Semiconductor Manufacturing Equipment Market Size And Forecast (2025 - 2033), Global And Regional Growth, Trend, Share And Industry Analysis Report Coverage: By Equipment Type (Front-End Equipment, Back-End Equipment, Other Equipment) By Dimension (2D, 2.5D, 3D) By Application (Semiconductor Fabrication Plant Or Foundry, Semiconductor Electronics Manufacturing, Other Applications) And Geography

2025-07-18

Semiconductor and Electronics

Description

Semiconductor Manufacturing Equipment Market Overview

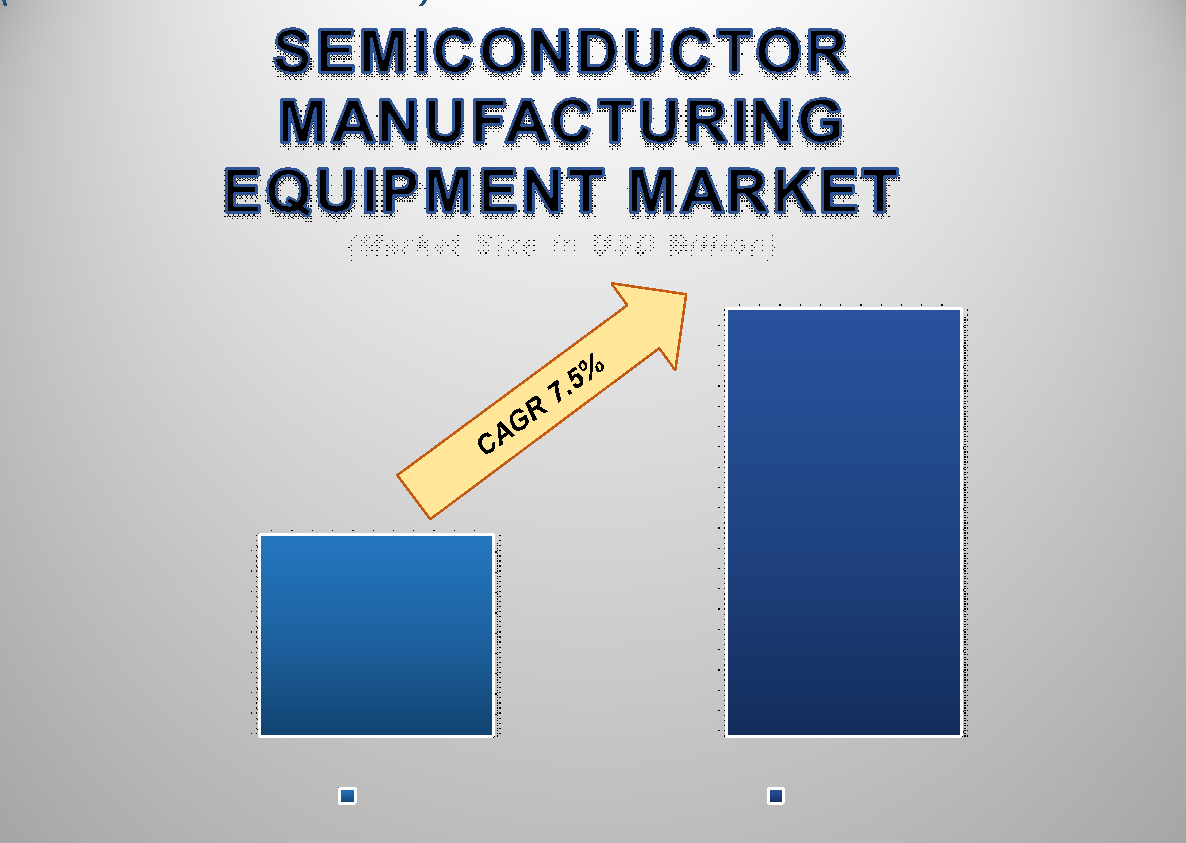

The global Semiconductor Manufacturing Equipment market size is projected to reach US$ 240.7 Billion by 2033 from US$ 113.6 Billion in 2025. The market is expected to register a CAGR of 7.5% from 2025–2033. This growth is primarily driven by the increasing demand for advanced semiconductor devices across various sectors, including consumer electronics, automotive, telecommunications, and industrial automation.

Semiconductor manufacturing equipment is the machinery and tools employed in the fabrication and assembly of semiconductor chips, which are the pillars of contemporary electronics. The industry is developing at a fast rate, with advancements in lithography, wafer processing, and packaging equipment contributing to increased efficiency and chip miniaturization. One of the major factors fueling the growth in the market is the increase in the need for high-performance computing and memory chips, which is encouraging semiconductor companies to increase their manufacturing capacity. The move towards narrower nodes, including 5nm and 3nm nodes, also requires heavy investment in the latest manufacturing equipment that is more sophisticated and uses more capital. In addition, geopolitical factors and the need for semiconductor self-sufficiency are causing heavy investments in semiconductor fabrication facilities in nations such as the United States, China, South Korea, and Taiwan. This is leading to heavy capital outlays from both governmental and private entities to make new semiconductor fabrication plants and upgrade existing facilities.

Semiconductor Manufacturing Equipment Market Drivers and Opportunities

Rising demand for advanced semiconductor devices across key industries is anticipated to lift the semiconductor manufacturing equipment market

The growth in consumer electronics, automotive, telecommunication, and manufacturing industries is fueling tremendous semiconductor manufacturing equipment demand. With rising dependence on semiconductors to facilitate functions in smartphones, notebooks, smart home appliances, electric vehicles (EVs), and 5G networks, the market is increasingly demanding highly efficient and accurate manufacturing equipment. Advanced semiconductors are also a central component in the technologies of artificial intelligence (AI), machine learning (ML), and edge computing, further fueling equipment requirements. While chip manufacturers battle to match performance and miniaturization demands, the industry is witnessing increasing investment in state-of-the-art equipment such as EUV (extreme ultraviolet) lithography machines, sophisticated etching instruments, and wafer cleaning equipment. Players such as TSMC, Intel, and Samsung are expanding their facilities across the world with the help of government incentives, giving the equipment buying process a strong pipeline. Also, increasing chip usage in electric vehicles, autonomous car systems, and renewable energy infrastructure further broadened the use scope. All these, coupled with the worldwide digital transformation movement, are compelling semiconductor manufacturers to enhance their capacities as well as install next-gen equipment. This ongoing boom across industries is a critical factor propelling the market into growth.

Government initiatives and strategic investments in semiconductor manufacturing is a vital driver for influencing the growth of the global semiconductor manufacturing equipment market

Governments all over the world are increasingly viewing semiconductors as a strategic resource, with large-scale policy initiatives and funding to drive domestic chip manufacturing. The likes of the U.S. CHIPS and Science Act, the European Union's Chips Act, and China's "Made in China 2025" are designed to establish robust semiconductor supply chains and cut dependence on foreign suppliers. The policy action is translating into heavy investment in new fabrication plants (fabs), which is directly favors the semiconductor manufacturing equipment industry. For example, the U.S. is providing billions in incentives and tax breaks to convince semiconductor manufacturers to establish fabs in the country, which encouraged the likes of Intel, TSMC, and GlobalFoundries to make large capital announcements. South Korea and Taiwan are continuing to dominate overall semiconductor spending, and emerging economies like India and Vietnam are increasing their manufacturing infrastructure. The national plans also include workforce upskilling and private-sector engagement, further underpinning longer-term growth prospects. With such strategic support and growing geopolitical focus on chip sovereignty, semiconductor equipment vendors are poised for long-range business opportunities related to infrastructure build-out and capacity augmentation globally.

Growth in semiconductor packaging and testing equipment is poised to create significant opportunities in the global semiconductor manufacturing equipment market

The development of chip design and integration, in the form of system-in-package (SiP), 2.5D, and 3D packaging, is creating new growth prospects in the semiconductor manufacturing equipment industry. With decreasing device form factors and increasing performance requirements, conventional planar packaging technologies are giving way to advanced packaging technologies that provide enhanced power management, thermal performance, and interconnect densities. The transition is fueling the need for wafer-level packaging, flip-chip bonding, and fan-out packaging equipment. Also, with chips becoming increasingly complex, there is a growing need for advanced testing solutions that guarantee reliability, signal integrity, and yield optimization. The backend process of semiconductor manufacturing—previously a less technology-intensive process—is now experiencing high-value investments and technology advancements. Backend equipment makers are seizing the moment by creating machines that deliver support for heterogeneous integration, advanced metrology, and AI-driven testing. With automotive, aerospace, and healthcare industries demanding fail-proof electronics, the packaging and testing functions are becoming more strategically critical. Therefore, the need for equipment in this space is anticipated to increase substantially during the forecast period.

Semiconductor Manufacturing Equipment Market Scope

Semiconductor Manufacturing Equipment Market Report Segmentation Analysis

The global semiconductor manufacturing equipment market industry analysis is segmented by equipment type, by dimension, by application, and by region.

The front-end equipment segment is anticipated to hold the highest share of the global semiconductor manufacturing equipment market during the projected timeframe

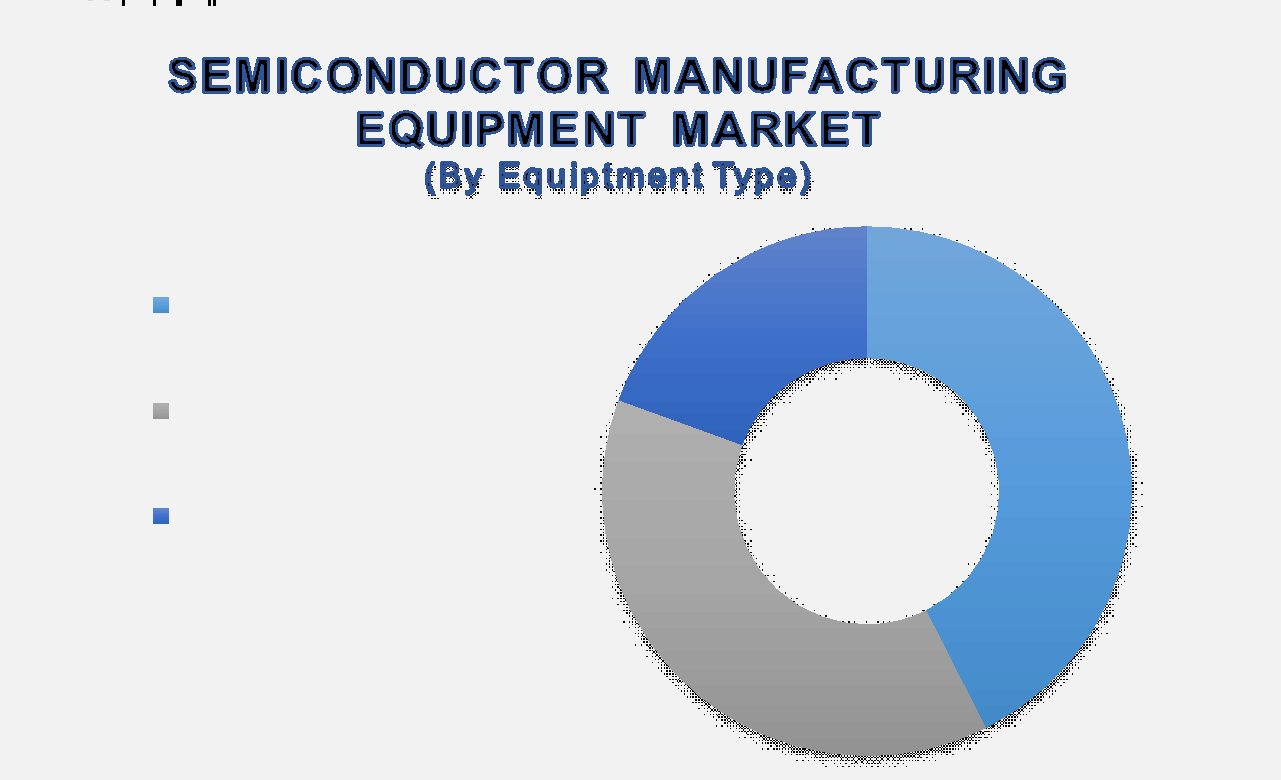

By equipment type, the market is divided into Front-end Equipment, Back-end Equipment, and Other Equipment. Among them, the Front-end Equipment segment is expected to have the largest share of 42.6% in the semiconductor manufacturing equipment industry. The growth is induced by the increasing need for precise tools used in the wafer fabrication process, including photolithography, etching, doping, and deposition. The movement of nodes to the sub-5nm region is further enhancing the usage of very advanced front-end technologies like ion implantation (e.g., EUV) and photolithography.

The 3D segment is anticipated to hold the highest share of the market over the forecast period

By Dimension, the market is divided based on 2D, 2.5D, and 3D semiconductor devices. The 3D sector is anticipated to dominate the market during the forecast period, with the largest share, owing to the trend towards space-saving and performance-driven chip designs. 3D integration technologies such as 3D NAND and 3D ICs are becoming increasingly used as they can place multiple circuit planes stacked together in a single chip, resulting in faster speed, power savings, and capacity for data. The latter are critical for applications in AI, big data, high-performance computing (HPC), and smartphones, which call for both density and performance optimization.

The semiconductor fabrication plant or foundry segment dominated the market in 2024 and is predicted to grow at the highest CAGR over the forecast period

By Application, the market is divided into Semiconductor Fabrication Plant or Foundry, Semiconductor Electronics Manufacturing, and Other Applications. The Semiconductor Fabrication Plant or Foundry dominated the market in the year 2024 and will register the highest CAGR during the forecast period. The leadership of the segment is a result of aggressive capacity additions and modernization by world-class foundries like TSMC, Samsung Foundry, and Intel. The plants are used for the fabrication of a vast array of chips for consumer electronics, automotive, industrial, and telecom applications.

The following segments are part of an in-depth analysis of the global Semiconductor Manufacturing Equipment market:

Semiconductor Manufacturing Equipment Market Share Analysis by Region

North America is projected to hold the largest share of the global semiconductor manufacturing equipment market over the forecast period

Asia Pacific was the leading region in the semiconductor manufacturing equipment market globally, with a 42.5% share of the overall market in 2024. The region benefits from the presence of semiconductor manufacturing centers like South Korea, China, Japan, and Taiwan as the hub for leading integrated device manufacturers like Samsung, TSMC, and SMIC. The region continues to invest heavily in increasing wafer fabrication capacity as well as upgrading production equipment to accommodate advanced nodes of technology, which are especially lower than 5nm. The region is bolstered by the presence of a developed electronics ecosystem, semiconductor incentive schemes supported by the government, as well as access to a professional labor pool. The region also draws advantages from the electronics manufacturing and consumption hub, which facilitates additional spending in the form of high-quality lithography, deposition, and etching tools as a result of growing needs for smartphones, automotive electronics, and consumer devices. The region is also seeing growing capabilities in domestic equipment manufacturing, especially from China, as it plans to decrease dependence on foreign tools, as well as enhance semiconductor supply chain resilience.

Concurrently, North America is also anticipated to have the highest CAGR over the forecast period, spurred by incentives from the government and the private sector to shore up domestic chip manufacturing. The CHIPS and Science Act in the United States is spurring large capacity additions and prompting global equipment suppliers to expand their presence in the region. Top semiconductor manufacturers are setting up new fabrication facilities and world-class R&D centers, further generating demand for advanced manufacturing equipment. The focus of the region for next-generation computing technologies like AI, quantum computing, and 5G is also leading to equipment advancements, supporting North America's increasing presence in the global semiconductor industry.

Semiconductor Manufacturing Equipment Market Competition Landscape Analysis

Global semiconductor manufacturing equipment market is marked by robust competition among key players focusing on innovation, strategic expansion, and sustainability. Continuous research and development efforts lead to the introduction of advanced semiconductor manufacturing equipment with improved performance characteristics, catering to evolving industry demands.

Global Semiconductor Manufacturing Equipment Market Recent Developments News:

In June 2024, ASML announced its next-generation Hyper-NA EUV lithography system, targeting a numerical aperture (NA) of 0.75 by around 2030. This breakthrough would enable semiconductor patterning at an unprecedented ~0.2 nm (2 angstrom) scale, far surpassing current High-NA EUV (0.55 NA) capabilities. By allowing significantly finer transistor features and higher chip density, Hyper-NA could extend Moore’s Law for another decade, reinforcing ASML’s leadership in advanced chip manufacturing.

In December 2024, KLA Corporation enhanced its IC substrate product portfolio to address critical challenges in advanced packaging, including connectivity, yield, and miniaturization.

The Global Semiconductor Manufacturing Equipment Market is dominated by a few large companies, such as

Applied Materials Inc

Tokyo Electron Limited

Lam Research Corporation

ASML

Dainippon Screen Group

KLA Corporation

Ferrotec Holdings Corporation

Hitachi High-Technologies Corporation

ASM International

Canon Machinery Inc

Others

Frequently Asked Questions

- Global Semiconductor Manufacturing Equipment Market Introduction and Market Overview

-

- Objectives of the Study

- Global Semiconductor Manufacturing Equipment Market Scope and Market Estimation

- Global Semiconductor Manufacturing Equipment Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Semiconductor Manufacturing Equipment Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2020 - 2033

- Market Segmentation

- Equipment Type of Global Semiconductor Manufacturing Equipment Market

- Dimension of Global Semiconductor Manufacturing Equipment Market

- Application of Global Semiconductor Manufacturing Equipment Market

- Region of Global Semiconductor Manufacturing Equipment Market

- Executive Summary

-

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Semiconductor Manufacturing Equipment Market

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Semiconductor Manufacturing Equipment Market Estimates & Historical Trend Analysis (2020 - 2024)

-

- Global Semiconductor Manufacturing Equipment Market Estimates & Forecast Trend Analysis, by Equipment Type

- Global Semiconductor Manufacturing Equipment Market Revenue (US$ Bn) Estimates and Forecasts, by Equipment Type, 2020 - 2033

- Front-end Equipment

- Silicon Wafer Manufacturing

- Wafer Processing Equipment

- Back-end Equipment

- Testing Equipment

- Assembling and Packaging Equipment

- Other Equipment

- Global Semiconductor Manufacturing Equipment Market Estimates & Forecast Trend Analysis, by Dimension

- Global Semiconductor Manufacturing Equipment Market Revenue (US$ Bn) Estimates and Forecasts, by Dimension, 2020 - 2033

- 2D

- 2.5D

- 3D

- Global Semiconductor Manufacturing Equipment Market Estimates & Forecast Trend Analysis, by Application

-

- Global Semiconductor Manufacturing Equipment Market Revenue (US$ Bn) Estimates and Forecasts, by Application, 2020 - 2033

- Semiconductor Fabrication Plant or Foundry

- Semiconductor Electronics Manufacturing

- Other Applications

- Global Semiconductor Manufacturing Equipment Market Estimates & Forecast Trend Analysis, by Region

-

- Global Semiconductor Manufacturing Equipment Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2020 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- North America Semiconductor Manufacturing Equipment Market: Estimates & Forecast Trend Analysis

-

- North America Semiconductor Manufacturing Equipment Market Assessments & Key Findings

- North America Semiconductor Manufacturing Equipment Market Introduction

- North America Semiconductor Manufacturing Equipment Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Equipment Type

- By Dimension

- By Application

- By Country

- The U.S.

- Canada

- Europe Semiconductor Manufacturing Equipment Market: Estimates & Forecast Trend Analysis

-

- Europe Semiconductor Manufacturing Equipment Market Assessments & Key Findings

- Western Europe Semiconductor Manufacturing Equipment Market Introduction

- Western Europe Semiconductor Manufacturing Equipment Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Equipment Type

- By Dimension

- By Application

- By Country

- Germany

- Italy

- U.K.

- France

- Spain

- Switzerland

-

- Rest of Europe

- Asia Pacific Semiconductor Manufacturing Equipment Market: Estimates & Forecast Trend Analysis

-

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Semiconductor Manufacturing Equipment Market Introduction

- Asia Pacific Semiconductor Manufacturing Equipment Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Equipment Type

- By Dimension

- By Application

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East & Africa Semiconductor Manufacturing Equipment Market: Estimates & Forecast Trend Analysis

-

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Semiconductor Manufacturing Equipment Market Introduction

- Middle East & Africa Semiconductor Manufacturing Equipment Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Equipment Type

- By Dimension

- By Application

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Latin America Semiconductor Manufacturing Equipment Market: Estimates & Forecast Trend Analysis

-

- Latin America Market Assessments & Key Findings

- Latin America Semiconductor Manufacturing Equipment Market Introduction

- Latin America Semiconductor Manufacturing Equipment Market Size Estimates and Forecast (US$ Billion) (2020 - 2033)

- By Equipment Type

- By Dimension

- By Application

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Country Wise Market: Introduction

- Competition Landscape

-

- Global Semiconductor Manufacturing Equipment Market Product Mapping

- Global Semiconductor Manufacturing Equipment Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Semiconductor Manufacturing Equipment Market Tier Structure Analysis

- Global Semiconductor Manufacturing Equipment Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

-

- Applied Materials Inc

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

* Similar details would be provided for all the players mentioned below

- Tokyo Electron Limited

- Lam Research Corporation

- ASML

- Dainippon Screen Group

- KLA Corporation

- Ferrotec Holdings Corporation

- Hitachi High-Technologies Corporation

- ASM International

- Canon Machinery Inc

- Others

- Research Methodology

-

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

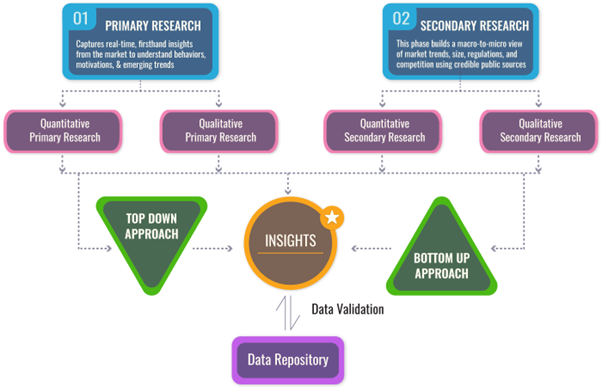

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables