Beverage Packaging Market Size And Forecast (2025 - 2033), Global And Regional Growth, Trend, Share And Industry Analysis Report Coverage: By Product Type (Cans, Bottles & Jars, Pouches, Cartons, Others), By Material (Plastic, Glass, Metal, Other Materials), By Application (Alcoholic Drinks, Non-Alcoholic Drinks) And Geography

2025-07-15

Consumer Products

Description

Beverage Packaging Market Overview

The global Beverage Packaging market is projected to reach US$ 232.8 Billion by 2033 from US$ 140.4 Billion in 2025. The market is expected to register a CAGR of 4.7% from 2025–2033. This growth is driven by rising demand for safe, sustainable, and visually appealing packaging solutions across the food and beverage packaging industry.

Beverage packaging refers to the

various materials and containers used to package liquid refreshments, including

water, soft drinks, alcoholic beverages, dairy products, and functional drinks.

Increasing consumption of ready-to-drink beverages and the rising popularity of

on-the-go packaging formats are significant contributors to this growth. One of

the key drivers fueling the market growth is the increased focus on

sustainability and the growing adoption of eco-friendly and recyclable

materials such as paper-based cartons, bio-based plastics, and lightweight

glass bottles. Global beverage manufacturers are aligning their strategies with

circular economy goals, driving innovations in biodegradable and reusable

packaging solutions. Furthermore, the expansion of e-commerce and

direct-to-consumer delivery channels has intensified the need for durable and

protective packaging, adding momentum to the market's development. The use of

smart packaging technologies such as QR codes and temperature-sensitive labels

is another emerging trend enhancing consumer engagement and product

traceability.

Beverage Packaging Market Drivers and Opportunities

Rising demand for convenient and sustainable packaging solutions is

anticipated to lift the beverage packaging market during the forecast period

One of the primary drivers of

the global beverage packaging market is the growing consumer demand for

convenient and sustainable packaging solutions. With busy lifestyles becoming

the norm across the globe, consumers are increasingly seeking on-the-go beverage

options that are easy to carry, open, and dispose of. This trend has driven

innovation in lightweight, resealable, and single-serve packaging formats.

Moreover, environmental concerns are playing an influential role in packaging

preferences. Consumers and regulatory bodies are pushing brands to adopt

eco-friendly packaging materials such as biodegradable plastics, recycled

content, and plant-based polymers. As a result, manufacturers are investing in

sustainable packaging innovations to maintain brand loyalty and comply with

evolving regulations. Additionally, brand reputation is heavily influenced by

environmental commitments, prompting companies to redesign packaging with

minimal carbon footprints. The shift towards circular economy principles and the

growing adoption of refillable and recyclable packaging systems are further

boosting demand. Beverage companies are also leveraging packaging as a

marketing tool, using design and sustainability claims to influence consumer

purchase decisions. In emerging economies, urbanization and rising disposable

income levels are fostering demand for packaged beverages, further propelling

packaging needs.

Rapid growth of the non-alcoholic beverage segment is a vital driver

for influencing the growth of the global beverage packaging market

The expansion of the

non-alcoholic beverage market, including soft drinks, juices, bottled water,

energy drinks, and ready-to-drink teas and coffees, is significantly driving

the global beverage packaging industry. Health-conscious consumers are increasingly

turning to non-alcoholic alternatives, especially functional beverages enriched

with vitamins, minerals, and probiotics. This shift in consumption patterns has

led to a surge in demand for diverse packaging formats that cater to different

consumer needs. For instance, functional and energy drinks often come in

eye-catching, convenient PET bottles or aluminum cans that provide barrier

protection and enhance shelf appeal. Bottled water, particularly in portable

and premium formats, is experiencing robust growth due to concerns over tap

water quality and the rising trend of hydration. Furthermore, the

ready-to-drink tea and coffee segments are expanding, driven by millennials and

Gen Z consumers who value convenience and healthier alternatives to sugary sodas.

Beverage companies are responding by innovating with packaging that preserves

product freshness, improves usability, and stands out on retail shelves.

Technological advancements in packaging that extend shelf life and support

cold-chain logistics are also enhancing the viability of these products in

global markets

Increasing focus on premium and customized packaging is poised to

create significant opportunities in the global beverage packaging market

The growing consumer preference

for premiumization and personalized experiences is creating substantial

opportunities in the beverage packaging market. In a competitive marketplace,

packaging has evolved from a functional necessity to a critical element of

branding and consumer engagement. Premium packaging characterized by superior

materials, unique shapes, intricate designs, and tactile finishes enhances the

perceived value of beverages and appeals to affluent and quality-conscious

consumers. This trend is particularly prominent in segments such as craft

beverages, wines, spirits, and luxury non-alcoholic drinks. Additionally,

personalized and limited-edition packaging is gaining traction, driven by

advancements in digital printing and design technologies. These innovations

allow for cost-effective production of short runs with custom graphics, names,

or messages, catering to events, holidays, or individual consumer preferences.

Brands are using such packaging strategies to foster emotional connections, encourage

social sharing, and drive brand loyalty. Furthermore, as sustainability

concerns grow, consumers are associating premium packaging with eco-conscious

choices, preferring glass bottles, metal cans, or stylish recyclable

containers. The rise of direct-to-consumer and e-commerce beverage sales is

also amplifying the need for aesthetically appealing and protective packaging.

Beverage Packaging Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 140.4 Billion |

|

Market Forecast in 2033 |

USD 232.8 Billion |

|

CAGR % 2025-2033 |

4.7% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production Capacity, growth factors and more |

|

Segments Covered |

●

By Product Type ●

By Material ●

By Application |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Beverage Packaging Market Report Segmentation Analysis

The Global Beverage Packaging

Market industry analysis is segmented into by Product Type, by Material, by

Application, and by Region.

The bottles & jars segment is anticipated to hold the highest share

of the global beverage packaging market during the projected timeframe

By Product Type, the beverage

packaging market is segmented into Cans, Bottles & Jars, Pouches, Cartons,

and Others. Over the forecast period, the Bottles & Jars category is

expected to have the largest share of the global market, accounting for 39.6%. This dominance is explained by the fact that

bottles and jars are widely used for both alcoholic and non-alcoholic

beverages, particularly in juices, dairy products, bottled water, and

carbonated soft drinks packaging market.

Both producers and customers favor them because of their adaptability,

portability, and capacity to maintain the flavor and freshness of

beverages. PET plastic bottles

predominate in mass-market and convenience beverage formats, but glass bottles

remain preferred in premium beverage categories. Bottles and jars' place in sustainable

packaging trends has been further cemented by advancements in recyclable

materials and lightweight design.

The plastic segment is anticipated to hold the highest share of the

market over the forecast period

By material, the beverage packaging market is segmented into Plastic, Glass, Metal, and Other Materials. The Plastic segment is anticipated to hold the highest share of the market over the forecast period, driven by its cost-effectiveness, lightweight nature, and ease of customization. PET (polyethylene terephthalate) and HDPE (high-density polyethylene) plastics are widely used in beverage packaging for soft drinks, bottled water, and functional beverages due to their durability, clarity, and recyclability. Despite growing environmental concerns, plastic remains a dominant packaging material, especially in regions with high consumption of ready-to-drink and convenience beverages. However, increasing regulatory pressure and consumer demand for sustainable alternatives are prompting innovations in biodegradable and bio-based plastics. The development of recyclable multilayer films and circular economy initiatives is expected to further influence plastic packaging trends.

The Non-alcoholic Drinks segment dominated the market in 2024 and is

predicted to grow at the highest CAGR over the forecast period

By application, the market is

segmented into Alcoholic Drinks and Non-alcoholic Drinks. The Non-alcoholic

Drinks segment dominated the global beverage packaging market in 2024 and is

projected to grow at the highest CAGR over the forecast period. This segment

encompasses carbonated soft drinks, bottled water, juices, dairy beverages,

energy drinks, and functional beverages, which are witnessing rapid consumption

growth globally. The demand for health-focused drinks, sugar-free beverages,

and plant-based alternatives is reshaping the non-alcoholic drinks landscape

and creating new packaging needs. Manufacturers are increasingly adopting

flexible packaging, resealable bottles, and single-serve options to cater to

on-the-go lifestyles and convenience-seeking consumers.

The following segments are part

of an in-depth analysis of the global beverage packaging market:

|

Market Segments |

|

|

By Product Type |

●

Cans ●

Bottles & Jars ●

Pouches ●

Cartons ●

Others |

|

by Material |

●

Plastic ●

Glass ●

Metal ●

Other Materials |

|

by Application |

●

Alcoholic Drinks o

Beer o

Other Alcoholic

Drinks ●

Non-alcoholic Drinks o

Dairy o

Carbonated

Drinks/Soda o

Juices/Soft Drinks o

Bottled Water o

Energy Drinks/RTD

Beverages |

Beverage Packaging Market Share Analysis by Region

North America is projected to hold the largest share of the global

beverage packaging market over the forecast period

North America held the dominant

share of 37.9% in the global beverage packaging market in 2024, and the region

is expected to maintain its lead over the forecast period. This dominance is

primarily attributed to the well-established beverage industry in the U.S. and

Canada, where consumption of both alcoholic and non-alcoholic beverages remains

consistently high. The region's strong preference for packaged bottled water,

energy drinks, carbonated soft drinks, and premium alcoholic beverage packaging

market continues to drive robust demand for innovative and sustainable

packaging solutions. North America is also at the forefront of packaging

innovation, with companies actively adopting eco-friendly materials,

lightweight bottle technologies, and smart packaging for better shelf appeal

and consumer interaction. Additionally, stringent regulatory frameworks

regarding packaging sustainability, along with increasing consumer awareness

about recyclability and environmental impact, are pushing beverage manufacturers

to transition toward greener packaging formats. The high level of automation

and digitization in packaging processes across the region further enhances

production efficiency and supports market growth.

Asia Pacific is projected to

witness the highest CAGR over the forecast period, driven by rapid

urbanization, growing middle-class populations, and changing consumption

patterns in countries such as China, India, Japan, and Southeast Asian nations.

The surge in demand for ready-to-drink beverages, health-focused products, and

premium packaging experiences is transforming the beverage landscape across the

region. Additionally, increasing investments in manufacturing infrastructure

and e-commerce expansion are further boosting the demand for advanced and

efficient beverage packaging solutions in the Asia Pacific. As a result, the

region is expected to emerge as a key growth engine for the global beverage

packaging market.

Beverage Packaging Market Competition Landscape Analysis

The beverage packaging industry

remains highly fragmented, with numerous companies competing across the market.

In recent years, the sector has seen a surge in new product launches, mergers

& acquisitions, and capacity expansions, reflecting its dynamic evolution.

Additionally, rising consumer demand for eco-friendly solutions continues to

drive innovation, pushing brands to adopt greener alternatives. Together, these

factors are reshaping the industry toward greater sustainability and

efficiency.

Global Beverage Packaging Market Recent Developments News:

- In April

2024, Amcor introduced the industry's first 1-liter carbonated soft

drink (CSD) bottle made entirely from 100% post-consumer recycled (PCR)

material, marking a breakthrough in sustainable packaging. This innovation

not only accelerates brands' compliance with recycled-content regulations

but also meets growing consumer demand for eco-friendly solutions while

maintaining production efficiency.

- In October 2023, Coca-Cola

India advanced its sustainability agenda by rolling out 100% recycled PET

(rPET) bottles in 250ml and 750ml sizes for its carbonated beverages. The

initiative supports India’s circular economy objectives, reinforcing

Coca-Cola’s commitment to reducing plastic waste through strategic

partnerships with bottlers and recyclers.

The Global Beverage Packaging

Market is dominated by a few large

companies, such as

●

Amcor plc

●

Glassworks

International

●

Crown Holdings

●

Mondi Group

●

Graham Packaging

Company

●

Sonoco Products

Company

●

Refresco Group

●

Ball Corporation

●

Berry Global Inc.

● Tetra Pak Group

● Others

Frequently Asked Questions

-

Global Beverage Packaging Market Introduction and Market Overview

- Objectives of the Study

- Global Beverage Packaging Market Scope and Market Estimation

- Global Beverage Packaging Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Beverage Packaging Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2033

- Market Segmentation

- Product Type of Global Beverage Packaging Market

- Material of Global Beverage Packaging Market

- Application of Global Beverage Packaging Market

- Region of Global Beverage Packaging Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Beverage Packaging Market

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Beverage Packaging Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global Beverage Packaging Market Estimates & Forecast Trend Analysis, by Product Type

- Global Beverage Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Product Type, 2021 - 2033

- Cans

- Bottles & Jars

- Pouches

- Cartons

- Others

- Global Beverage Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Product Type, 2021 - 2033

- Global Beverage Packaging Market Estimates & Forecast Trend Analysis, by Material

- Global Beverage Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Material, 2021 - 2033

- Plastic

- Glass

- Metal

- Other Materials

- Global Beverage Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Material, 2021 - 2033

- Global Beverage Packaging Market Estimates & Forecast Trend Analysis, by Application

- Global Beverage Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

- Alcoholic Drinks

- Beer

- Other Alcoholic Drinks

- Non-alcoholic Drinks

- Dairy

- Carbonated Drinks/Soda

- Juices/Soft Drinks

- Bottled Water

- Energy Drinks/RTD Beverages

- Alcoholic Drinks

- Global Beverage Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

- Global Beverage Packaging Market Estimates & Forecast Trend Analysis, by region

- Global Beverage Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Beverage Packaging Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America Beverage Packaging Market: Estimates & Forecast Trend Analysis

- North America Beverage Packaging Market Assessments & Key Findings

- North America Beverage Packaging Market Introduction

- North America Beverage Packaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product Type

- By Material

- By Application

- By Country

- The U.S.

- Canada

- North America Beverage Packaging Market Assessments & Key Findings

- Europe Beverage Packaging Market: Estimates & Forecast Trend Analysis

- Europe Beverage Packaging Market Assessments & Key Findings

- Europe Beverage Packaging Market Introduction

- Europe Beverage Packaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product Type

- By Material

- By Application

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Switzerland

- Rest of Europe

- Europe Beverage Packaging Market Assessments & Key Findings

- Asia Pacific Beverage Packaging Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Beverage Packaging Market Introduction

- Asia Pacific Beverage Packaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product Type

- By Material

- By Application

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Beverage Packaging Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Beverage Packaging Market Introduction

- Middle East & Africa Beverage Packaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product Type

- By Material

- By Application

- By Country

- South Africa

- UAE

- Saudi Arabia

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Beverage Packaging Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Beverage Packaging Market Introduction

- Latin America Beverage Packaging Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product Type

- By Material

- By Application

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Beverage Packaging Market Product Mapping

- Global Beverage Packaging Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Beverage Packaging Market Tier Structure Analysis

- Global Beverage Packaging Market Concentration & Company Market Shares (%) Analysis, 2023

- Company Profiles

- Amcor plc

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Amcor plc

* Similar details would be provided for all the players mentioned below

- Glassworks International

- Crown Holdings

- Mondi Group

- Graham Packaging Company

- Sonoco Products Company

- Refresco Group

- Ball Corporation

- Berry Global Inc.

- Tetra Pak Group

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

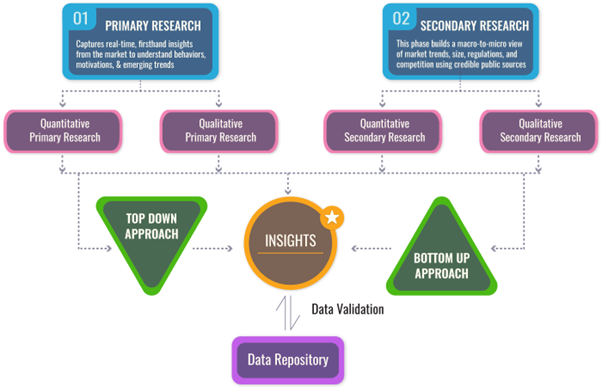

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables