Agricultural Drones Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Offering (Hardware, Software & Services); By Drone Type (Fixed-Wing Drones, Multirotor Drones, Hybrid/Transitional Drones [VTOL]); By Component (Frames and Airframes, Navigation Systems [GPS/GNSS], Cameras and Sensors, Batteries and Power Systems, Autopilot Systems, Others); By Application (Monitoring and Mapping, Precision Farming, Irrigation Management, Crop Health Assessment, Planting and Sowing, Data Collection and Analysis); and Geography

2025-07-15

Agriculture Industry

Description

Agriculture Drones

Market Overview

The Global Agriculture Drones Market is projected to grow significantly from USD 4.9 billion in 2025 to USD 13.2 billion by 2033, expanding at a CAGR of 13.5% during the forecast period. This rapid market expansion is driven by increasing demand for precision agriculture, the need for efficient farm management practices, and the rising global focus on food security.

Agriculture drones are

transforming traditional farming by enabling real-time data collection, crop

monitoring, spraying, seeding, and soil health analysis with greater accuracy

and efficiency. These drones are equipped with high-resolution cameras, multispectral

sensors, GPS modules, and AI-powered analytics platforms that allow farmers to

optimize resources and improve yields, thereby contributing to sustainable

agricultural practices. One of the key market trends fueling growth is the

integration of artificial intelligence and machine learning in drone software,

enabling advanced decision-making and predictive analytics. Additionally,

declining hardware costs, improved battery life, and enhanced drone navigation

technologies are making drones more accessible to small and mid-sized farms,

especially in emerging markets. Governments in countries such as the U.S.,

China, and India are also introducing supportive policies, subsidies, and

training programs to promote the use of unmanned aerial vehicles (UAVs) in

agriculture, which is positively impacting market penetration.

Agriculture Drones

Market Drivers and Opportunities

Rising demand for precision agriculture and farm automation to lift the

agriculture drones market during the forecast period

The increasing need for precision

agriculture is one of the most powerful drivers fueling the growth of the

global agriculture drones market. Precision agriculture focuses on the use of

advanced technologies to optimize crop yields, reduce waste, and ensure

efficient resource management. Drones play a pivotal role in this ecosystem by

enabling real-time crop health monitoring, soil analysis, plant counting, and

irrigation planning. Traditional farming methods are often based on uniform

application of water, fertilizers, and pesticides across large areas, which can

lead to overuse or under-treatment in various zones. Drones equipped with

multispectral and thermal sensors allow farmers to identify variations within a

field and apply inputs precisely where needed. This data-driven approach

improves productivity, lowers costs, and reduces environmental impact. As

global food demand rises and arable land becomes scarce, precision farming

becomes essential. Drones offer scalable and cost-effective solutions to small,

medium, and large-scale farmers alike, further accelerating their adoption. The

integration of AI and analytics platforms also enhances the value of

drone-collected data, allowing predictive decision-making.

Government support and favorable regulatory frameworks drives global

agriculture drones market

Government initiatives and

evolving regulatory frameworks play a critical role in propelling the global

agriculture drones market. Recognizing the transformative potential of drone

technology in boosting agricultural productivity and food security, several

governments have launched supportive policies, pilot programs, and subsidies

aimed at promoting drone adoption. For example, India’s Ministry of Agriculture

offers financial incentives for drone usage in pesticide spraying and crop

monitoring, while the U.S. Federal Aviation Administration (FAA) has

streamlined regulations to allow commercial drone operations under Part 107

rules. Countries like Japan, China, and Brazil have also established frameworks

to facilitate drone use in agriculture, encouraging local drone manufacturing

and skill development. These regulatory advancements not only reduce barriers

to entry but also increase farmer confidence in investing in drone technology.

Furthermore, partnerships between governments, tech firms, and agricultural

institutions are creating ecosystems that foster innovation, training, and

scalable deployment. This proactive regulatory support is instrumental in

integrating drones into mainstream agricultural practices and driving market

growth on a global scale.

Opportunity for the Agriculture Drones Market

Development of Drone-as-a-Service (DaaS) business models is significant

opportunities in the global agriculture drones market

The emergence of

Drone-as-a-Service (DaaS) business models presents a scalable and profitable

opportunity in the agriculture drones market. Not all farmers can afford to

purchase, maintain, or operate sophisticated drone systems—especially in

regions dominated by smallholder farms. DaaS addresses this gap by allowing

farmers to outsource drone-based services such as crop spraying, aerial

mapping, and data analytics to third-party providers on a pay-per-use basis.

This model significantly lowers the entry barrier and makes cutting-edge

technology accessible to a broader base of users. Agricultural service

providers, cooperatives, and startups are increasingly adopting this approach,

offering bundled packages that include drone deployment, data collection, image

processing, and consultation. This trend is particularly promising in

developing countries where capital investment remains a constraint. Moreover,

the DaaS model supports rural employment and skill development by training

local drone operators and technicians. It also opens up recurring revenue

streams for drone manufacturers and software developers, enabling them to scale

more rapidly.

Agriculture Drones Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 4.9 Billion |

|

Market Forecast in 2033 |

USD 13.2 Billion |

|

CAGR % 2025-2033 |

13.5% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production Capacity, growth factors and more |

|

Segments Covered |

●

By Offering ●

By Drone Type ●

By Component ●

By Application |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Agriculture Drones Market Report Segmentation Analysis

The global Agriculture Drones

Market industry analysis is segmented into by Offering, by Drone Type, by

Component, by Application and by region.

The hardware accounted for largest market share in the global

agriculture drones market

By Offering, the market is

segmented into Hardware and Software & Services. The Hardware segment

accounted for the largest market share over 61.2% in the global agriculture

drones market. Hardware components such as drone frames, propulsion systems, GPS

modules, cameras, sensors (multispectral, thermal, LiDAR), and battery systems

are essential to drone functionality and represent the core investment for

agricultural drone applications. The dominance of this segment is driven by the

continuous innovation in drone hardware technologies, which has led to higher

payload capacities, longer flight durations, and greater durability factors

critical to large-scale agricultural operations. As the agriculture industry

increasingly adopts drones for various field applications, the demand for

robust and reliable hardware systems remains a top priority.

The fixed-wing drones segment holds major share in the agriculture

drones market

By Drone Type, the market is

segmented into Fixed-Wing Drones, Multirotor Drones, and Hybrid/Transitional

Drones (VTOL). Among these, the Fixed-Wing Drones segment holds the major share

in the agriculture drones market. Fixed-wing drones are widely preferred in

agriculture due to their ability to cover larger land areas with longer flight

times compared to multirotor drones. They are particularly useful for

large-scale monitoring, mapping, and crop health assessment tasks. These drones

are built for endurance and speed, making them ideal for surveying vast

farmlands and collecting high-resolution imagery in a shorter time.

The Monitoring and mapping segment dominating in agriculture drones

market

By Application, the market is

segmented into Monitoring and Mapping, Precision Farming, Irrigation

Management, Crop Health Assessment, Planting and Sowing, and Data Collection

and Analysis. The Monitoring and Mapping segment dominates the agriculture drones

market, reflecting the critical role drones play in collecting real-time

spatial and visual data of farmland. This application enables farmers to obtain

detailed aerial imagery, topographic information, and vegetation indices, which

are vital for understanding crop performance, identifying stressed areas, and

planning field operations. The demand for high-resolution monitoring tools has

surged as farm owners and agribusinesses prioritize yield optimization and

input cost reduction.

The following segments are part

of an in-depth analysis of the global Agriculture Drones Market:

|

Market Segments |

|

|

By Offering |

●

Hardware ●

Software &

Services |

|

By Drone Type |

●

Fixed-Wing Drones ●

Multirotor Drones ●

Hybrid/Transitional

Drones (VTOL) |

|

By Component |

●

Frames and Airframes ●

Navigation Systems

(GPS/GNSS) ●

Cameras and Sensors ●

Batteries and Power

Systems ●

Autopilot Systems ●

Others |

|

By Application |

●

Monitoring and

Mapping ●

Precision Farming ●

Irrigation

Management ●

Crop Health

Assessment ●

Planting and Sowing ●

Data Collection and

Analysis |

Agriculture Drones

Market Share Analysis by Region

North America region is projected to hold the largest share of the

global agriculture drones market over the forecast period.

North America dominated the

global agriculture drones market with a 36.5% share in 2025, making it the

leading regional market. This dominance is driven by early technological

adoption, highly mechanized farming practices, and strong government and institutional

support for precision agriculture. The region benefits from a mature

agricultural infrastructure, widespread use of advanced farming equipment, and

high awareness of the benefits of drone-based monitoring, mapping, and crop

management. Key countries such as the United States and Canada are investing

heavily in smart farming technologies, including UAV-based solutions that

enhance operational efficiency, reduce input costs, and optimize yield.

Additionally, favorable regulatory frameworks, the presence of major drone

manufacturers, and strong collaborations between agritech startups and research

institutions further boost the region’s market growth. The push toward

sustainable and environmentally responsible farming is also encouraging wider

adoption of drones for targeted pesticide application and resource monitoring,

cementing North America’s leadership in the global agriculture drones

landscape.

Asia Pacific is projected to

register the highest CAGR during the forecast period, fueled by large-scale

agricultural activities, increasing food demand, and growing government support

for digital farming initiatives. Countries like China, India, and Japan are

rapidly deploying drone technology to address labor shortages, improve

productivity, and promote climate-resilient agriculture across diverse

terrains.

Agriculture Drones

Market Competition Landscape Analysis

The market is

competitive, with several established players and new entrants offering a range

of smart lock products. Some of the key players are DJI, XAG, Parrot, AgEagle,

PrecisionHawk, Yamaha Motor, TTA, DroneDeploy, Rantizo, EHang, and others.

Global Agriculture

Drones Market Recent Developments News:

- In September 2024, Trimble Inc. unveiled its

Trimble APX RTX portfolio at INTERGEO 2024, introducing a breakthrough in

direct georeferencing for UAV mapping. The solution leverages Trimble

CenterPoint RTX technology to deliver centimeter-level accuracy without

base stations, streamlining workflows for OEMs and drone payload

integrators. This innovation enhances efficiency while maintaining high

precision in geospatial data collection.

- In April 2024, DJI globally launched its next-gen agricultural

drones—the Agras T50 (for large farms) and compact Agras T25 (for small

fields)—alongside an upgraded SmartFarm app. The T50 boasts improved

stability, payload capacity, and obstacle avoidance, while the T25 offers

portability without sacrificing performance. Both models support fast

charging and precision spraying/spreading. The enhanced SmartFarm app

provides advanced drone fleet management and data analytics, further

solidifying DJI’s leadership in smart farming solutions.

The Global Agriculture Drones Market is dominated by a few large

companies, such as

●

DJI

●

XAG

●

Parrot

●

AgEagle

●

PrecisionHawk

●

Yamaha Motor

●

TTA

●

DroneDeploy

●

Rantizo

●

EHang

●

Trimble

●

Delair

●

Sentera

●

Hylio

●

AeroVironment

● Other Prominent Players

Frequently Asked Questions

- Global Agriculture Drones Market Introduction and Market Overview

- Objectives of the Study

- Global Agriculture Drones Market Scope and Market Estimation

- Global Agriculture Drones Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Agriculture Drones Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2033

- Market Segmentation

- Offering of Global Agriculture Drones Market

- Drone Type of Global Agriculture Drones Market

- Component of Global Agriculture Drones Market

- Application of Global Agriculture Drones Market

- Region of Global Agriculture Drones Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Agriculture Drones Market

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Agriculture Drones Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global Agriculture Drones Market Estimates & Forecast Trend Analysis, by Offering

- Global Agriculture Drones Market Revenue (US$ Bn) Estimates and Forecasts, by Offering, 2021 - 2033

- Hardware

- Software & Services

- Global Agriculture Drones Market Revenue (US$ Bn) Estimates and Forecasts, by Offering, 2021 - 2033

- Global Agriculture Drones Market Estimates & Forecast Trend Analysis, by Drone Type

- Global Agriculture Drones Market Revenue (US$ Bn) Estimates and Forecasts, by Drone Type, 2021 - 2033

- Fixed-Wing Drones

- Multirotor Drones

- Hybrid/Transitional Drones (VTOL)

- Global Agriculture Drones Market Revenue (US$ Bn) Estimates and Forecasts, by Drone Type, 2021 - 2033

- Global Agriculture Drones Market Estimates & Forecast Trend Analysis, by Component

- Global Agriculture Drones Market Revenue (US$ Bn) Estimates and Forecasts, by Component, 2021 - 2033

- Frames and Airframes

- Navigation Systems (GPS/GNSS)

- Cameras and Sensors

- Batteries and Power Systems

- Autopilot Systems

- Others

- Global Agriculture Drones Market Revenue (US$ Bn) Estimates and Forecasts, by Component, 2021 - 2033

- Global Agriculture Drones Market Estimates & Forecast Trend Analysis, by Application

- Global Agriculture Drones Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

- Monitoring and Mapping

- Precision Farming

- Irrigation Management

- Crop Health Assessment

- Planting and Sowing

- Data Collection and Analysis

- Global Agriculture Drones Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

- Global Agriculture Drones Market Estimates & Forecast Trend Analysis, by region

- Global Agriculture Drones Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Agriculture Drones Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America Agriculture Drones Market: Estimates & Forecast Trend Analysis

- North America Agriculture Drones Market Assessments & Key Findings

- North America Agriculture Drones Market Introduction

- North America Agriculture Drones Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Offering

- By Drone Type

- By Component

- By Application

- By Country

- The U.S.

- Canada

- North America Agriculture Drones Market Assessments & Key Findings

- Europe Agriculture Drones Market: Estimates & Forecast Trend Analysis

- Europe Agriculture Drones Market Assessments & Key Findings

- Europe Agriculture Drones Market Introduction

- Europe Agriculture Drones Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Offering

- By Drone Type

- By Component

- By Application

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Switzerland

- Rest of Europe

- Europe Agriculture Drones Market Assessments & Key Findings

- Asia Pacific Agriculture Drones Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Agriculture Drones Market Introduction

- Asia Pacific Agriculture Drones Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Offering

- By Drone Type

- By Component

- By Application

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Agriculture Drones Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Agriculture Drones Market Introduction

- Middle East & Africa Agriculture Drones Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Offering

- By Drone Type

- By Component

- By Application

- By Country

- South Africa

- UAE

- Saudi Arabia

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Agriculture Drones Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Agriculture Drones Market Introduction

- Latin America Agriculture Drones Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Offering

- By Drone Type

- By Component

- By Application

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Agriculture Drones Market Product Mapping

- Global Agriculture Drones Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Agriculture Drones Market Tier Structure Analysis

- Global Agriculture Drones Market Concentration & Company Market Shares (%) Analysis, 2023

- Company Profiles

- DJI

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- DJI

* Similar details would be provided for all the players mentioned below

- XAG

- Parrot

- AgEagle

- PrecisionHawk

- Yamaha Motor

- TTA

- DroneDeploy

- Rantizo

- EHang

- Trimble

- Delair

- Sentera

- Hylio

- AeroVironment

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

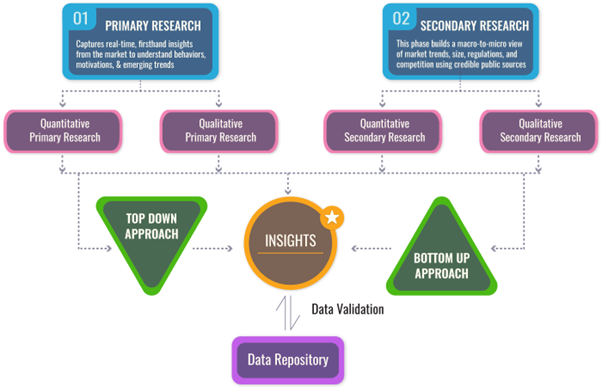

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables