Data Center UPS Market Size And Forecast (2025 - 2033), Global And Regional Growth, Trend, Share And Industry Analysis Report Coverage: By UPS Type (Double Conversion, Line Interactive, Standby) By Tier Type (Tier I, Tier II, Tier III, Tier IV) By Application (Cloud Storage, Enterprise Resource Planning (ERP) System, Data Warehouse, File Servers, Application Servers, Customer Relationship Management (CRM) Systems), By End-User Industry (IT & Telecom, Banking, Financial Services, And Insurance (BFSI), Healthcare, Government, Retail & E-Commerce, Media & Entertainment, Energy & Utilities, Education) And Geography

2025-07-17

Semiconductor and Electronics

Description

Data Center UPS Market Overview

The global Data Center UPS market

is poised for significant expansion over the forecast period, driven by the

surging demand for data storage, cloud computing, and continuous digital

operations across industries. By 2025, the market is projected to reach a value

of around USD 6.2 Billion. Looking ahead to 2033, it is expected to expand

further to about USD 11.0 Billion. This represents an annual growth rate of

7.5% over the ten years.

Data center UPS Systems play a

prominent role in securing continuous performance and protection of servers and

other network resources should an unexpected power outage or power variation

occur. The Data Center UPS Market Growth is being driven by many factors,

including the growth in cloud-based services, increased internet traffic driven

by IoT and AI, and the growth of edge computing networks. Ongoing concerns

regarding the availability of power, integrity, and business continuity require

enterprises to invest in higher levels of UPS systems, including modular and

scalable UPS systems. The market is seeing a trend of more interest in

energy-efficient UPS systems and lithium-ion UPS systems, which offer

additional lifecycle benefits and lower maintenance than traditional battery

technologies. Government regulations regarding data security and the growth of

segments such as BFSI, IT & telecom, healthcare, and manufacturing further

contribute to market expansion.

Data Center UPS Market Drivers and Opportunities

Surge in Data Center Construction and Expansion is anticipated to lift

the Data Center UPS market during the forecast period

The demand for data processing

and storage, driven by massive digital transformation, is spurring the global

growth of data centers. Cloud, edge, big data, and AI technologies are

substantially raising the demand for solid data center infrastructure. With

businesses in various industries extending their digital presence, the

deployment of colocation and hyperscale data centers is gathering momentum.

Data centers need high power availability and uptime, and for this, UPS

solutions are a key factor. UPS solutions help insulate servers and networking

devices from power outages, resulting in unnecessary downtime and lost data at

considerable cost. The trend towards intelligent cities, IoT devices, and 5G

deployment also increases the need for data processing centers, further

propelling the use of UPS. Major players are investing in next-generation UPS

systems with scalable and modular designs, which are more energy-efficient and

space-saving, aligning with evolving data center needs. This continuous

expansion in data centers is forecasted to remain a primary driver for market

growth throughout the forecast period.

Growth in Cloud-Based Services and Colocation Facilities is a vital

driver for influencing the global Data Center UPS Industry market Growth

One major reason for the rise

of more sophisticated UPS systems is the rise of colocation data centers and

the widespread use of cloud services. As enterprises continue to outsource

their data housing, looking to save on infrastructure costs and add agility to

their business, there is an upsurge of cloud data centers and colocation

facilities being created worldwide. These facilities are reliant on a

dependable and redundant UPS infrastructure so they can continue to service

their customers. In addition, cloud service providers are spurring the shift

towards energy-efficient and sustainable solutions, creating a move towards UPS

systems that deliver the best efficiency ratings and are environmentally

friendly. As businesses adopt a hybrid IT infrastructure that consists of

on-premise, cloud, and edge systems, the added complexity of power management

exacerbates the importance of sophisticated UPS systems. The market for UPS

systems that enable these transitions is only going to grow as more companies

migrate to the cloud, providing many opportunities for manufacturers and

service providers.

Innovation in Lithium-ion and Modular UPS Systems is poised to create

significant opportunities in the global Data Center UPS market

The advancement of lithium-ion

batteries and modular designs for UPS systems is expected to fuel growth in the

Data Center UPS Industry. Historically, lead-acid batteries have powered

uninterruptible power supplies, characterized by bulkiness, heavy maintenance

requirements, and operational configuration rigidity. Lithium-ion technology

offers data centers advantages in terms of operating life, footprint, and total

cost of ownership, making it logical that market adoption is accelerating.

Modular UPS systems also permit easy growth of data center capacity; operators

can utilize modular systems to build up capacity in line with increased demand

without requiring major overhauls to their infrastructure. Modular UPS systems

also allow operators to realize increased energy efficiencies and lower costs

of operation, which aligns with the growing emphasis on sustainability in IT

operations. As innovation continues, UPS manufacturers are even beginning to

develop UPSs powered by lithium-ion batteries, with integrated AI-enabled tools

and predictive analytics to enhance reliability and support predictive rather

than reactive maintenance. The move towards smarter, modular, and

energy-efficient UPS systems in the industry will create expansive revenue

opportunities for companies in logistics, particularly in countries that are

currently rapidly evolving their digital and IT infrastructure projects.

Data Center UPS Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 6.2 Billion |

|

Market Forecast in 2033 |

USD 11.0 Billion |

|

CAGR % 2025-2033 |

7.5% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production capacity, growth factors and more |

|

Segments Covered |

●

By UPS Type ●

By Tier Type ●

By Application ●

By End-User Industry |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Data Center UPS Market Report Segmentation Analysis

The global data center UPS market

industry analysis is segmented by UPS type, by tier type, by application, by

end-user industry, and by region.

The Double Conversion segment is anticipated to hold the highest of the

global Data Center UPS market share during the projected timeframe

By UPS Type, the market is

segmented into Double Conversion, Line Interactive, and Standby. The Double

Conversion segment is anticipated to hold the highest share of 44.2% in the

global Data Center UPS market during the projected timeframe. Double conversion

UPS systems offer superior protection by converting incoming AC power to DC and

then back to AC, ensuring a constant, clean, and uninterrupted power supply.

This makes them highly suitable for critical data center environments where

power fluctuations or outages can lead to significant operational and financial

losses. Their ability to isolate sensitive equipment from power anomalies makes

them the preferred choice for large-scale data centers, especially those

supporting cloud services, colocation, and mission-critical workloads. As data

centers continue to scale in capacity and complexity, the demand for reliable

power backup through double conversion systems is expected to drive their

market dominance.

The Tier II segment dominated the market in 2024 and is predicted to

grow at the highest CAGR over the forecast period

By Tier Type, the market is

segmented into Tier I, Tier II, Tier III, and Tier IV. The Tier II segment

dominated the market in 2024 and is predicted to grow at the highest CAGR over

the forecast period. Tier II data centers offer improved redundancy and reliability

over Tier I centers by incorporating components such as redundant capacity

components and a single path for power and cooling distribution. These

facilities strike a balance between cost-efficiency and moderate fault

tolerance, making them attractive to mid-sized enterprises and emerging

markets. The growing need for scalable yet affordable data centers to support

digital services, especially in developing regions, is driving the adoption of

Tier II infrastructures. Moreover, the expansion of edge data centers and

hybrid IT environments is also contributing to the growth of this segment.

The Cloud Storage segment is

predicted to grow at the highest CAGR over the forecast period

By data center UPS market

Application, the market is segmented into Cloud Storage, Enterprise Resource

Planning (ERP) System, Data Warehouse, File Servers, Application Servers, and

Customer Relationship Management (CRM) Systems. The Cloud Storage segment is

predicted to grow at the highest CAGR over the forecast period. As businesses

increasingly migrate workloads to the cloud, there is a soaring demand for

cloud storage infrastructure backed by reliable and uninterrupted power

solutions. UPS systems are essential to prevent data loss, ensure service

continuity, and maintain compliance with data protection standards. The

proliferation of SaaS platforms, IoT data, and real-time analytics has driven

massive growth in storage needs, necessitating large-scale and energy-efficient

UPS systems. This trend, combined with global cloud adoption across industries,

continues to fuel the growth of UPS systems, specifically supporting cloud

storage operations.

The IT & Telecom segment is expected to dominate the market during

the forecast period

By End-User Industry, the market

is segmented into IT & Telecom, Banking, Financial Services, and Insurance

(BFSI), Healthcare, Government, Retail & E-commerce, Media &

Entertainment, Energy & Utilities, and Education. The IT & Telecom

segment is expected to dominate the market during the forecast period. The

ongoing global digitalization and expansion of telecom infrastructure—including

5G rollouts—have exponentially increased data traffic and the need for

high-performance data centers. These facilities require uninterrupted power

supplies to ensure network reliability, service uptime, and data security.

Telecom companies and IT service providers are investing in robust UPS systems

to support their core infrastructure and mitigate the risks associated with

power outages. With the sector increasingly relying on virtualization, AI

workloads, and cloud-based operations, the need for highly efficient, scalable,

and redundant UPS solutions is critical, thereby securing the segment’s

dominant position in the overall market.

The following segments are part

of an in-depth analysis of the global data center UPS market:

|

Market Segments |

|

|

By UPS Type |

●

Double Conversion ●

Line Interactive ●

Standby |

|

By Tier Type |

●

Tier I ●

Tier II ●

Tier III ●

Tier IV |

|

By Application |

●

Cloud Storage ●

Enterprise Resource

Planning (ERP) System ●

Data Warehouse ●

File Servers ●

Application Servers ●

Customer

Relationship Management (CRM) Systems |

|

By End-User Industry |

●

IT & Telecom ●

Banking, Financial

Services, and Insurance (BFSI) ●

Healthcare ●

Government ●

Retail &

E-commerce ●

Media &

Entertainment ●

Energy &

Utilities ●

Education |

Data Center UPS Market Share Analysis by Region

North America is projected to hold the largest share of the global Data

Center UPS market over the forecast period

North America dominated the

global Data Center UPS market in 2024, accounting for a substantial 36.5%

share, and is expected to maintain its leadership throughout the forecast

period. The Data Center UPS Market Region’s dominance is primarily attributed to

the high concentration of data centers, cloud service providers, and hyperscale

facilities across the United States and Canada. The widespread adoption of

digital technologies, combined with the rapid expansion of 5G infrastructure,

AI, and IoT, has significantly increased data processing demands, driving the

need for highly reliable and efficient power backup systems. Moreover, strict

regulatory requirements regarding data integrity and operational continuity,

especially in sectors such as BFSI, healthcare, and government, have further

reinforced the need for advanced UPS systems. The presence of major technology

players, early adoption of innovative UPS architectures, and increased

investments in energy-efficient and modular data center solutions also support

North America's continued dominance in the market.

Meanwhile, the Asia Pacific

region is forecasted to grow at the highest CAGR during the projection period.

This growth is fueled by the rapid digital transformation across emerging

economies like China, India, and Southeast Asian nations, along with rising

investments in cloud computing, e-commerce, and telecommunications. The

increasing number of data centers to meet the region’s expanding online

population and digital economy is driving demand for reliable UPS

infrastructure. Additionally, government-led initiatives supporting

digitalization and smart city developments are expected to accelerate the

adoption of data center UPS solutions in the Asia Pacific region.

Data Center UPS Market Competition Landscape Analysis

The global data center UPS market

is led by key players including Schneider Electric, Eaton, Toshiba, Emerson

Network Power, Clary Corp, Intellipower, GE Electrical Systems, Belkin

International, and Power Innovations International. These industry leaders are

enhancing their competitive positioning through strategic product development,

partnerships, and collaborations to address evolving power protection needs in

data centers worldwide.

Global Data Center UPS Market Recent Developments News:

- December

2023: Eaton introduced its 93T UPS series, delivering reliable power

protection for small data centers and server rooms. The solution supports

mission-critical operations across IT, finance, government, and healthcare

sectors, ensuring uninterrupted power for sensitive applications.

- April 2023: Schneider

Electric unveiled the Easy UPS 3-Phase Modular, featuring Live Swap

capability for seamless maintenance without downtime. The system provides

robust protection for critical loads, enhancing operational resilience in

demanding environments.

The Global Data Center UPS Market is dominated by a few large

companies, such as

●

ABB

●

Schneider Electric

●

Eaton

●

Vertiv Group Corp

●

Mitsubishi Electric

Corporation

●

N1 Critical

Technologies

●

Legrand

●

Delta Electronics,

Inc.

●

Huawei Digital Power

Technologies Co., Ltd.

●

Toshiba Corporation

●

LITE-ON Technology

Corporation

●

Power Innovations

International, Inc.

●

SOCOMEC

●

Borri S.p.A.

●

Fuji Electric Co.,

Ltd.

●

Hitachi Hi-Rel Power

Electronics Private Limited

●

KOHLER Uninterruptible

Power Limited

● Others

Frequently Asked Questions

- Global Data Center UPS Market Introduction and Market Overview

- Objectives of the Study

- Global Data Center UPS Market Scope and Market Estimation

- Global Data Center UPS Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Data Center UPS Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

- Market Segmentation

- UPS Type of Global Data Center UPS Market

- Tier Type of Global Data Center UPS Market

- Application of Global Data Center UPS Market

- End-User Industry of Global Data Center UPS Market

- Region of Global Data Center UPS Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Data Center UPS Market

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Data Center UPS Market Estimates & Historical Trend Analysis (2020 - 2024)

- Global Data Center UPS Market Estimates & Forecast Trend Analysis, by UPS Type

- Global Data Center UPS Market Revenue (US$ Bn) Estimates and Forecasts, by UPS Type, 2020 - 2033

- Double Conversion

- Line Interactive

- Standby

- Global Data Center UPS Market Revenue (US$ Bn) Estimates and Forecasts, by UPS Type, 2020 - 2033

- Global Data Center UPS Market Estimates & Forecast Trend Analysis, by Tier Type

- Global Data Center UPS Market Revenue (US$ Bn) Estimates and Forecasts, by Tier Type, 2020 - 2033

- Tier I

- Tier II

- Tier III

- Tier IV

- Global Data Center UPS Market Revenue (US$ Bn) Estimates and Forecasts, by Tier Type, 2020 - 2033

- Global Data Center UPS Market Estimates & Forecast Trend Analysis, by Application

- Global Data Center UPS Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Cloud Storage

- Enterprise Resource Planning (ERP) System

- Data Warehouse

- File Servers

- Application Servers

- Customer Relationship Management (CRM) Systems

- Global Data Center UPS Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Global Data Center UPS Market Estimates & Forecast Trend Analysis, by End-User Industry

- Global Data Center UPS Market Revenue (US$ Bn) Estimates and Forecasts, by End-User Industry, 2020 - 2033

- IT & Telecom

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare

- Government

- Retail & E-commerce

- Media & Entertainment

- Energy & Utilities

- Education

- Global Data Center UPS Market Revenue (US$ Bn) Estimates and Forecasts, by End-User Industry, 2020 - 2033

- Global Data Center UPS Market Estimates & Forecast Trend Analysis, by Region

- Global Data Center UPS Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Data Center UPS Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

- North America Data Center UPS Market: Estimates & Forecast Trend Analysis

- North America Data Center UPS Market Assessments & Key Findings

- North America Data Center UPS Market Introduction

- North America Data Center UPS Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By UPS Type

- By Tier Type

- By Application

- By End-User Industry

- By Country

- The U.S.

- Canada

- North America Data Center UPS Market Assessments & Key Findings

- Europe Data Center UPS Market: Estimates & Forecast Trend Analysis

- Europe Data Center UPS Market Assessments & Key Findings

- Europe Data Center UPS Market Introduction

- Europe Data Center UPS Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By UPS Type

- By Tier Type

- By Application

- By End-User Industry

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Switzerland

- Rest of Europe

- Europe Data Center UPS Market Assessments & Key Findings

- Asia Pacific Data Center UPS Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Data Center UPS Market Introduction

- Asia Pacific Data Center UPS Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By UPS Type

- By Tier Type

- By Application

- By End-User Industry

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Data Center UPS Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Data Center UPS Market Introduction

- Middle East & Africa Data Center UPS Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By UPS Type

- By Tier Type

- By Application

- By End-User Industry

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Data Center UPS Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Data Center UPS Market Introduction

- Latin America Data Center UPS Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By UPS Type

- By Tier Type

- By Application

- By End-User Industry

- By Country

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Data Center UPS Market Product Mapping

- Global Data Center UPS Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Data Center UPS Market Tier Structure Analysis

- Global Data Center UPS Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- ABB

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- ABB

* Similar details would be provided for all the players mentioned below

- Schneider Electric

- Eaton

- Vertiv Group Corp

- Mitsubishi Electric Corporation

- N1 Critical Technologies

- Legrand

- Delta Electronics, Inc.

- Huawei Digital Power Technologies Co., Ltd.

- Toshiba Corporation

- LITE-ON Technology Corporation

- Power Innovations International, Inc.

- SOCOMEC

- Borri S.p.A.

- Fuji Electric Co., Ltd.

- Hitachi Hi-Rel Power Electronics Private Limited

- KOHLER Uninterruptible Power Limited

- Others

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

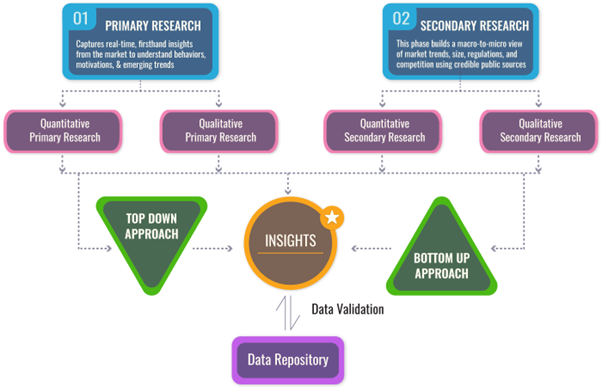

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables