or in-house capabilities to provide seamless integration of

sensors, ECUs, operating systems, and user interfaces. Full-stack ADAS

platforms allow for better system coordination, more accurate data

interpretation, and streamlined deployment across vehicle models. These

platforms also enable over-the-air updates, subscription-based services, and

continuous feature upgrades, opening up new revenue streams. Companies such as

NVIDIA, Mobileye, and Qualcomm are leading examples of tech-driven players

offering end-to-end solutions that can be customized by automakers. This shift

toward platform-based development not only enhances functionality and

efficiency but also accelerates the transition to autonomous driving. The

convergence of software innovation, cloud computing, and vehicle integration

presents a compelling opportunity for market players to expand their value

proposition, build long-term relationships with OEMs, and increase their share

in the fast-growing ADAS ecosystem.

ADAS Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 33.6 Billion |

|

Market Forecast in 2033 |

USD 77.6 Billion |

|

CAGR % 2025-2033 |

11.2% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production Capacity, growth factors and more |

|

Segments Covered |

●

By System Type ●

By Component ●

By Vehicle Type |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

ADAS Market Report Segmentation Analysis

The global ADAS Market industry

analysis is segmented by System Type, Component, Vehicle Type, and by region.

The Adaptive Cruise Control (ACC) segment accounted for the largest

market share in the global ADAS Market

By System Type, the market is

segmented into Adaptive Cruise Control (ACC), Blind Spot Detection System

(BSD), Park Assistance, Lane Departure Warning System (LDWS), Tire Pressure

Monitoring System (TPMS), Autonomous Emergency Braking (AEB), Adaptive Front

Lights (AFL), and Others. In 2025, the Adaptive Cruise Control (ACC) segment

accounted for the largest market share of 25.2% in the global ADAS market. ACC

systems automatically adjust a vehicle's speed to maintain a safe distance from

vehicles ahead, enhancing both safety and driver convenience. With increasing

traffic congestion and growing demand for semi-autonomous features, ACC has

become a core functionality in modern vehicles, especially in mid- to high-end

passenger cars. The integration of radar and camera-based technologies allows

ACC systems to operate efficiently even in complex driving environments.

The Sensors segment holds a major share in the ADAS Market

By Component, the market is

segmented into Processor, Sensors, Radar, LiDAR, Ultrasonic, Software, and

Others. The Sensors segment holds the major share in the global ADAS market.

Sensors are critical enablers of ADAS functionalities, providing real-time data

to monitor vehicle surroundings, detect obstacles, and ensure timely system

responses. This segment includes a wide range of sensors, such as cameras,

radar, ultrasonic, and LiDAR sensors, which collectively enable features like

automatic braking, lane assistance, blind spot detection, and pedestrian

recognition. The increasing sophistication and affordability of sensor

technologies, coupled with innovations in miniaturization and performance

accuracy, have made it feasible to integrate multiple sensors even in mid-range

vehicles.

The Passenger Cars vehicle type segment dominates in the ADAS Market

By Vehicle Type, the market is

segmented into Passenger Cars and Commercial Vehicles. The Passenger Cars

segment dominates the global ADAS market, accounting for the largest share due

to the high production volume, fast-paced adoption of new technologies, and

increasing consumer demand for enhanced safety and comfort features. ADAS

functionalities such as automatic emergency braking, adaptive cruise control,

and lane departure warning are increasingly being integrated as standard or

optional features in compact and mid-size passenger vehicles. As consumers

prioritize safety, OEMs are under growing pressure to include these features

even in entry-level models.

The

following segments are part of an in-depth analysis of the global ADAS market:

|

Market Segments |

|

|

By System Type |

●

Adaptive Cruise

Control (ACC) ●

Blind Spot Detection

System (BSD) ●

Park Assistance ●

Lane Departure

Warning System (LDWS) ●

Tire Pressure

Monitoring System (TPMS) ●

Autonomous Emergency

Braking (AEB) ●

Adaptive Front

Lights (AFL) ●

Others |

|

By Component |

●

Processor ●

Sensors o

Radar o

LiDAR o

Ultrasonic o

Others ●

Software ●

Others |

|

By Vehicle Type |

●

Passenger Cars ●

Commercial Vehicle o Light Commercial Vehicle o

Heavy Commercial

Vehicle |

Advanced Driver

Assistance Systems (ADAS) Market Share Analysis by Region

The North America region is projected to hold the largest share of the

global ADAS Market over the forecast period.

North America accounted for the

largest share of 40.4% in the global Advanced Driver Assistance Systems (ADAS)

market in 2025, firmly establishing its position as the leading regional

market. This dominance is primarily driven by the early adoption of vehicle

safety technologies, stringent automotive safety regulations, and strong

consumer demand for advanced features in both luxury and mainstream vehicles.

Regulatory bodies such as the National Highway Traffic Safety Administration

(NHTSA) and the Insurance Institute for Highway Safety (IIHS) have played a

crucial role in mandating the integration of core ADAS features such as lane

departure warning, automatic emergency braking, and blind-spot detection.

Additionally, North America is home to leading automotive OEMs, technology

developers, and Tier 1 suppliers who are investing heavily in next-generation

ADAS platforms, further strengthening regional innovation and

commercialization. The rising penetration of electric vehicles and the

development of smart city infrastructure also support the integration of ADAS

technologies in both passenger and commercial vehicles. Moreover, high consumer

awareness, favorable insurance incentives, and the presence of a

well-established aftermarket ecosystem contribute to the sustained demand for

ADAS across the region.

In contrast, Asia Pacific is

projected to witness the highest CAGR during the forecast period, driven by

rapid urbanization, increasing vehicle production, and evolving safety

regulations in major countries like China, India, Japan, and South Korea. The region's

growing middle-class population and expanding automotive sector are expected to

fuel significant growth in the adoption of ADAS technologies across both

private and commercial transportation segments.

ADAS Market

Competition Landscape Analysis

The market is

competitive, with several established players and new entrants offering a range

of smart lock products. Some of the key players are Altera Corporation (Intel

Corporation), Continental AG, DENSO CORPORATION, Garmin Ltd., Robert Bosch

GmbH, Valeo SA and others. and others.

Global ADAS Market

Recent Developments News:

- In April 2025, Continental’s Automotive Group Sector announced its

rebranding to ‘Aumovio’ ahead of its planned spin-off and IPO in September

2025. As an independent entity, Aumovio will specialize in cutting-edge

automotive electronics, focusing on autonomous driving, sensor systems,

smart displays, and software-defined vehicle platforms. The company aims

to enhance safety, connectivity, and automated mobility solutions for

next-gen vehicles.

- In April 2025, Mobileye (Israel) joined forces with Valens

Semiconductor (Israel) to develop advanced ADAS connectivity solutions.

Valens’ VA7000 chipsets, compliant with the MIPI A-PHY standard, will

enable high-speed sensor-to-computer communication for Mobileye’s

EyeQ6-based autonomous driving systems. This partnership aims to enhance

real-time data processing and vehicle safety in next-gen ADAS platforms.

- In

April 2025, Valeo (France) partnered with Renault Group (France) to

integrate its Valeo Smart Safety 360 (VSS360) system into the new Renault

Grand Koleos. The turnkey L2/L2+ ADAS solution features a smart front

camera, radars, and AI detection algorithms, offering enhanced driving

safety and automated parking assistance. This collaboration reinforces

Renault’s commitment to advanced driver-assistance technologies.

The Global ADAS Market is dominated by a few large companies, such as

●

Bosch

●

Continental AG

●

ZF Friedrichshafen

●

Valeo

●

Aptiv

●

Denso

●

Magna International

●

Mobileye (Intel)

●

NVIDIA

●

Tesla

●

Harman (Samsung)

●

Hitachi Astemo

●

Autoliv

●

Panasonic

●

Qualcomm

●

Infineon Technologies

●

Texas Instruments

●

Hella

●

Veoneer

●

Waymo

● Other Prominent Players

Frequently Asked Questions

- Global ADAS Market Introduction and Market Overview

- Objectives of the Study

- Global ADAS Market Scope and Market Estimation

- Global ADAS Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global ADAS Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2033

- Market Segmentation

- System Type of Global ADAS Market

- Component of Global ADAS Market

- Vehicle Type Industry of Global ADAS Market

- Region of Global ADAS Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for ADAS Market

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global ADAS Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global ADAS Market Estimates & Forecast Trend Analysis, by System Type

- Global ADAS Market Revenue (US$ Bn) Estimates and Forecasts, by System Type, 2021 - 2033

- Adaptive Cruise Control (ACC)

- Blind Spot Detection System (BSD)

- Park Assistance

- Lane Departure Warning System (LDWS)

- Tire Pressure Monitoring System (TPMS)

- Autonomous Emergency Braking (AEB)

- Adaptive Front Lights (AFL)

- Others

- Global ADAS Market Revenue (US$ Bn) Estimates and Forecasts, by System Type, 2021 - 2033

- Global ADAS Market Estimates & Forecast Trend Analysis, by Component

- Global ADAS Market Revenue (US$ Bn) Estimates and Forecasts, by Component, 2021 - 2033

- Processor

- Sensors

- Radar

- LiDAR

- Ultrasonic

- Others

- Software

- Others

- Global ADAS Market Revenue (US$ Bn) Estimates and Forecasts, by Component, 2021 - 2033

- Global ADAS Market Estimates & Forecast Trend Analysis, by Vehicle Type Industry

- Global ADAS Market Revenue (US$ Bn) Estimates and Forecasts, by Vehicle Type Industry, 2021 - 2033

- Passenger Cars

- Commercial Vehicle

- Light Commercial Vehicle

- Heavy Commercial Vehicle

- Global ADAS Market Revenue (US$ Bn) Estimates and Forecasts, by Vehicle Type Industry, 2021 - 2033

- Global ADAS Market Estimates & Forecast Trend Analysis, by region

- Global ADAS Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global ADAS Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America ADAS Market: Estimates & Forecast Trend Analysis

- North America ADAS Market Assessments & Key Findings

- North America ADAS Market Introduction

- North America ADAS Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By System Type

- By Component

- By Vehicle Type Industry

- By Country

- The U.S.

- Canada

- North America ADAS Market Assessments & Key Findings

- Europe ADAS Market: Estimates & Forecast Trend Analysis

- Europe ADAS Market Assessments & Key Findings

- Europe ADAS Market Introduction

- Europe ADAS Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By System Type

- By Component

- By Vehicle Type Industry

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Switzerland

- Rest of Europe

- Europe ADAS Market Assessments & Key Findings

- Asia Pacific ADAS Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific ADAS Market Introduction

- Asia Pacific ADAS Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By System Type

- By Component

- By Vehicle Type Industry

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa ADAS Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa ADAS Market Introduction

- Middle East & Africa ADAS Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By System Type

- By Component

- By Vehicle Type Industry

- By Country

- South Africa

- UAE

- Saudi Arabia

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America ADAS Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America ADAS Market Introduction

- Latin America ADAS Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By System Type

- By Component

- By Vehicle Type Industry

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global ADAS Market Product Mapping

- Global ADAS Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global ADAS Market Tier Structure Analysis

- Global ADAS Market Concentration & Company Market Shares (%) Analysis, 2023

- Company Profiles

- Bosch

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Bosch

* Similar details would be provided for all the players mentioned below

- Continental AG

- ZF Friedrichshafen

- Valeo

- Aptiv

- Denso

- Magna International

- Mobileye (Intel)

- NVIDIA

- Tesla

- Harman (Samsung)

- Hitachi Astemo

- Autoliv

- Panasonic

- Qualcomm

- Infineon Technologies

- Texas Instruments

- Hella

- Veoneer

- Waymo

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

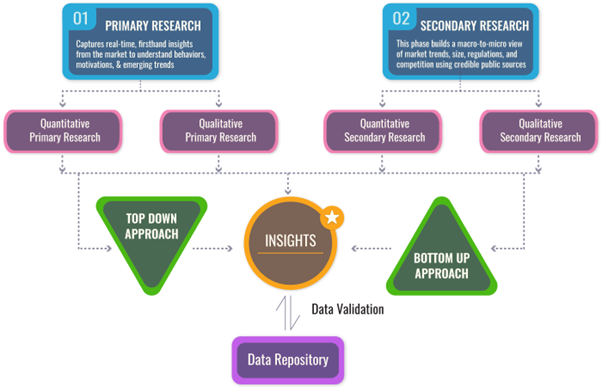

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables