Oncology Drugs Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Therapy Type (Chemotherapy, Targeted Therapy, Immunotherapy (Biologic Therapy), Hormonal Therapy and Others (Radiopharmaceuticals, Biosimilars)); By Drug Class (Alkylating Agents, Antimetabolites, Mitotic Inhibitors, Cytotoxic Antibiotics, Monoclonal Antibodies, Tyrosine Kinase Inhibitors and Others); Cancer Type (Breast Cancer, Lung Cancer, Colorectal Cancer, Prostate Cancer, Blood Cancer, Skin Cancer, Ovarian Cancer, Pancreatic Cancer and Other Cancers)); By Dosage Form (Oral, Injectable, and Others); By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies) and Geography

2025-07-17

Healthcare

Description

Oncology Drugs Market

Overview

The oncology drugs market is anticipated to experience substantial growth from 2025 to 2033, increase in the adoption of automation technologies in the food and beverage industry being a key factor propelling this growth. With an estimated valuation of approximately USD 253.6 billion in 2025, the market is expected to reach USD 580.2 billion by 2033, registering a robust compound annual growth rate (CAGR) of 11.2% over the decade.

The oncology drug development

trends represents one of the most dynamic and rapidly evolving segments of the

global pharmaceutical industry. Driven by the rising global cancer burden,

increasing healthcare spending, and continuous advancements in molecular

biology and biotechnology, this market is witnessing sustained growth. Oncology

drugs are designed to treat various forms of cancer by targeting and inhibiting

the growth of malignant cells. The market encompasses several key drug classes,

including chemotherapy, targeted therapy, immunotherapy (biologic therapy),

hormonal therapy, and others such as oncology radiopharmaceuticals market and

biosimilars.

Among these, targeted therapies

and immunotherapies are gaining prominence due to their improved efficacy and

reduced toxicity compared to traditional chemotherapy. The surge in

personalized medicine, supported by genetic profiling and biomarker development,

is also reshaping treatment paradigms. Pharmaceutical companies are heavily

investing in research and development, leading to a robust pipeline of novel

therapies.

Moreover, regulatory support for

accelerated drug approvals, especially for breakthrough cancer treatments, is

contributing to faster market entry. Despite the high treatment costs posing

challenges, the growing adoption of biosimilars and value-based care models is

helping to balance affordability. With aging populations, increased cancer

screening, and ongoing innovation, the oncology drugs market is poised to

remain a key focus of global healthcare investment and development.

Oncology Drugs Market

Drivers and Opportunities

Rising Global Cancer Prevalence is anticipated to lift the oncology

drugs market during the forecast period

One of the primary drivers of the

oncology drugs market is the continuous rise in global anticancer drugs market.

According to the World Health Organization (WHO), cancer remains one of the

leading causes of death worldwide, with cases expected to increase

significantly due to aging populations, lifestyle changes, and environmental

exposures. This growing disease burden is prompting increased demand for

effective cancer therapies across all healthcare settings. Early diagnosis

through improved screening programs has also contributed to higher detection

rates, subsequently driving up the need for oncology drugs. Additionally,

awareness campaigns and improved access to healthcare services in emerging

economies are expanding the patient base. Governments and health organizations

are allocating more resources to combat cancer, further stimulating market

growth. As cancer incidence rises, pharmaceutical companies are under pressure

to innovate and deliver new treatment solutions, thereby accelerating research,

development, and commercialization of oncology drugs globally.

Advancements in Precision and Targeted Therapies drive the global

Oncology Drugs Market

The advent of precision medicine

and targeted therapies has significantly transformed the oncology landscape,

driving market growth. Unlike traditional chemotherapy, targeted therapies aim

at specific molecular targets involved in cancer progression, offering enhanced

efficacy and fewer side effects. Technologies such as next-generation

sequencing (NGS), liquid biopsies, and biomarker identification enable

physicians to tailor treatments to individual patients based on their genetic

profiles. This personalized approach not only improves outcomes but also

enhances patient compliance and satisfaction. The rapid development of

monoclonal antibodies, tyrosine kinase inhibitors, and antibody-drug conjugates

is a testament to this shift. Furthermore, collaboration between biotech firms,

academia, and pharmaceutical companies has led to a surge in clinical trials

exploring new molecular targets. Regulatory agencies are also facilitating

faster approvals of targeted therapies, especially for rare and aggressive cancers.

These innovations are shaping the future of oncology treatment and

significantly expanding the scope of the oncology drugs market.

Opportunity for the Oncology Drugs Market

Growing Adoption of Biosimilars in Oncology is a significant

opportunity in the global Oncology Drugs Market

The growing adoption of

biosimilars presents a major opportunity in the oncology drugs market. As

patent expirations of blockbuster biologics occur, biosimilars are being

introduced as cost-effective alternatives, particularly for therapies involving

monoclonal antibodies used in cancer treatment. These products offer similar

efficacy and safety profiles to originator biologics but at significantly lower

prices, making cancer treatment more accessible, especially in low- and

middle-income countries. Healthcare providers and payers are increasingly

embracing biosimilars to manage rising treatment costs without compromising

care quality. Moreover, regulatory bodies like the FDA and EMA are streamlining

approval processes for biosimilars, boosting their market entry. Pharmaceutical

companies are also expanding their oncology biosimilar market pipelines to tap

into this growing demand. The increased availability and acceptance of

biosimilars can reduce the financial burden on healthcare systems, widen

patient access to essential cancer therapies, and create a more competitive

market landscape, ultimately benefiting both patients and providers.

Oncology Drugs Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 253.6 Billion |

|

Market Forecast in 2033 |

USD 580.2 Billion |

|

CAGR % 2025-2033 |

11.2% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production Capacity, growth factors, and more |

|

Segments Covered |

●

By Therapy Type ●

By Drug Class ●

By Cancer Type ●

By Dosage Form ●

By End-user |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Oncology Drugs Industry Report Segmentation Analysis

The global Oncology Drugs

industry analysis is segmented into by Therapy Type, by Drug Class, by Cancer

Type, by Dosage Form and by end-user and by region.

Targeted Therapy Type segment leading the oncology drugs market

Targeted therapy is currently the

leading segment within the oncology drugs market due to its precision, reduced

toxicity, and superior clinical outcomes compared to conventional treatments

like chemotherapy. These therapies work by interfering with specific molecules

involved in tumor growth and progression, such as mutated genes or proteins.

Key examples include tyrosine kinase inhibitors, monoclonal antibodies, and

PARP inhibitors. This approach allows for personalized treatment plans tailored

to an individual's unique cancer profile, resulting in better treatment

efficacy and fewer adverse effects. The rising prevalence of cancers with

identifiable molecular targets, such as HER2-positive breast cancer and

EGFR-mutated lung cancer, has further driven demand. The global shift towards

precision medicine, along with advancements in companion diagnostics and

genomics, is accelerating the adoption of targeted therapies. Continued

investment in R&D and faster regulatory approvals are expected to sustain

this segment's dominance in the oncology drugs market.

The alkylating agents drug class segment holds a major share in the

oncology drugs market

Alkylating agents hold a

significant share in the oncology drugs market, largely due to their

broad-spectrum efficacy across various cancer types. These drugs work by

interfering with DNA replication, ultimately inducing cancer cell death. Common

alkylating agents include cyclophosphamide, melphalan, and ifosfamide, which

are widely used in treating hematologic cancers (like lymphoma and leukemia)

and solid tumors. Despite the emergence of more targeted and biologic

therapies, alkylating agents continue to be a cornerstone in oncology,

especially in multi-drug chemotherapy regimens. Their versatility and proven

clinical outcomes make them particularly valuable in low-resource settings

where newer therapies may not be accessible. Moreover, they are often used in

conjunction with modern therapies to enhance overall treatment efficacy. The

longevity and continued reliance on these agents in both curative and

palliative care contribute to their sustained market presence, especially in

regions where traditional chemotherapy remains the standard of care.

Lung Cancer Type segment dominating in the Oncology Drugs Market

Lung cancer accounts for the

largest share within the oncology drugs market due to its high global incidence

and mortality rate. Non-small cell lung cancer (NSCLC) and small cell lung

cancer (SCLC) together represent a substantial portion of diagnosed cancer

cases worldwide. Factors such as increased smoking prevalence, environmental

pollution, and aging populations contribute to its widespread occurrence. As a

result, there is a significant demand for effective therapeutic options. The

development of advanced targeted therapies (e.g., EGFR and ALK inhibitors),

immunotherapies (e.g., PD-1/PD-L1 inhibitors), and novel drug delivery

mechanisms has significantly improved treatment outcomes and extended survival

in lung cancer patients. Early detection efforts and large-scale screening

programs have also played a role in identifying more cases, thus expanding the

patient pool for drug therapies. The high disease burden, coupled with

continual innovation and regulatory support for new treatments, ensures lung cancer

remains a dominant segment in the oncology drugs market.

Hospital Pharmacies' distribution channel segment contributes a major

share to the oncology drugs market

Hospital pharmacies dominate the

distribution channel segment in the oncology drugs market due to the complex

nature of cancer treatments, which often require controlled environments,

specialized handling, and continuous medical supervision. Many oncology drugs,

especially intravenous chemotherapies, biologics, and targeted therapies, need

to be administered in clinical settings under the guidance of trained

healthcare professionals. Hospital pharmacies are also integral to ensuring the

safe storage, dosing, and management of high-cost and high-potency cancer

drugs. Additionally, inpatient and outpatient cancer treatment centers are

typically associated with hospitals, making these institutions central hubs for

oncology drug dispensing. Hospital pharmacies are also the primary points for

clinical trial drugs, investigational therapies, and emergency drug access

programs. With rising healthcare infrastructure development globally and

increased centralization of cancer care in specialized hospitals, this distribution

channel continues to hold the largest market share, offering efficiency,

patient safety, and optimized drug utilization.

The following segments are part

of an in-depth analysis of the global oncology drugs market:

|

Market Segments |

|

|

By Therapy Type |

●

Chemotherapy ●

Targeted Therapy ●

Immunotherapy

(Biologic Therapy) ●

Hormonal Therapy ●

Others

(Radiopharmaceuticals, Biosimilars) |

|

By Drug Class

|

●

Alkylating Agents ●

Antimetabolites ●

Mitotic Inhibitors ●

Cytotoxic

Antibiotics ●

Monoclonal

Antibodies ●

Tyrosine Kinase

Inhibitors ●

Others |

|

By Cancer Type

|

●

Breast Cancer ●

Lung Cancer ●

Colorectal Cancer ●

Prostate Cancer ●

Blood Cancer ●

Skin Cancer ●

Ovarian Cancer ●

Pancreatic Cancer ●

Other Cancers |

|

By Dosage Form |

●

Oral ●

Injectable ●

Others (Topical,

Intravenous) |

|

By End-user |

●

Hospital Pharmacies ●

Retail Pharmacies ●

Online Pharmacies |

Oncology Drugs Market

Share Analysis by Region

North America region is projected to hold the largest share of the

global Oncology Drugs Market over the forecast period.

North America is expected to

maintain its dominance in the global oncology drugs market throughout the

forecast period, driven by a combination of advanced healthcare infrastructure,

high healthcare expenditure, and a strong presence of leading pharmaceutical

companies. The region benefits from early adoption of innovative therapies,

including targeted treatments and immunotherapies, as well as a

well-established system for clinical research and drug approvals. The United

States, in particular, has a high cancer prevalence, which fuels sustained

demand for advanced oncology drugs. Furthermore, favourable regulatory

frameworks from agencies like the FDA, coupled with a growing emphasis on

personalized medicine, expedite the approval and adoption of new therapies.

Insurance coverage, access to high-end diagnostics, and public awareness

campaigns also contribute to the market's growth. Additionally, the presence of

leading biopharmaceutical players and ongoing R&D investments make North

America a central hub for oncology drug innovation and commercialization.

Oncology Drugs Market

Competition Landscape Analysis

The market is

competitive, with several established players and new entrants offering a range

of oncology drug products. Some of the key players include F. Hoffmann-La Roche

Ltd, Bristol-Myers Squibb, Johnson & Johnson, Merck & Co., Pfizer,

AstraZeneca, Novartis, and others.

Global Oncology Drugs

Market Recent Developments News:

- In June 2025, BioNTech and Bristol Myers Squibb

launched a co-development deal for BNT327, a bispecific PD-L1/VEGF-A

antibody with potential in lung and breast cancers. The collaboration

includes $1.5 billion upfront, plus $2 billion guaranteed and up to

$7.6 billion in milestones.

- In April 2025, AstraZeneca shared positive

Phase III results for camizestrant at ASCO: the new oral estrogen-receptor

degrader cut the risk of progression or death by 56% in advanced HR+

breast cancer and delayed disease progression by 16 months, highlighting a

move toward precision cancer care.

- In May 2025, AbbVie’s antibody–drug conjugate Emrelis (telisotuzumab

vedotin) received FDA approval for previously treated, advanced non‑small cell lung cancer with

high c‑Met

expression. Approval followed strong Phase I data showing a 63% objective

response rate.

The Global Oncology Drugs Market is dominated by a few large companies,

such as

●

F. Hoffmann-La Roche

Ltd

●

Bristol-Myers Squibb

●

Johnson & Johnson

●

Merck & Co.

●

Pfizer

●

AstraZeneca

●

Novartis

●

AbbVie

●

Eli Lilly and Company

●

Astellas Pharma

●

GSK

●

Sanofi

●

Takeda Pharmaceutical

●

Amgen

●

Gilead Sciences

● Other Prominent Players

Frequently Asked Questions

- Global Oncology Drugs Market Introduction and Market Overview

- Objectives of the Study

- Global Oncology Drugs Market Scope and Market Estimation

- Global Oncology Drugs Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Oncology Drugs Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2033

- Market Segmentation

- Therapy Type of Global Oncology Drugs Market

- Drug Class of Global Oncology Drugs Market

- Cancer Type of Global Medical Devices Coating Market

- Dosage Form of Global Oncology Drugs Market

- Distribution Channel of Global Medical Devices Coating Market

- Region of Global Oncology Drugs Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Pipeline Analysis

- Emerging Trends for Oncology Drugs Market

- Key Product/Brand Analysis

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Oncology Drugs Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global Oncology Drugs Market Estimates & Forecast Trend Analysis, by Therapy Type

- Global Oncology Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by Therapy Type, 2021 - 2033

- Chemotherapy

- Targeted Therapy

- Immunotherapy (Biologic Therapy)

- Hormonal Therapy

- Others

- Global Oncology Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by Therapy Type, 2021 - 2033

- Global Oncology Drugs Market Estimates & Forecast Trend Analysis, by Drug Class

- Global Oncology Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by Drug Class, 2021 - 2033

- Alkylating Agents

- Antimetabolites

- Mitotic Inhibitors

- Cytotoxic Antibiotics

- Monoclonal Antibodies

- Tyrosine Kinase Inhibitors

- Others

- Global Oncology Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by Drug Class, 2021 - 2033

- Global Oncology Drugs Market Estimates & Forecast Trend Analysis, by Cancer Type

- Global Oncology Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by Cancer Type, 2021 - 2033

- Breast Cancer

- Lung Cancer

- Colorectal Cancer

- Prostate Cancer

- Blood Cancer

- Skin Cancer

- Ovarian Cancer

- Pancreatic Cancer

- Other Cancers

- Global Oncology Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by Cancer Type, 2021 - 2033

- Global Oncology Drugs Market Estimates & Forecast Trend Analysis, by Dosage Form

- Global Oncology Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by Dosage Form, 2021 - 2033

- Oral

- Injectable

- Others (Topical, Intravenous etc.)

- Global Oncology Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by Dosage Form, 2021 - 2033

- Global Oncology Drugs Market Estimates & Forecast Trend Analysis, by Distribution Channel

- Global Oncology Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution Channel, 2021 - 2033

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Global Oncology Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by Distribution Channel, 2021 - 2033

- Global Oncology Drugs Market Estimates & Forecast Trend Analysis, by region

- Global Oncology Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Oncology Drugs Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America Oncology Drugs Market: Estimates & Forecast Trend Analysis

- North America Oncology Drugs Market Assessments & Key Findings

- North America Oncology Drugs Market Introduction

- North America Oncology Drugs Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Therapy Type

- By Drug Class

- By Cancer Type

- By Dosage Form

- By Distribution Channel

- By Country

- The U.S.

- Canada

- North America Oncology Drugs Market Assessments & Key Findings

- Europe Oncology Drugs Market: Estimates & Forecast Trend Analysis

- Europe Oncology Drugs Market Assessments & Key Findings

- Europe Oncology Drugs Market Introduction

- Europe Oncology Drugs Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Therapy Type

- By Drug Class

- By Cancer Type

- By Dosage Form

- By Distribution Channel

- By Country

- Germany

- Italy

- K.

- France

- Spain

- Switzerland

- Rest of Europe

- Europe Oncology Drugs Market Assessments & Key Findings

- Asia Pacific Oncology Drugs Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Oncology Drugs Market Introduction

- Asia Pacific Oncology Drugs Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Therapy Type

- By Drug Class

- By Cancer Type

- By Dosage Form

- By Distribution Channel

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Oncology Drugs Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Oncology Drugs Market Introduction

- Middle East & Africa Oncology Drugs Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Therapy Type

- By Drug Class

- By Cancer Type

- By Dosage Form

- By Distribution Channel

- By Country

- South Africa

- UAE

- Saudi Arabia

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Oncology Drugs Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Oncology Drugs Market Introduction

- Latin America Oncology Drugs Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Therapy Type

- By Drug Class

- By Cancer Type

- By Dosage Form

- By Distribution Channel

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Oncology Drugs Market Product Mapping

- Global Oncology Drugs Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Oncology Drugs Market Tier Structure Analysis

- Global Oncology Drugs Market Concentration & Company Market Shares (%) Analysis, 2023

- Company Profiles

- Hoffmann-La Roche Ltd

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Hoffmann-La Roche Ltd

* Similar details would be provided for all the players mentioned below

- Bristol-Myers Squibb

- Johnson & Johnson

- Merck & Co.

- Pfizer

- AstraZeneca

- Novartis

- AbbVie

- Eli Lilly and Company

- Astellas Pharma

- GSK

- Sanofi

- Takeda Pharmaceutical

- Amgen

- Gilead Sciences

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

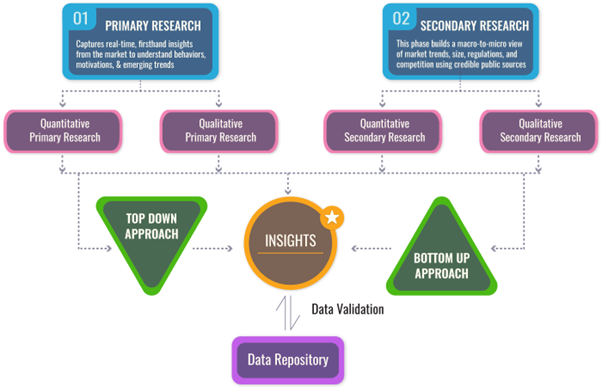

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables