Smart Factory Market Size And Forecast (2025 - 2033), Global And Regional Growth, Trend, Share And Industry Analysis Report Coverage: By Components (Industrial Sensors, Industrial Robots, Industrial 3D Printing, Machine Vision), By Solution (SCADA, MES, Industrial Safety, PAM), By Process Industry (Oil & Gas, Chemicals, Pulp & Paper, Pharmaceuticals, Metals & Mining, Food & Beverages, Energy & Power, Others), By Discrete Industry (Automotive, Aerospace & Defense, Semiconductor & Electronics, Machine Manufacturing, Medical Devices, Others) And Geography

2025-07-18

Semiconductor and Electronics

Description

Smart Factory Market Overview

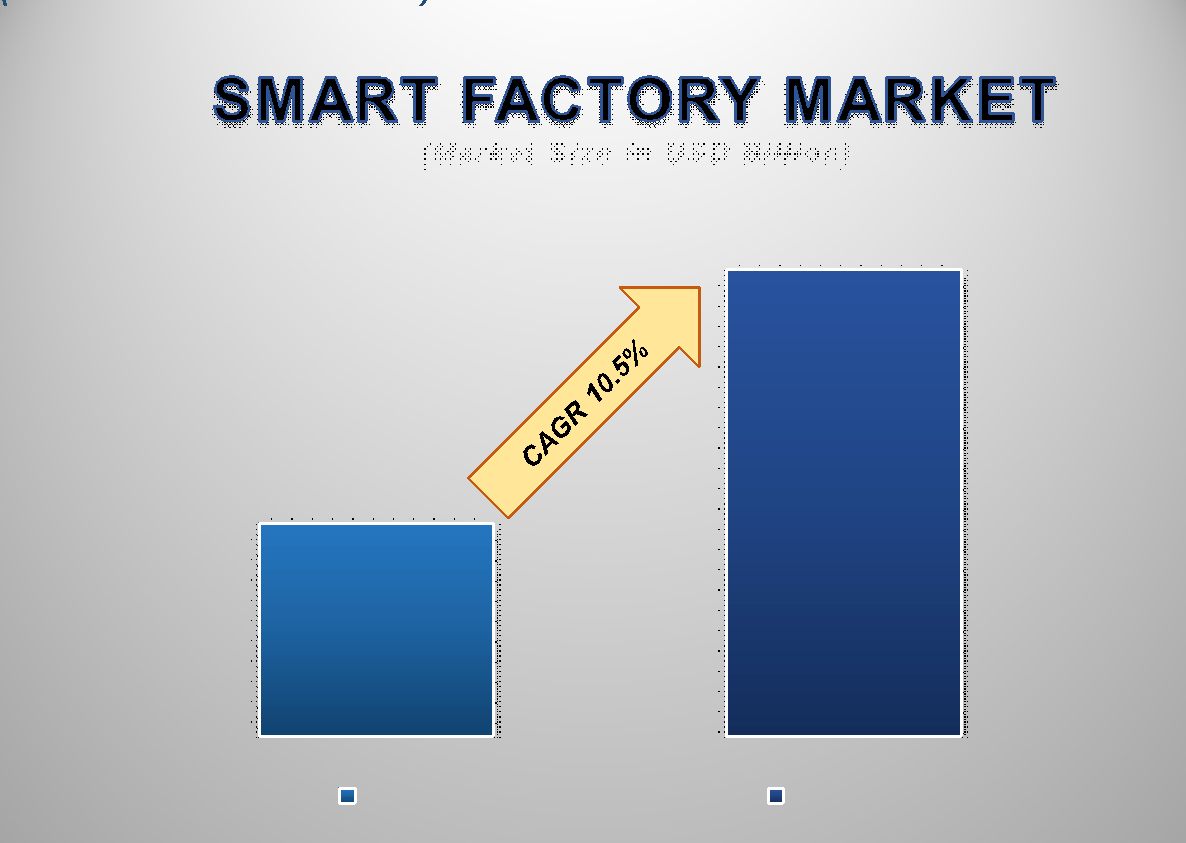

The global Smart Factory market is projected to reach US$524.7 Billion by 2033 from US$240.1 Billion in 2025. The market is expected to register a CAGR of 10.5% from 2025–2033. This growth is primarily driven by the integration of advanced technologies such as artificial intelligence (AI), the Internet of Things (IoT), robotics, big data analytics, and cloud computing into manufacturing systems.

A smart factory represents a fully connected and flexible system that can autonomously run production processes with minimal human intervention. This level of automation not only enhances operational efficiency but also improves product quality, reduces downtime, and lowers overall manufacturing costs. The key driving factors of this market are the rising adoption of smart manufacturing industry 4.0 principles by manufacturers worldwide. These principles emphasize digitization, connectivity, and smart automation, all of which are essential to compete in the modern industrial landscape. Additionally, the growing emphasis on energy efficiency and sustainable production processes is compelling companies to invest in smart factory technologies. The integration of cyber-physical systems and digital twins further enables real-time simulation and optimization, facilitating quicker decision-making and fault detection. With technological advancements and growing investment in R&D, the forecasted market analysis projects significant expansion across all regions, making the smart factory landscape one of the most dynamic segments in the manufacturing and industrial automation sector.

Smart Factory Market Drivers and Opportunities

Rising demand for industrial automation to improve productivity and efficiency is anticipated to lift the smart factory market during the forecast period

One of the primary drivers fueling the growth of the global smart factory market is the escalating demand for industrial automation to enhance productivity and operational efficiency. As industries become more competitive and globalized, manufacturers are under constant pressure to optimize production cycles, reduce downtime, and increase throughput. Smart factories leverage a combination of advanced technologies such as AI, IoT, robotics, and big data analytics to automate processes and minimize human intervention. This not only leads to faster production but also ensures greater accuracy, reduced errors, and lower operational costs. The adoption of automated systems allows for predictive maintenance, real-time monitoring, and adaptive production planning, which together result in better resource utilization and improved efficiency. Furthermore, automation helps in reducing workplace injuries by eliminating the need for human involvement in hazardous tasks. With growing awareness of the benefits, industries such as automotive, electronics, pharmaceuticals, and food & beverages are rapidly transitioning to smart factory frameworks. As a result, the market size for smart factories is forecasted to witness substantial growth, driven by the compelling need for streamlined and efficient manufacturing systems.

Supportive government initiatives for digital transformation in manufacturing is a vital driver for influencing the growth of the global smart factory market

Governments across the globe are launching initiatives to promote the digital transformation of manufacturing sectors, which is significantly driving the smart factory market growth. Programs such as Industry 4.0 in Germany, Smart Manufacturing Leadership Coalition in the U.S., and Made in China 2025 aim to modernize industrial practices by integrating smart technologies. These initiatives encourage innovation through subsidies, tax benefits, and investment in R&D to support companies transitioning to digital manufacturing systems. Additionally, regulatory bodies are setting standards for automation, cybersecurity, and data integration, thereby creating a conducive environment for smart factory adoption. Emerging economies are also aligning with these digital transformation goals to enhance their global competitiveness. Such initiatives not only create demand for smart factory solutions but also ease the implementation process for manufacturers. With strong institutional support and growing investments in infrastructure and innovation, the market is expected to witness sustained growth during the forecasted period.

Rising adoption of cloud and edge computing in the smart manufacturing market is poised to create significant opportunities in the global smart factory market

The increasing adoption of cloud and edge computing technologies presents a major opportunity for the smart factory market. These technologies enable decentralized processing of data, allowing for faster decision-making and greater agility in operations. Cloud computing facilitates seamless integration of systems across different locations, real-time data sharing, and scalable storage for big data analytics. Meanwhile, edge computing enhances performance by processing data locally at the source, which is particularly important for time-sensitive manufacturing processes. The hybrid use of both cloud and edge platforms offers a flexible and cost-effective infrastructure for implementing smart factory applications such as AI-based quality inspection, predictive maintenance, and robotic process automation. Furthermore, cloud-based platforms support remote monitoring and control of manufacturing operations, which became especially critical during the COVID-19 pandemic. As businesses increasingly shift toward digital infrastructure, the integration of cloud and edge computing will become a key enabler of smart factory innovations, presenting long-term growth opportunities for solution providers and manufacturers alike.

Smart Factory Market Scope

Smart Factory Market Report Segmentation Analysis

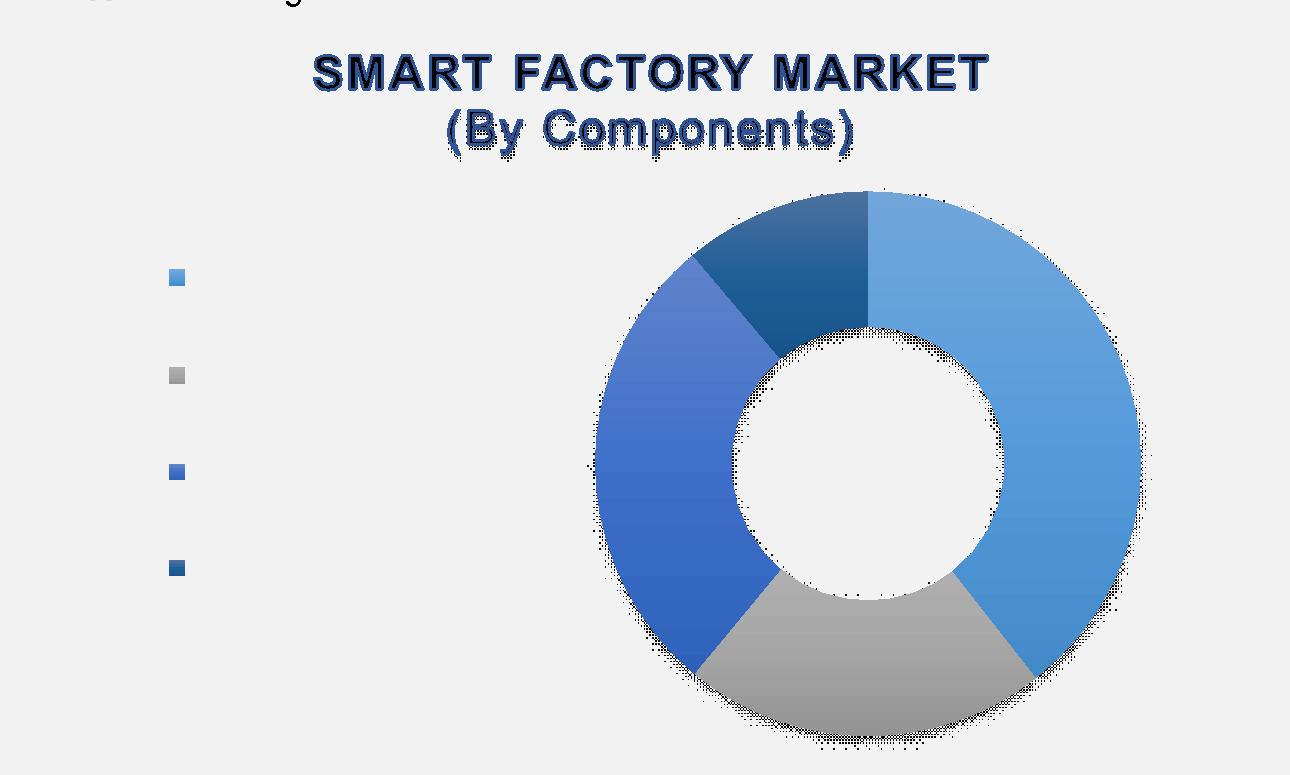

The Global Smart Factory Market industry analysis is segmented by Components, Solution, Process Industry, Discrete Industry, and by Region.

The Industrial Sensors segment is anticipated to hold the highest share of the global Smart Factory market during the projected timeframe

By Components, the market is segmented into Industrial Sensors, Industrial Robots, Industrial 3D Printing, and Machine Vision. In 2025, the Industrial Sensors segment is anticipated to hold the highest share of 39.4% in the global smart factory market during the projected timeframe. Industrial sensors are essential components in smart factories, enabling real-time data collection from machines, processes, and the environment. These sensors facilitate predictive maintenance, quality control, and efficient production by transmitting vital data to centralized systems. Their extensive use in monitoring temperature, pressure, proximity, motion, and flow across manufacturing units boosts their demand across industries like automotive, electronics, food & beverage, and metal & mining. With the rise in industrial automation, demand for sensors that support IoT integration and machine learning applications has accelerated, thereby contributing significantly to market growth.

The Manufacturing Execution Systems (MES) segment is anticipated to hold the highest share of the market over the forecast period

By Solution, the market is segmented into SCADA, Manufacturing Execution Systems (MES), Industrial Safety, and Plant Asset Management (PAM). The Manufacturing Execution Systems (MES) segment is anticipated to dominate the smart factory market throughout the forecast period. MES serves as a critical software layer that connects, monitors, and controls complex manufacturing systems and data flows on the factory floor. It plays a pivotal role in enabling real-time decision-making, production scheduling, quality management, and regulatory compliance. With manufacturers aiming for enhanced visibility, improved productivity, and reduced downtime, MES adoption has witnessed substantial growth.

The Metals & Mining segment dominated the market in 2024 and is predicted to grow at the highest CAGR over the forecast period

By Process Industry, the market is segmented into Oil & Gas, Chemicals, Pulp & Paper, Pharmaceuticals, Metals & Mining, Food & Beverages, Energy & Power, and Others. The Metals & Mining segment dominated the market in 2024 and is projected to grow at the highest CAGR over the forecast period. This industry's increasing adoption of automation and digital technologies is driven by the need to improve operational efficiency, worker safety, and environmental compliance. Smart factory solutions enable remote monitoring, predictive maintenance, and real-time control in hazardous and complex mining environments. In addition, the integration of IoT-enabled machinery, robotics, and analytics helps in resource optimization and cost management. The growing emphasis on digital transformation in this capital-intensive industry is expected to sustain its market dominance and growth trajectory.

The following segments are part of an in-depth analysis of the global Smart Factory market:

Smart Factory Market Share Analysis by Region

North America is projected to hold the largest share of the global Smart Factory market over the forecast period.

North America emerged as the dominant region in the global smart factory market, accounting for a substantial 40.5% market share in 2024. This dominance is primarily attributed to the region’s early and aggressive adoption of advanced manufacturing technologies such as artificial intelligence (AI), industrial Internet of Things (IIoT), and machine learning. The presence of key market players, robust industrial infrastructure, and high investments in digital transformation across sectors like automotive, aerospace, and consumer electronics are fueling the region's market size and growth. In addition, strong government support and favorable initiatives such as the “Advanced Manufacturing Partnership” in the United States are accelerating the deployment of smart factory solutions. The region's emphasis on energy efficiency, operational transparency, and real-time data analytics to enhance productivity and reduce downtime has further amplified the demand for smart automation systems.

Meanwhile, Asia Pacific is forecasted to grow at the highest CAGR over the forecast period. Rapid industrialization, expansion of manufacturing facilities, and increasing adoption of smart manufacturing industry 4.0 technologies in countries like China, Japan, South Korea, and India are key factors driving regional growth. Governments across the region are also launching digital manufacturing initiatives and infrastructure modernization programs to bolster smart industry capabilities. The growing demand for high-quality, cost-efficient, and scalable production solutions in this price-sensitive yet innovation-driven market is expected to solidify Asia Pacific’s position as the fastest-growing region in the global smart factory market landscape.

Smart Factory Market Competition Landscape Analysis

The global smart factory market features intense competition, with major players like General Electric, Emerson Electric, Honeywell International, and Rockwell Automation driving innovation and strategic growth. These industry leaders are expanding their capabilities by developing cutting-edge smart manufacturing solutions, leveraging advancements in AI, IoT, and automation. A strong emphasis on sustainability and operational efficiency further underscores their commitment to transforming traditional manufacturing into connected, intelligent ecosystems.

Global Smart Factory Market Recent Developments News:

In December 2023, Mitsubishi Electric India unveiled a state-of-the-art smart factory in Maharashtra’s Talegaon Industrial Area, dedicated to producing advanced Factory Automation Systems. The facility complies with global industry benchmarks, ensuring high-precision manufacturing of reliable automation products to meet growing industrial demand.

In November 2022, ABB Measurement & Analytics inaugurated its first smart instrumentation plant in Bangalore, featuring AI-driven production lines and IoT integration. The facility supports India’s "Make in India" initiative by delivering sustainable, precision-engineered solutions for global and domestic markets.

The Global Smart Factory Market is dominated by a few large companies, such as

ABB

Emerson Electric Co.

Siemens

Schneider Electric

Mitsubishi Electric Corporation

General Electric

Rockwell Automation, Inc.

Honeywell International Inc.

Yokogawa Electric Corporation

OMRON Corporation

Endress+Hauser

FANUC Corporation

WIKA

Dwyer Instruments, LLC.

Stratasys

3D Systems Corporation

Others

Frequently Asked Questions

- Global Smart Factory Market Introduction and Market Overview

- Objectives of the Study

- Global Smart Factory Market Scope and Market Estimation

- Global Smart Factory Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Smart Factory Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2033

- Market Segmentation

- Components of Global Smart Factory Market

- Solution of Global Smart Factory Market

- Process Industry of Global Smart Factory Market

- Discrete Industry of Global Smart Factory Market

- Region of Global Smart Factory Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Smart Factory Market

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Smart Factory Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global Smart Factory Market Estimates & Forecast Trend Analysis, by Components

- Global Smart Factory Market Revenue (US$ Bn) Estimates and Forecasts, by Components, 2021 - 2033

- Industrial Sensors

- Industrial Robots

- Industrial 3D Printing

- Machine Vision

- Global Smart Factory Market Estimates & Forecast Trend Analysis, by Solution

- Global Smart Factory Market Revenue (US$ Bn) Estimates and Forecasts, by Solution, 2021 - 2033

- SCADA

- MES

- Industrial Safety

- PAM

- Global Smart Factory Market Estimates & Forecast Trend Analysis, by Process Industry

- Global Smart Factory Market Revenue (US$ Bn) Estimates and Forecasts, by Process Industry, 2021 - 2033

- Oil & Gas

- Chemicals

- Pulp & Paper

- Pharmaceuticals

- Metals & Mining

- Food & Beverages

- Energy & Power

- Others

- Global Smart Factory Market Estimates & Forecast Trend Analysis, by Discrete Industry

- Global Smart Factory Market Revenue (US$ Bn) Estimates and Forecasts, by Discrete Industry, 2021 - 2033

- Automotive

- Aerospace & Defense

- Semiconductor & Electronics

- Machine Manufacturing

- Medical Devices

- Others

- Global Smart Factory Market Estimates & Forecast Trend Analysis, by Region

- Global Smart Factory Market Revenue (US$ Bn) Estimates and Forecasts, by Region, 2021 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- North America Smart Factory Market: Estimates & Forecast Trend Analysis

- North America Smart Factory Market Assessments & Key Findings

- North America Smart Factory Market Introduction

- North America Smart Factory Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Components

- By Solution

- By Process Industry

- By Discrete Industry

- By Country

- The U.S.

- Canada

- Europe Smart Factory Market: Estimates & Forecast Trend Analysis

- Europe Smart Factory Market Assessments & Key Findings

- Europe Smart Factory Market Introduction

- Europe Smart Factory Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Components

- By Solution

- By Process Industry

- By Discrete Industry

- By Country

- Germany

- Italy

- U.K.

- France

- Spain

- Switzerland

- Rest of Europe

- Asia Pacific Smart Factory Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Smart Factory Market Introduction

- Asia Pacific Smart Factory Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Components

- By Solution

- By Process Industry

- By Discrete Industry

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East & Africa Smart Factory Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Smart Factory Market Introduction

- Middle East & Africa Smart Factory Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Components

- By Solution

- By Process Industry

- By Discrete Industry

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Latin America Smart Factory Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Smart Factory Market Introduction

- Latin America Smart Factory Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Components

- By Solution

- By Process Industry

- By Discrete Industry

- By Country

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- Country Wise Market: Introduction

- Competition Landscape

- Global Smart Factory Market Product Mapping

- Global Smart Factory Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Smart Factory Market Tier Structure Analysis

- Global Smart Factory Market Concentration & Company Market Shares (%) Analysis, 2024

- Company Profiles

- ABB

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

* Similar details would be provided for all the players mentioned below

- Emerson Electric Co.

- Siemens

- Schneider Electric

- Mitsubishi Electric Corporation

- General Electric

- Rockwell Automation, Inc.

- Honeywell International Inc.

- Yokogawa Electric Corporation

- OMRON Corporation

- Endress+Hauser

- FANUC Corporation

- WIKA

- Dwyer Instruments, LLC.

- Stratasys

- 3D Systems Corporation

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

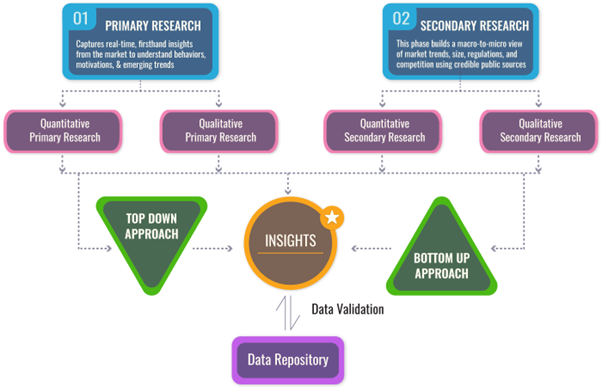

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables