Global Base Oil Market Size And Forecast (2025 - 2033), Global And Regional Growth, Trend, Share And Industry Analysis Report Coverage: By Product (Group I, Group II, Group III, Group IV, Group V), By Application (Automotive Oils, Process Oils, Hydraulic Oils, Metalworking Fluids, Industrial Oils, Others) And Geography

2025-07-18

Chemicals & Materials

Description

Global Base Oil Market Overview

The global Base Oil market is

projected to reach US$50.4 Billion by 2033 from US$34.1 Billion in 2025. The

market is expected to register a CAGR of 5.1% from 2025–2033. This growth

is primarily attributed to increasing demand from the automotive, industrial,

and marine sectors.

Base oils are essential

components used to formulate lubricants, which are necessary to minimize

friction and wear in engines and machinery. There is an increasing demand for

more high-performance lubricants as global industries grow and vehicle ownership

increases, contributing to a simultaneous increase in base oil market size.

Growth trends are increasingly shifting to Group II and Group III base oils

because of superior oxidative stability and less sulfur content. Growing

environmental regulations and the trends demanding cleaner and more efficient

lubricants are shifting demand towards these types of base oils. Increasing

synthetic and semi-synthetic lubricant production, especially in

high-performance automotive and industrial applications, also supports the

increasing use of higher-quality base oils, as well as improvements in refining

technologies producing categories of base oils that are premium grade, allowing

base oil producers to manufacture base oils with decreased costs.

Global Base Oil Market Drivers and Opportunities

Rising Demand for High-Performance Engine Oils is anticipated to lift

the Base Oil market during the forecast period

The rising demand for

high-performance engine oils is a key driver of growth in the global base oil

market. Advances in automotive technology and consumer preference for vehicles

with better mileage, lower emissions, and enhanced engine performance have increased

the need for superior lubricants. These lubricants rely on high-quality base

oils with excellent thermal and oxidative stability, low volatility, and a high

viscosity index. Emerging markets like India, China, and Brazil are

experiencing rapid automotive sector growth, with stricter emission standards

and higher vehicle ownership boosting demand for Group II and Group III base

oils. The commercial vehicle segment, requiring durable engine oils for extreme

conditions, further drives consumption. OEM recommendations for synthetic or

semi-synthetic oils in modern engines also support this trend. Urbanization and

economic development in emerging regions are expanding transportation and

logistics industries, increasing demand for automotive lubricants and premium

base oils. Market players are responding by expanding production and investing

in R&D for advanced base oils, supporting long-term market growth. As

environmental and performance standards evolve, high-performance engine oils

and the premium base oils they depend on will remain a critical factor in the

market’s expansion.

Stringent Environmental Regulations Driving Shift to Group II and Group

III Base Oils is a vital driver for influencing the growth of the global Base

Oil market

Stringent environmental

regulations and emissions standards are significantly influencing the global

base oil market by accelerating the shift from Group I to Group II and Group

III base oils. These regulations, which aim to reduce carbon emissions and improve

fuel efficiency, are pushing automotive and industrial lubricant manufacturers

to opt for base oils with better properties, including lower sulfur content,

improved viscosity index, and enhanced oxidation stability. Group I base oils,

with their higher aromatic content and impurities, are being gradually phased

out in favor of cleaner alternatives. Governments in North America, Europe, and

parts of Asia are mandating lower emissions and more efficient lubricants,

prompting refiners and manufacturers to reconfigure or upgrade their facilities

to produce Group II and Group III base oils. These base oils meet the

performance requirements of newer engine designs and help extend drain

intervals, reduce engine wear, and enhance overall fuel economy. This regulatory

shift has also opened up market opportunities for refineries that are capable

of producing premium-grade base oils. As sustainability becomes an increasingly

integral part of business strategies across industries, regulatory compliance

acts as both a challenge and a catalyst for innovation in the base oil

industry. Consequently, the base oil market is undergoing a significant

transformation, where environmental stewardship is directly linked with product

evolution and market competitiveness, thus serving as a vital driver of growth.

Growing Adoption of Synthetic and Bio-Based Lubricants is poised to

create significant opportunities in the global Base Oil market

The rising adoption of synthetic

and bio-based lubricants offers a compelling opportunity for the global base

oil market, particularly for producers of Group III, Group IV (PAO), and Group

V base oils. As industries and consumers become increasingly aware of the

environmental impact of conventional lubricants, demand for more sustainable

and high-performance alternatives is rising. Synthetic lubricants offer

superior properties such as thermal stability, low volatility, and extended

drain intervals, which make them ideal for modern engines and high-load

industrial applications. Similarly, bio-based lubricants derived from renewable

sources are gaining traction in environmentally sensitive sectors such as

agriculture, marine, and forestry. This transition is being supported by

stringent environmental regulations, eco-label certifications, and the growing

emphasis on corporate sustainability. For base oil manufacturers, this shift

presents an opportunity to innovate and develop base stocks that meet both performance

and ecological standards. R&D investments aimed at producing high-quality

synthetic or bio-based base oils can provide a competitive edge. Additionally,

lubricant blenders and OEMs increasingly require base oils that can help them

formulate eco-friendly products without compromising performance. With

consumers and industrial users willing to pay a premium for sustainable and

long-lasting lubricants, base oil producers have a clear path to value-added

offerings and the Base Oil Market price. The expansion of synthetic and

bio-lubricants is not just a trend, but a strategic opportunity for market

differentiation and long-term profitability in the base oil industry.

Base Oil Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 34.1 Billion |

|

Market Forecast in 2033 |

USD 50.4 Billion |

|

CAGR % 2025-2033 |

5.1% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production capacity, growth factors and more |

|

Segments Covered |

●

By Product ●

By Application |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Base Oil Market Report Segmentation Analysis

The Global Base Oil Market

industry analysis is segmented by Product, Application, and by Region.

The Group I segment is anticipated to hold the highest share of the

global Base Oil market during the projected timeframe.

By Product, the market is

segmented into Group I, Group II, Group III, Group IV, and Group V. The Group I

segment is anticipated to hold the highest share of 40.6% in the global base

oil report price during the projected timeframe. Group I base oils are widely

used due to their cost-effectiveness and versatility across a broad range of

applications, particularly in the manufacturing of lubricants for automotive,

industrial, and marine sectors. The high demand from small and medium-scale

industries that prioritize affordability and moderate performance further

reinforces the dominance of this segment.

The Automotive Oils segment is anticipated to hold the highest share of

the market over the forecast period.

By Application, the market is

segmented into Automotive Oils, Process Oils, Hydraulic Oils, Metalworking

Fluids, Industrial Oils, and Others. The Automotive Oils segment is anticipated

to hold the highest share of the global base oil market over the forecast

period. This dominance is driven by the continuous growth of the global

automotive industry, increasing vehicle ownership, and the rising need for

efficient engine lubrication. Base oils form the primary component in the

formulation of automotive lubricants such as engine oils, gear oils, and

transmission fluids. As internal combustion engines require lubricants that can

withstand high temperatures and pressures while reducing wear and enhancing

fuel efficiency, the demand for high-performance base oils has surged.

The following segments are part of an in-depth analysis of the global

base oil market:

|

Market Segments |

|

|

by Product |

●

Group I ●

Group II ●

Group III ●

Group IV ●

Group V |

|

by Application |

●

Automotive Oils ●

Process Oils ●

Hydraulic Oils ●

Metalworking Fluids ●

Industrial Oils ●

Others |

Base Oil Market Share Analysis by Region

Asia Pacific is projected to hold the largest share of the global Base

Oil market over the forecast period.

Asia Pacific dominated the global

base oil market in 2024, accounting for a commanding 46.7% share, and is

projected to maintain its leadership throughout the forecast period. This

significant market size is primarily driven by the rapid expansion of the

automotive and industrial sectors across key economies such as China, India,

South Korea, and Japan. The region has witnessed a surge in vehicle ownership

and manufacturing activities, both of which are major consumers of lubricants

and, consequently, base oils. In addition, increasing infrastructure

development, urbanization, and industrialization have amplified the demand for

various machinery and equipment, further boosting the consumption of industrial

lubricants. Asia Pacific also benefits from a strong refining capacity,

especially in countries like South Korea and Singapore, which serve as major

base oil exporters due to advanced refining technologies. Government

initiatives promoting industrial growth, coupled with relatively lower

production costs and a steady rise in consumer demand, are creating a favorable

environment for sustained market growth. Moreover, the presence of several

leading lubricant manufacturers and base oil producers in the region

contributes to Asia Pacific’s dominance in the global base oil market analysis

and trends.

Meanwhile, North America is

projected to register the highest CAGR over the forecast period. This

accelerated growth is fueled by increased adoption of high-performance

synthetic lubricants, growing demand for cleaner and more efficient engine

oils, and advancements in refining technologies. The U.S. and Canada are seeing

rising investments in automotive innovation and industrial automation, which

are positively influencing the consumption of premium base oils. Additionally,

stricter emission regulations are driving a shift toward higher group base

oils, supporting market growth in the region.

Base Oil Market Competition Landscape Analysis

The global base oil market is

marked by robust competition among key players focusing on innovation,

strategic expansion, and sustainability. Continuous research and development

efforts lead to the introduction of advanced base oil formulations with improved

performance characteristics, catering to evolving industry demands.

Global Base Oil Market Recent Developments News:

- In August

2019, ExxonMobil Chemical Company appointed Synergy Additives Company

S.A. de C.V. as its exclusive distributor for Group IV/V synthetic base

stocks across Mexico, Central America, and the Caribbean. This partnership

strengthened ExxonMobil’s regional market reach and supply chain

efficiency for high-performance lubricants.

- In May 2018, Chevron

Corporation’s subsidiary Chevron U.S.A. Inc. partnered with Novvi, LLC to

co-develop and commercialize renewable base oil technologies. The

collaboration aimed to expand Chevron’s portfolio of sustainable,

bio-based lubricants for global markets.

The Global Base Oil Market is dominated by a few large

companies, such as

●

Chevron Corporation

●

Exxon Mobil

Corporation

●

S-OIL CORPORATION

●

Motiva Enterprises LLC

●

SK Innovation Co., Ltd.

●

Royal Dutch Shell Plc

●

Neste Oyj

●

AVISTA OIL AG

●

Nynas AB

●

Repsol S.A.

●

Ergon, Inc.

●

Calumet Specialty

Products Partners, L.P.

●

H&R Group

●

Sinopec Corp.

●

PetroChina Company

Limited

●

Saudi Aramco

●

Abu Dhabi National Oil

Company (ADNOC)

●

PT Pertamina (Persero)

●

Phillips 66

●

Petroliam Nasional

Berhad (PETRONAS)

●

GRUPA LOTOS S.A.

●

Sepahan Oil

●

GS Caltex Corporation

●

Hindustan Petroleum

Corporation Limited or HPCL

● Others

Frequently Asked Questions

- Global Base Oil Market Introduction and Market Overview

- Objectives of the Study

- Global Base Oil Market Scope and Market Estimation

- Global Base Oil Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Base Oil Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2033

- Market Segmentation

- Product of Global Base Oil Market

- Application of Global Base Oil Market

- Region of Global Base Oil Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Base Oil Market

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Base Oil Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global Base Oil Market Estimates & Forecast Trend Analysis, by Product

- Global Base Oil Market Revenue (US$ Bn) Estimates and Forecasts, by Product, 2021 - 2033

- Group I

- Group II

- Group III

- Group IV

- Group V

- Global Base Oil Market Revenue (US$ Bn) Estimates and Forecasts, by Product, 2021 - 2033

- Global Base Oil Market Estimates & Forecast Trend Analysis, by Application

- Global Base Oil Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

- Automotive Oils

- Process Oils

- Hydraulic Oils

- Metalworking Fluids

- Industrial Oils

- Others

- Global Base Oil Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2021 - 2033

- Global Base Oil Market Estimates & Forecast Trend Analysis, by Region

- Global Base Oil Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2021 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Base Oil Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2021 - 2033

- North America Base Oil Market: Estimates & Forecast Trend Analysis

- North America Base Oil Market Assessments & Key Findings

- North America Base Oil Market Introduction

- North America Base Oil Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product

- By Application

- By Country

- The U.S.

- Canada

- North America Base Oil Market Assessments & Key Findings

- Europe Base Oil Market: Estimates & Forecast Trend Analysis

- Europe Base Oil Market Assessments & Key Findings

- Europe Base Oil Market Introduction

- Europe Base Oil Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product

- By Application

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Switzerland

- Rest of Europe

- Europe Base Oil Market Assessments & Key Findings

- Asia Pacific Base Oil Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Base Oil Market Introduction

- Asia Pacific Base Oil Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product

- By Application

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Base Oil Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Base Oil Market Introduction

- Middle East & Africa Base Oil Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product

- By Application

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Base Oil Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Base Oil Market Introduction

- Latin America Base Oil Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Product

- By Application

- By Country

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Base Oil Market Product Mapping

- Global Base Oil Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Base Oil Market Tier Structure Analysis

- Global Base Oil Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- Chevron Corporation

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Chevron Corporation

* Similar details would be provided for all the players mentioned below

- Exxon Mobil Corporation

- S-OIL CORPORATION

- Motiva Enterprises LLC

- SK innovation Co., Ltd.

- Royal Dutch Shell Plc

- Neste Oyj

- AVISTA OIL AG

- Nynas AB

- Repsol S.A.

- Ergon, Inc.

- Calumet Specialty Products Partners, L.P.

- H&R Group

- Sinopec Corp.

- PetroChina Company Limited

- Saudi Aramco

- Abu Dhabi National Oil Company (ADNOC)

- PT Pertamina (Persero)

- Phillips 66

- Petroliam Nasional Berhad (PETRONAS)

- GRUPA LOTOS S.A.

- Sepahan Oil

- GS Caltex Corporation

- Hindustan Petroleum Corporation Limited or HPCL

- Others

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

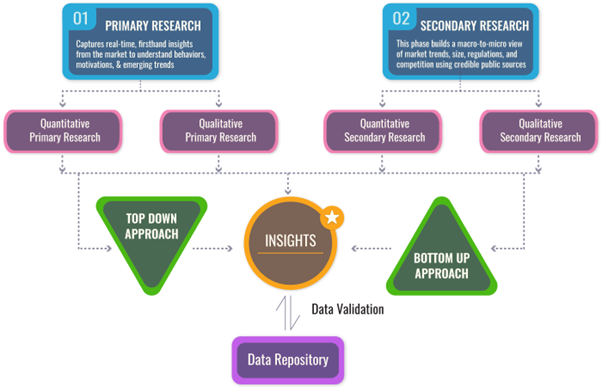

Our Research Methodology

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables