Food Processing Automation Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Type of automation (Semi-automatic and Fully automatic); By component (Plant-level Controls, Measurement & Sensing Devices, Robotics & Mechanical Components and others); Function (Processing, Packaging & Repackaging, Sorting & Grading, Quality Control & Inspection, Palletizing & Depalletizing and Clean-in-Place (CIP)); By Application (Meat, Poultry & Seafood Processing, Bakery & Confectionery, Dairy Products, Beverages, Fruits & Vegetables, Grains & Cereals and Snacks & Convenience Foods); By Distribution Channel (Food Manufacturers, Contract Manufacturers, Industrial Kitchens and Quick Service Restaurants (QSRs)) and Geography

2025-07-15

ICT

Description

Food Processing

Automation Market Overview

The food processing automation

market is anticipated to experience substantial growth from 2025 to 2033,

increase in the adoption of automation technologies in the food and beverage

industry are being a key factor propelling this growth. With an estimated

valuation of approximately USD 12.4 billion in 2025, the market is expected to

reach USD 31.2 billion by 2033, registering a robust compound annual growth

rate (CAGR) of 12.8% over the decade.

Food processing automation

involves the use of advanced technologies and machinery to handle, prepare,

package, and distribute food products with minimal human intervention. This

system integrates robotics, artificial intelligence (AI), sensors, and control

systems to streamline operations, enhance efficiency, and maintain consistent

product quality. Automation is applied across various stages of food

production, including sorting, washing, cutting, cooking, packaging, and

labelling.

One of the primary benefits of

automation in food processing is improved hygiene and food safety, as automated

systems reduce human contact with food. Additionally, automation minimizes

labor costs, increases productivity, and ensures higher precision and

consistency in production. Smart automation systems can also monitor and adjust

processes in real-time, reducing waste and energy consumption.

Industries ranging from dairy and

bakery to meat and beverage production are rapidly adopting automation to meet

growing consumer demands, comply with strict regulations, and stay competitive.

While the initial investment in automation can be high, the long-term savings

and operational improvements justify the cost for many companies. Overall, food

processing automation is transforming the industry by promoting sustainable

practices, enhancing food quality, and enabling scalable production to meet

global food supply needs.

Food Processing

Automation Market Drivers and Opportunities

Rising Labor Costs and Workforce Shortages are anticipated to lift the

Food Processing Automation Market during the forecast period

A primary driver fuelling food

processing automation is the rapid rise in labour costs and widespread

workforce shortages. Manual tasks like sorting, packing, and repetitive

processing are both time-consuming and costly—automated systems can work

continuously without breaks or overtime pay. In many regions, tightening labour

markets and increasing wages push companies toward automation to remain

competitive. Automation not only addresses staffing challenges but also boosts

throughput and reduces per-unit costs, enabling processors to maintain leaner,

more reliable operations. This is a critical advantage as consumer demand for

processed and convenient foods continues to rise, and companies seek scalable

solutions to meet that demand efficiently.

Food Safety, Quality, and Compliance drive the global Food Processing

Automation Market

Stringent food safety regulations

and heightened consumer expectations are accelerating the adoption of

automation for hygiene and quality assurance. Automated systems minimize human

contact, reducing contamination risks and improving traceability. The automation

of inspection and packaging systems ensures consistent standards and

significantly lowers the risk of product recalls. Additionally, machine vision

and sensor technologies can detect foreign objects or product defects in real

time, enhancing quality control far beyond manual capabilities. This shift not

only supports compliance with regulatory standards but also improves consumer

trust and brand reputation through consistent product safety and quality.

Opportunity for the Food Processing Automation Market

AI-Powered Adaptive Processing & Smart Packaging is a significant

opportunity in the global Food Processing Automation Market

A major opportunity in the food

processing automation market lies in the integration of artificial

intelligence, machine learning, and smart packaging technologies. These systems

can adapt in real time to variations in ingredients or environmental conditions,

optimizing production efficiency and reducing waste. Intelligent packaging,

embedded with sensors, can provide real-time data on freshness, temperature,

and traceability, which enhances supply chain transparency and improves

consumer satisfaction. As demand increases for sustainable and personalized

food products, AI-powered solutions offer processors the ability to innovate

while maintaining high efficiency and compliance standards. This creates a

strong competitive advantage in an evolving market.

Food Processing Automation Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 12.4 Billion |

|

Market Forecast in 2033 |

USD 31.2 Billion |

|

CAGR % 2025-2033 |

12.8% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production Capacity, growth factors, and more |

|

Segments Covered |

●

By Type of Automation ●

By Component ●

By Function ●

By Application ●

By End-user |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Food Processing Automation Market Report Segmentation Analysis

The global food processing

automation market industry analysis is segmented into by Type of automation, by

component, by function, by application, by end-user, and by region.

Semi-automatic type of automation segment leading the Food Processing

Automation Market

The semi-automatic automation segment leads the food

processing automation market due to its balance between efficiency and cost.

These systems offer a mix of manual and automated operations, allowing for

greater flexibility and control during production processes. They are

especially popular among small and mid-sized food processing units that cannot

afford or do not require fully automated systems. Semi-automatic systems help

in reducing labour costs while maintaining a level of human oversight, which is

crucial in ensuring product quality in complex food operations. Moreover, they

are relatively easier to maintain and upgrade compared to fully automatic

systems. As companies in developing regions seek to modernize with limited

investment, the demand for semi-automatic solutions continues to grow,

contributing significantly to this segment’s dominance. This setup also helps

companies to gradually transition towards full automation in phases, thereby

aligning with long-term growth strategies without disrupting current workflows.

The Plant-level Controls component segment holds a major share in the

Food Processing Automation Market

Plant-level control systems, such

as SCADA (Supervisory Control and Data Acquisition) and DCS (Distributed

Control Systems), dominate the component segment in the food processing

automation market. These systems play a vital role in monitoring and controlling

entire processing plants from a centralized interface. They ensure that

operations across different departments—like mixing, cooking, and packaging—are

synchronized and optimized. Plant-level controls improve productivity, energy

efficiency, and safety by providing real-time insights and automated responses

to deviations or faults in the system. As food safety standards and regulatory

requirements become more stringent, these systems help companies maintain

compliance by enabling traceability and detailed record-keeping. Additionally,

they support predictive maintenance and reduce unplanned downtimes, which are

critical for maintaining uninterrupted production in food processing. The

growing adoption of Industry 4.0 technologies and the need for smarter manufacturing

processes have further accelerated the demand for advanced plant-level controls

in this sector.

The Food Processing function segment dominates in the Food Processing

Automation Market

The food processing function

segment dominates the food processing automation market due to its critical

role in transforming raw ingredients into finished food products through

various operations such as grinding, mixing, pasteurizing, fermenting, and packaging.

Automation in this segment increases consistency, enhances product quality, and

reduces manual labour requirements. As consumer demand for processed and

packaged food continues to rise globally, especially in urban and fast-paced

environments, manufacturers are compelled to adopt automation to scale

operations efficiently. Furthermore, automation ensures hygiene, minimizes

contamination risks, and aligns with food safety regulations. With advances in

sensor technology, robotics, and AI integration, food processing functions are

becoming increasingly precise and intelligent. This has enabled food processors

to achieve better yields, reduce waste, and improve overall profitability. As a

result, food processing functions represent the most essential and

value-generating stage within the automation ecosystem in the industry, driving

their dominance in the market.

The food manufacturing end-user segment is contributing a major share

to the solar hybrid inverters market

The food manufacturing end-user

segment contributes the major share in the food processing automation market

because it encompasses a wide range of operations from ingredient preparation

to packaging of final food products. Food manufacturers are under constant

pressure to improve productivity, ensure safety, and meet regulatory standards

while reducing operational costs. Automation enables them to streamline these

processes, enhance throughput, and maintain consistent quality across

large-scale operations. Moreover, the rise in demand for packaged,

ready-to-eat, and processed foods has driven manufacturers to invest heavily in

automation to meet market demand efficiently. Automated systems in food

manufacturing also help in maintaining cleanliness and minimizing human

contact, which is crucial in ensuring food safety. Additionally, with growing

competition and the need for innovation in product offerings, manufacturers are

leveraging automation to support flexible production lines that can adapt to

different product types. This makes the food manufacturing segment a key driver

of automation adoption in the industry.

The following segments are part

of an in-depth analysis of the global Food Processing Automation Market:

|

Market Segments |

|

|

By Type of Automation |

●

Semi-automatic ●

Fully automatic |

|

By Component

|

●

Plant-level Controls o PLCs (Programmable Logic Controllers) o SCADA (Supervisory Control and Data Acquisition) o DCS (Distributed Control Systems) o HMI (Human-Machine Interface) ●

Measurement &

Sensing Devices o

Sensors o

Transmitters ●

Robotics &

Mechanical Components o

Industrial Robots o

Actuators o

Motors o

Conveyors ●

Others |

|

By Function |

●

Processing ●

Packaging &

Repackaging ●

Sorting &

Grading ●

Quality Control

& Inspection ●

Palletizing &

Depalletizing ●

Clean-in-Place (CIP) |

|

By Application |

●

Meat, Poultry &

Seafood Processing ●

Bakery &

Confectionery ●

Dairy Products ●

Beverages ●

Fruits &

Vegetables ●

Grains & Cereals ●

Snacks &

Convenience Foods |

|

By End-user |

●

Food Manufacturers ●

Contract

Manufacturers ●

Industrial Kitchens ●

Quick Service

Restaurants (QSRs) |

Food Processing

Automation Market Share Analysis by Region

North America region is projected to hold the largest share of the

global Food Processing Automation Market over the forecast period.

North America is projected to

hold the largest share of the global Food Processing Automation Market over the

forecast period due to its highly advanced food processing industry, strong

technological infrastructure, and growing emphasis on automation. The region is

home to several leading food manufacturers and automation technology providers,

fostering widespread adoption of robotics, AI, and smart control systems across

processing facilities. Additionally, stringent food safety regulations in the

U.S. and Canada drive the need for automated systems that ensure compliance,

traceability, and product consistency. Rising labor costs and workforce

shortages further accelerate the shift toward automation, making it a strategic

investment for operational efficiency and long-term cost savings. Moreover,

North American consumers' demand for packaged, ready-to-eat, and high-quality

food products encourages food companies to embrace automation to meet market

expectations. These factors collectively position North America as the dominant

force in shaping the future of automated food processing worldwide.

Food Processing

Automation Market Competition Landscape Analysis

The market is

competitive, with several established players and new entrants offering a range

of food processing automation products. Some of the key players are ABB Ltd.,

Siemens AG, Rockwell Automation, Inc., Schneider Electric SE, Mitsubishi

Electric Corporation, Yokogawa Electric Corporation, GEA Group AG, Emerson

Electric Co., and others.

Global Food

Processing Automation Market Recent Developments News:

- In May 2025, A new fast‑food concept called Burgerbots in Los Gatos,

California, uses ABB Robotics’ Flexpicker and YuMi robots to fully

assemble burgers in just 27 seconds. The system places patties, toppings,

and buns with speed and consistency, though human staff still handle

service and customer-facing roles.

- In April 2025, Chef Robotics, an AI-driven robotics

startup, raised $20.6 million in Series A funding led by Avataar Ventures,

including an additional $22.5M in equipment financing, bringing the total to $43M. Their

robots, capable of adapting to nearly 2,000 ingredients, collaborate with

human workers in food production plants.

- In February 2025, Sensei Ag, backed by Larry Ellison, aimed to

revolutionize farming via automation, encompassing

robots, AI, and sensors. But on the Hawaiian island of Lanai, their

initiative faced major setbacks: greenhouse failures from climate

incompatibility, solar panel breakdowns, supply issues, and leadership

turnover.

The Global Food Processing Automation Market is dominated by a few

large companies, such as

●

ABB Ltd.

●

Siemens AG

●

Rockwell Automation,

Inc.

●

Schneider Electric SE

●

Mitsubishi Electric

Corporation

●

Yokogawa Electric

Corporation

●

GEA Group AG

●

Emerson Electric Co.

●

FANUC Corporation

●

Yaskawa Electric

Corporation

●

Bosch Packaging

Technology

●

Omron Corporation

●

Tetra Pak

International S.A.

●

Bühler AG

●

Alfa Laval AB

● Other Prominent Players

Frequently Asked Questions

- Global Food Processing Automation Market Introduction and Market Overview

- Objectives of the Study

- Global Food Processing Automation Market Scope and Market Estimation

- Global Food Processing Automation Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Food Processing Automation Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2033

- Market Segmentation

- Type of Automation of Global Food Processing Automation Market

- Component of Global Food Processing Automation Market

- Function of Global Medical Devices Coating Market

- Application of Global Food Processing Automation Market

- End-user of Global Medical Devices Coating Market

- Region of Global Food Processing Automation Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Food Processing Automation Market

- Key Product/Brand Analysis

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Food Processing Automation Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global Food Processing Automation Market Estimates & Forecast Trend Analysis, by Type of Automation

- Global Food Processing Automation Market Revenue (US$ Bn) Estimates and Forecasts, by Type of Automation, 2021 - 2033

- Semi-automatic

- Fully automatic

- Global Food Processing Automation Market Revenue (US$ Bn) Estimates and Forecasts, by Type of Automation, 2021 - 2033

- Global Food Processing Automation Market Estimates & Forecast Trend Analysis, by Component

- Global Food Processing Automation Market Revenue (US$ Bn) Estimates and Forecasts, by Component, 2021 - 2033

- Plant-level Controls

- PLCs (Programmable Logic Controllers)

- SCADA (Supervisory Control and Data Acquisition)

- DCS (Distributed Control Systems)

- HMI (Human-Machine Interface)

- Measurement & Sensing Devices

- Sensors

- Transmitters

- Robotics & Mechanical Components

- Industrial Robots

- Actuators

- Motors

- Conveyors

- Others

- Plant-level Controls

- Global Food Processing Automation Market Revenue (US$ Bn) Estimates and Forecasts, by Component, 2021 - 2033

- Global Food Processing Automation Market Estimates & Forecast Trend Analysis, by Function

- Global Food Processing Automation Market Revenue (US$ Bn) Estimates and Forecasts, by Function, 2021 - 2033

- Processing

- Packaging & Repackaging

- Sorting & Grading

- Quality Control & Inspection

- Palletizing & Depalletizing

- Clean-in-Place (CIP)

- Global Food Processing Automation Market Revenue (US$ Bn) Estimates and Forecasts, by Function, 2021 - 2033

- Global Food Processing Automation Market Estimates & Forecast Trend Analysis, by Application

- Global Food Processing Automation Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

- Meat, Poultry & Seafood Processing

- Bakery & Confectionery

- Dairy Products

- Beverages

- Fruits & Vegetables

- Grains & Cereals

- Snacks & Convenience Foods

- Global Food Processing Automation Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

- Global Food Processing Automation Market Estimates & Forecast Trend Analysis, by End-user

- Global Food Processing Automation Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2021 - 2033

- Food Manufacturers

- Contract Manufacturers

- Industrial Kitchens

- Quick Service Restaurants (QSRs)

- Global Food Processing Automation Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2021 - 2033

- Global Food Processing Automation Market Estimates & Forecast Trend Analysis, by region

- Global Food Processing Automation Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Food Processing Automation Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America Food Processing Automation Market: Estimates & Forecast Trend Analysis

- North America Food Processing Automation Market Assessments & Key Findings

- North America Food Processing Automation Market Introduction

- North America Food Processing Automation Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Type of Automation

- By Component

- By Function

- By Application

- By End-user

- By Country

- The U.S.

- Canada

- North America Food Processing Automation Market Assessments & Key Findings

- Europe Food Processing Automation Market: Estimates & Forecast Trend Analysis

- Europe Food Processing Automation Market Assessments & Key Findings

- Europe Food Processing Automation Market Introduction

- Europe Food Processing Automation Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Type of Automation

- By Component

- By Function

- By Application

- By End-user

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Switzerland

- Rest of Europe

- Europe Food Processing Automation Market Assessments & Key Findings

- Asia Pacific Food Processing Automation Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Food Processing Automation Market Introduction

- Asia Pacific Food Processing Automation Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Type of Automation

- By Component

- By Function

- By Application

- By End-user

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Food Processing Automation Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Food Processing Automation Market Introduction

- Middle East & Africa Food Processing Automation Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Type of Automation

- By Component

- By Function

- By Application

- By End-user

- By Country

- South Africa

- UAE

- Saudi Arabia

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Food Processing Automation Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Food Processing Automation Market Introduction

- Latin America Food Processing Automation Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Type of Automation

- By Component

- By Function

- By Application

- By End-user

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Food Processing Automation Market Product Mapping

- Global Food Processing Automation Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Food Processing Automation Market Tier Structure Analysis

- Global Food Processing Automation Market Concentration & Company Market Shares (%) Analysis, 2023

- Company Profiles

- ABB Ltd.

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- ABB Ltd.

* Similar details would be provided for all the players mentioned below

- Siemens AG

- Rockwell Automation, Inc.

- Schneider Electric SE

- Mitsubishi Electric Corporation

- Yokogawa Electric Corporation

- GEA Group AG

- Emerson Electric Co.

- FANUC Corporation

- Yaskawa Electric Corporation

- Bosch Packaging Technology

- Omron Corporation

- Tetra Pak International S.A.

- Bühler AG

- Alfa Laval AB

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

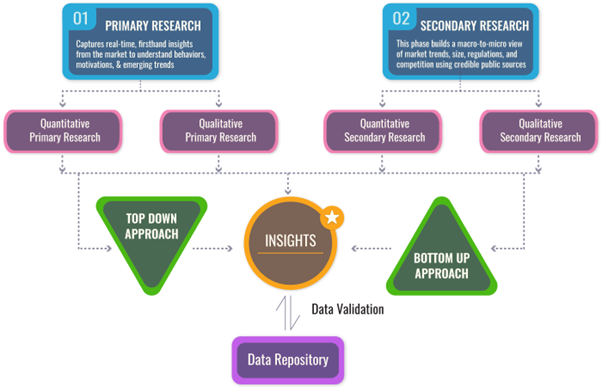

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables