Ammunition Market Size And Forecast (2025 - 2033), Global And Regional Growth, Trend, Share And Industry Analysis Report Coverage: By Caliber (Small, Medium, Large Caliber Ammunition Market), By Components (Fuzes & Primers, Gunpowder, Cases, Projectiles And Warheads, Others), By Products (Bullets, Aerial Bombs, Artillery Shells, Grenades, Mortars, Others), By Application (Military & Homeland Security, Civil & Commercial) And Geography

2025-07-14

Aerospace & Defense

Description

Ammunition Industry Market Overview

The global ammunition market is poised for steady growth, with projections indicating an increase from US$ 21.5 billion in 2025 to US$31.0 billion by 2033, reflecting a compound annual growth rate (CAGR) of 3.4% over the decade. This expansion is fueled by three key factors: rising defense expenditures worldwide, escalating geopolitical conflicts, and heightened demand from civilian and law enforcement agencies for small arms and tactical ammunition. The convergence of these drivers underscores the market's resilience amid global security challenges and evolving threat landscapes.

Ammunition refers to the projectiles and propellants used in firearms and artillery, encompassing a wide range of products such as bullets, shells, cartridges, and explosives. Additionally, ongoing conflicts and territorial disputes across regions are contributing to an upsurge in demand for the small, medium, and large caliber ammunition market. One of the key trends shaping the global ammunition market is the development of lightweight and environment-friendly ammunition with enhanced accuracy and performance. Military organizations are increasingly investing in specialized ammunition tailored for counterterrorism, urban warfare, and precision-guided operations. Moreover, the market is also seeing a growing shift towards technologically advanced smart ammunition, which integrates sensors and guidance systems to improve targeting and minimize collateral damage. These innovations are likely to drive further market growth and competitive differentiation among key players.

Ammunition Market Drivers and Opportunities

Rising defense expenditures across nations are anticipated to lift the ammunition market during the forecast period

One of the most influential drivers for the global ammunition market is the continual rise in defense spending across major and emerging economies. Countries are increasingly prioritizing the modernization of their military forces, and ammunition forms the backbone of this modernization. For instance, the U.S., China, India, and Russia have substantially ramped up their defense budgets to procure modern weaponry and advanced munitions. According to the Stockholm International Peace Research Institute (SIPRI), global military expenditure reached a record high of over $2.2 trillion in recent years, reflecting a strong upward trend. These investments are not limited to large economies; smaller nations with regional security concerns are also enhancing their defense arsenals. The demand spans various types of ammunition, including small-caliber, medium-caliber, and large-caliber categories for both training and combat operations. Additionally, geopolitical tensions, border disputes, and regional conflicts fuel urgent procurement needs, further bolstering ammunition demand. The continuous replacement and stockpiling of ammunition due to aging inventories and usage during training or conflict scenarios ensures a stable and recurring demand cycle. Therefore, this surge in military spending is directly correlated with increased ammunition production and procurement, thereby significantly contributing to market growth.

Surge in terrorism and insurgency activities is a vital driver for influencing the growth of the global ammunition market

The growing prevalence of terrorism, insurgency, and internal security threats has significantly driven demand for ammunition worldwide. Several regions, particularly in the Middle East, Africa, South Asia, and parts of Latin America, continue to witness armed conflict and extremist activities. Governments are compelled to equip their defense and law enforcement agencies with adequate ammunition to counter these threats effectively. In addition to the armed forces, the demand from paramilitary units, homeland security departments, and special forces has surged, further expanding the customer base for ammunition manufacturers. Moreover, hybrid warfare and asymmetric threats from non-state actors necessitate the use of various ammunition types, including specialized rounds for urban combat, sniping, and riot control. Urbanization of conflict zones and the rise in close-quarter battles also increase the requirement for precision-guided munitions and enhanced kinetic projectiles. These factors have led to consistent orders and multi-year procurement contracts from government agencies, ensuring market stability. The intensification of global security threats has thus become a catalyst for ammunition market growth, reinforcing the need for continuous manufacturing innovation and supply chain resilience.

Demand for training and simulation ammunition is poised to create significant opportunities in the global ammunition market

As military and law enforcement agencies around the world emphasize skill enhancement and readiness, there is a growing need for specialized training and simulation ammunition. Unlike traditional combat munitions, training rounds are designed to replicate real-world conditions while ensuring safety and cost-effectiveness. These include blank cartridges, non-lethal rounds, marking cartridges, and digitally enhanced ammunition for use in virtual or augmented training environments. The adoption of advanced simulation technologies by defense forces creates a substantial opportunity for manufacturers to provide customized solutions. Additionally, frequent drills and the need for continual proficiency maintenance drive repeat purchases of such ammunition. Several countries mandate periodic requalification for both military and police personnel, further increasing the volume demand. The training ammunition market is also resilient to peacetime budget constraints, as governments prioritize preparedness even in the absence of active conflict. Furthermore, the commercial market for civilian shooting ranges and training academies is also expanding, offering a parallel stream of opportunity. Companies that invest in this niche, while ensuring compliance with safety and environmental standards, can secure long-term contracts and diversify their customer base.

Ammunition Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 21.5 Billion |

|

Market Forecast in 2033 |

USD 31.0 Billion |

|

CAGR % 2025-2033 |

3.4% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production capacity, growth factors, and more |

|

Segments Covered |

●

By Caliber ●

By Components ●

By Products ●

By Application |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Ammunition Market Report Segmentation Analysis

The Global Ammunition Market industry analysis is segmented into by Caliber, by Components, by Products, by Application, and by Region.

The small segment is anticipated to hold the highest share of the global ammunition market during the projected timeframe

Based on Caliber, the ammunition market is segmented into small, medium, and large calibers. In 2025, the small caliber ammunition market segment is anticipated to hold the highest share of 51.6% of the global ammunition market during the projected timeframe. This dominance is attributed to the widespread use of small-caliber ammunition in both the defense and civilian sectors. Small caliber rounds, such as 5.56mm, 7.62mm, and 9mm, are extensively used by military forces, law enforcement agencies, and private security personnel for rifles, handguns, and submachine guns. Moreover, the rising trend of civilian firearm ownership for personal protection and recreational shooting further fuels demand. The segment is also benefiting from continuous procurement programs, especially in regions facing internal security threats or actively modernizing their small arms inventories.

The cases segment is anticipated to hold the highest share of the market over the forecast period

By Components, the ammunition market is segmented by components into fuzes & primers, gunpowder, cases, projectiles and warheads, and others. Among these, the cases segment is anticipated to hold the highest share of the market over the forecast period. Ammunition cases are integral to the structural integrity and functionality of every round, serving to house the primer, gunpowder, and projectile. With growing global ammunition consumption across both military and civilian applications, the demand for high-quality cases has surged. Typically made of brass, steel, or polymer composites, the cases ensure safety, reliability, and proper chambering during firing. As governments and defense contractors increasingly invest in the production and stockpiling of small- and medium-caliber ammunition market, the need for corresponding cases rises proportionally.

The military & homeland security segment dominated the market in 2024 and is predicted to grow at the highest CAGR over the forecast period

By Application, the ammunition market is segmented by application into military & homeland security and civil & commercial. The military & homeland security segment dominated the global market in 2024 and is predicted to grow at the highest CAGR over the forecast period. This segment's dominance is underpinned by increasing global defense budgets, regional tensions, and the persistent threat of terrorism. Military forces across North America, Europe, Asia-Pacific, and the Middle East are continuously engaged in the procurement and replenishment of ammunition stockpiles for operational readiness and strategic deterrence. Homeland security forces and law enforcement agencies are also key users, especially in countries grappling with internal unrest, insurgencies, or border security concerns. The development and adoption of advanced ammunition such as smart rounds, guided munitions, and non-lethal ammunition for crowd control are further enhancing growth prospects.

The following segments are part of an in-depth analysis of the global

Helicopter market:

|

Market Segments |

|

|

By Type |

●

Civil &

Commercial Helicopter Market o

Light Helicopters o

Medium Helicopters o

Heavy Helicopters ●

Military Helicopter

Market o

Attack Helicopters o

Transport

Helicopters o

Reconnaissance

Helicopters o

Maritime Helicopters o

Search and Rescue

(SAR) Helicopters o

Training Helicopters |

|

By Maximum Take-off Weight (MTOW) |

●

Less than 3,000 Kg ●

3,000 Kg to 9,000 Kg ●

Greater than 9,000

Kg |

|

By Rotor Type |

●

Single-Rotor

Helicopters ●

Twin-Rotor

Helicopters ●

Tiltrotor

Helicopters ●

Others |

|

By Engine Type |

●

Single-Engine

Helicopters ●

Twin-Engine

Helicopters ●

Multi-Engine

Helicopters |

|

By Application |

●

Emergency Medical

Service ●

Corporate Service ●

Search and Rescue

Operation ●

Oil & Gas ●

Defense ●

Homeland Security ●

Others |

|

By Sales Channel |

●

New ●

Pre-Owned |

Ammunition Market Share Analysis by Region

North America Ammunition Market is projected to hold the largest share of the global ammunition market over the forecast period

Asia-Pacific dominated the global ammunition market in 2024, accounting for the largest share of 44.9%, and is expected to maintain its leading position throughout the forecast period. This regional dominance is primarily driven by escalating geopolitical tensions, border disputes, and sustained military modernization programs across countries like China, India, South Korea, and Japan. These nations are heavily investing in upgrading their defense capabilities, which includes large-scale procurement and indigenous production of a wide range of ammunition. China’s aggressive military buildup and India’s “Make in India” defense manufacturing initiatives are particularly significant contributors to the region’s market strength. Additionally, ongoing conflicts and the increasing focus on homeland security in Southeast Asian countries further accelerate ammunition demand. Governments are also expanding their training and simulation capacities, which contributes to the recurring purchase of training rounds and small-caliber ammunition market. The presence of several domestic manufacturers and favorable policy frameworks for defense investments make Asia-Pacific a central hub for ammunition production and consumption.

Meanwhile, the North America Ammunition Market is projected to register the highest CAGR during the forecast period. This growth is fueled by consistent military expenditure, rising civilian firearm ownership, and robust R&D efforts in advanced ammunition technologies across the United States and Canada. The strong emphasis on law enforcement preparedness, homeland security, and continuous innovation in smart and eco-friendly ammunition further supports the region’s rapid market expansion.

Ammunition Market Competition Landscape Analysis

Key Ammunition industry market players are prioritizing innovation in next-generation ammunition, with a strategic focus on lightweight lethal rounds and versatile multipurpose munitions to meet modern combat and defense needs. The market is being transformed by cutting-edge technologies, including caseless ammunition, laser-initiated rounds, precision-guided munitions, and environmentally friendly "green" ammunition solutions. Leading manufacturers maintain their competitive edge through diversified product portfolios and sustained R&D investments, enabling them to address evolving military, law enforcement, and civilian requirements while driving technological advancements in ballistic performance and operational efficiency.

Global Ammunition Market Recent Developments News:

- In January 2024: Nammo AS secured a USD 95 million investment from the Norwegian government to ramp up production capacity, with a primary focus on 155mm artillery ammunition to meet growing defense demands.

- In December 2023: Rheinmetall secured a USD 1.3 billion contract to supply tens of thousands of artillery shells to the Ukrainian armed forces, with deliveries slated for 2025.

- In November 2023: The UK Ministry of Defence (MOD) awarded BAE Systems a USD 21 million contract to provide additional small arms munitions over two years, reinforcing military stockpiles.

- In February 2023, Remington Arms Company LLC unveiled upgraded versions of its core ammunition lines, including handgun, shotshell, rimfire, and rifle cartridges. The enhancements focus on improved ballistic performance, reliability, and manufacturing precision across all categories.

The Global Ammunition Market is dominated by a few large companies, such as

- Northrop Grumman Corporation

- General Dynamics Corporation

- CBC Global Ammunition

- Olin Corporation

- Ruag Ammotec

- BAE Systems

- Thales Group

- Rheinmetall AG

- Nexter KNDS group

- Elbit Systems

- Nammo AS

- ST Engineering

- Others

Frequently Asked Questions

1. Global Ammunition Market Introduction and Market Overview

1.1. Objectives of the Study

1.2. Global Ammunition Market Scope and Market Estimation

1.2.1. Global Ammunition Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

1.2.2. Global Ammunition Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2033

1.3. Market Segmentation

1.3.1. Caliber of Global Ammunition Market

1.3.2. Components of Global Ammunition Market

1.3.3. Product of Global Ammunition Market

1.3.4. Application of Global Ammunition Market

1.3.5. Region of Global Ammunition Market

2. Executive Summary

2.1. Demand Side Trends

2.2. Key Market Trends

2.3. Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

2.4. Demand and Opportunity Assessment

2.5. Demand Supply Scenario

2.6. Market Dynamics

2.6.1. Drivers

2.6.2.Limitations

2.6.3. Opportunities

2.6.4.Impact Analysis of Drivers and Restraints

2.7. Emerging Trends for Ammunition Market

2.8. Porter’s Five Forces Analysis

2.9. PEST Analysis

2.10.Key Regulation

3. Global Ammunition Market Estimates & Historical Trend Analysis (2021 - 2024)

4. Global Ammunition Market Estimates & Forecast Trend Analysis, by Caliber

4.1. Global Ammunition Market Revenue (US$ Bn) Estimates and Forecasts, by Caliber, 2021 - 2033

4.1.1. Small

4.1.2. Medium

4.1.3. Large

5. Global Ammunition Market Estimates & Forecast Trend Analysis, by Components

5.1. Global Ammunition Market Revenue (US$ Bn) Estimates and Forecasts, by Components, 2021 - 2033

5.1.1. Fuzes & Primers

5.1.2. GunPowder

5.1.3. Cases

5.1.4. Projectiles and warheads

5.1.5. Others

6. Global Ammunition Market Estimates & Forecast Trend Analysis, by Product

6.1. Global Ammunition Market Revenue (US$ Bn) Estimates and Forecasts, by Product, 2021 - 2033

6.1.1. Bullets

6.1.2. Aerial Bombs

6.1.3. Artillery Shells

6.1.4. Grenades

6.1.5. Mortars

6.1.6. Others

7. Global Ammunition Market Estimates & Forecast Trend Analysis, by Application

7.1. Global Ammunition Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

7.1.1. Military & Homeland Security

7.1.2. Civil & Commercial

8. Global Ammunition Market Estimates & Forecast Trend Analysis, by region

1.1. Global Ammunition Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

1.1.1. North America

1.1.2. Europe

1.1.3. Asia Pacific

1.1.4. Middle East & Africa

1.1.5. Latin America

9. North America Ammunition Market: Estimates & Forecast Trend Analysis

9.1. Ammunition Market in North America Assessments & Key Findings

9.1.1. North America Ammunition Market Introduction

9.1.2. North America Ammunition Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

9.1.2.1. By Caliber

9.1.2.2. By Components

9.1.2.3. By Product

9.1.2.4. By Application

9.1.2.5. By Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Ammunition Market: Estimates & Forecast Trend Analysis

10.1. Europe Ammunition Market Assessments & Key Findings

10.1.1. Europe Ammunition Market Introduction

10.1.2. Europe Ammunition Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

10.1.2.1. By Caliber

10.1.2.2. By Components

10.1.2.3. By Product

10.1.2.4. By Application

10.1.2.5. By Country

10.1.2.5.1. Germany

10.1.2.5.2. Italy

10.1.2.5.3. U.K.

10.1.2.5.4. France

10.1.2.5.5. Spain

10.1.2.5.6. Switzerland

10.1.2.5.7. Rest of Europe

11. Asia Pacific Ammunition Market: Estimates & Forecast Trend Analysis

11.1. Asia Pacific Market Assessments & Key Findings

11.1.1. Asia Pacific Ammunition Market Introduction

11.1.2. Asia Pacific Ammunition Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

11.1.2.1. By Caliber

11.1.2.2.By Components

11.1.2.3.By Product

11.1.2.4.By Application

11.1.2.5.By Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Ammunition Market: Estimates & Forecast Trend Analysis

12.1. Middle East & Africa Market Assessments & Key Findings

12.1.1. Middle East & Africa Ammunition Market Introduction

12.1.2. Middle East & Africa Ammunition Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

12.1.2.1.By Caliber

12.1.2.2. By Components

12.1.2.3. By Product

12.1.2.4. By Application

12.1.2.5. By Country

12.1.2.5.1. South Africa

12.1.2.5.2. UAE

12.1.2.5.3. Saudi Arabia

12.1.2.5.4. Rest of MEA

13. Latin America Ammunition Market: Estimates & Forecast Trend Analysis

13.1. Latin America Market Assessments & Key Findings

13.1.1. Latin America Ammunition Market Introduction

13.1.2. Latin America Ammunition Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

13.1.2.1.By Caliber

13.1.2.2. By Components

13.1.2.3. By Product

13.1.2.4. By Application

13.1.2.5. By Country

13.1.2.5.1. Brazil

13.1.2.5.2. Mexico

13.1.2.5.3. Argentina

13.1.2.5.4. Rest of LATAM

14. Country Wise Market: Introduction

15. Competition Landscape

15.1. Global Ammunition Market Product Mapping

15.2. Global Ammunition Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

15.3. Global Ammunition Market Tier Structure Analysis

15.4. Global Ammunition Market Concentration & Company Market Shares (%) Analysis, 2023

16. Company Profiles

16.1. Northrop Grumman Corporation

16.1.1. Company Overview & Key Stats

16.1.2. Financial Performance & KPIs

16.1.3. Product Portfolio

16.1.4. SWOT Analysis

16.1.5. Business Strategy & Recent Developments

* Similar details would be provided for all the players mentioned below

16.2. General Dynamics Corporation

16.3. CBC Global Ammunition

16.4. Olin Corporation

16.5. Ruag Ammotec

16.6. BAE Systems

16.7. Thales Group

16.8. Rheinmetal AG

16.9. Nexter KNDS group

16.10. Elbit Systems

16.11. Nammo AS

16.12. ST Engineering

16.13. Other Prominent Players

17. Research Methodology

17.1. External Transportations / Databases

17.2. Internal Proprietary Database

17.3. Primary Research

17.4. Secondary Research

17.5. Assumptions

17.6. Limitations

17.7. Report FAQs

18. Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

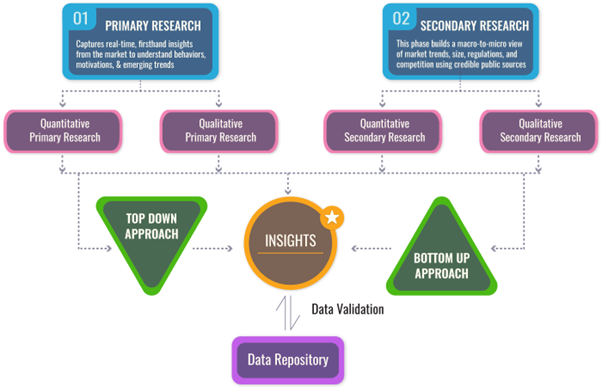

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables