Smoke Detector Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Detector Type (Photoelectric Smoke Detectors, Ionization Smoke Detectors, Dual-sensor Smoke Detectors, Aspirating Smoke Detector and Others); By Power Source (Battery-powered Smoke Detectors, Hardwired Smoke Detectors, Wireless Interconnected Smoke Detectors and Others); By End-user (Commercial, Industrial and Residential) and Geography

2025-07-15

ICT

Description

Smoke Detector Market

Overview

The Smoke Detector Market is

projected to witness significant growth between 2025 and 2033, primarily driven

by rising government initiatives and regulatory mandates requiring smoke

detector installations in residential and commercial buildings. Valued at

around USD 2.3 billion in 2025, the market is expected to expand to USD 4.62

billion by 2033, reflecting a strong compound annual growth rate (CAGR) of 8.0%

throughout the forecast period.

A smoke detector is a device

designed to sense the presence of smoke, typically as an early warning sign of

fire. It operates using either optical (photoelectric) technology or physical

(ionization) processes—or a combination of both for enhanced detection. In

addition to fire safety, highly sensitive detectors can be employed to identify

and prevent smoking in restricted areas.

In large commercial and

industrial settings, smoke detectors are often integrated into centralized fire

alarm system market. These detectors, whether conventional or addressable, are

connected to fire alarm control panels that manage the overall alert system.

Compared to battery-powered standalone residential smoke alarms, these

commercial detectors are generally more expensive and offer greater

functionality. They are commonly installed in commercial buildings, factories,

ships, and trains, and are occasionally included in residential security

systems to provide comprehensive fire protection.

Aspirating Smoke Detectors (ASDs)

are increasingly being adopted as part of advanced fire safety systems due to

their high sensitivity and early detection capabilities. These high-tech

devices continuously draw air from various locations through a network of

small, flexible pipes. The collected air is then analyzed for tiny smoke

particles, allowing for rapid identification of potential fire hazards, often

before the smoke becomes visible.

Unlike traditional detectors,

ASDs do not rely on passive airflow within a room, making them especially

effective in challenging environments. They are ideal for areas with high air

circulation, condensation, or where ultra-early detection is critical, such as

server rooms, data centers, and other mission-critical infrastructure. Their

precision and reliability make aspirating systems a preferred choice for

ensuring maximum fire safety in complex or sensitive settings.

Smart Smoke Detector

Market Drivers and Opportunities

Rising Fire Safety Awareness and Smart Home Adoption Fuel Global Smoke

Detector Market Growth

A major driver behind the

expansion of the global smoke detector market is the growing public awareness

of fire safety, coupled with the rapid adoption of smart home technologies.

Each year, fire-related incidents lead to significant injuries, fatalities, and

property loss, prompting individuals and households to prioritize preventive

safety measures. As awareness increases, particularly regarding the dangers of

nighttime residential fires, more homeowners are opting for advanced smoke

detection systems that offer greater reliability and performance than

traditional standalone alarms.

At the same time, the

proliferation of smart homes is reshaping consumer expectations around safety

and automation. Modern smoke detectors are now integrated with IoT platforms,

offering capabilities such as remote monitoring, voice alerts, real-time mobile

notifications, and even direct links to emergency responders. This level of

connectivity improves both responsiveness and user convenience. Tech-savvy

consumers are increasingly choosing smart smoke detectors that seamlessly

integrate with other smart home devices, including security systems, lighting,

and climate controls. In response, manufacturers are innovating with

multifunctional detectors that not only identify smoke but also monitor for

carbon monoxide and indoor air quality, adding further value to their products.

Stringent Government Regulations and Building Codes is anticipated to

lift the Smoke Detector Market during the forecast period

One of the key drivers of the

smoke detector market is the enforcement of strict government regulations and

fire safety building codes worldwide. Regulatory bodies like the National Fire

Protection Association (NFPA) in the U.S. and the European Committee for

Standardization (CEN) have made smoke detector installation mandatory in

residential, commercial, and industrial buildings. These regulations often

dictate the type, placement, and number of detectors required, pushing

developers and property owners to comply. In developed nations, new

constructions must include hardwired or battery-powered smoke alarms by law. In

developing countries, rapid urbanization and efforts to improve public safety

are accelerating the adoption of fire safety standards. Compliance is

especially critical in high-risk sectors such as healthcare, education,

hospitality, and manufacturing, where non-adherence can result in legal

penalties, financial losses, and reputational harm. Consequently, builders and

facility managers prioritize the integration of advanced fire safety systems in

their infrastructure plans.

Opportunity for the Smoke Detector Market

Growth in Emerging Markets and Urban Infrastructure Development is

significant opportunities in the global Smoke Detector Market

A significant growth opportunity

in the global smoke detector market lies in the rapid urbanization and

infrastructure development across emerging regions such as Asia-Pacific, Latin

America, the Middle East, and Africa. Countries like India, China, Brazil, and

Indonesia are experiencing a surge in residential, commercial, and industrial

construction, driving the need for enhanced fire safety measures. As these

nations build new urban centers and expand housing and commercial spaces, the

demand for fire detection systems is rising accordingly.

Governments in these regions are

becoming more proactive in enforcing fire safety regulations, particularly in

densely populated urban areas where fire risks are higher. At the same time,

rising incomes, a growing middle class, and increasing awareness of safety are

prompting both consumers and businesses to invest in modern fire protection

solutions. This presents a major opportunity for global and regional

manufacturers to enter these relatively untapped markets with affordable,

scalable, and easy-to-install smoke detection systems.

Smoke Detector Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 2.3 Billion |

|

Market Forecast in 2033 |

USD 4.62 Billion |

|

CAGR % 2025-2033 |

8.0% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP |

Production, Consumption, company share, company heatmap, company

production Capacity, growth factors and more |

|

Segments Covered |

●

By Detector Type ●

By Power Source ●

By End-user |

|

Regional Scope |

●

North America ●

Europe ●

APAC ●

Latin America ●

Middle East and Africa |

|

Country Scope |

1)

U.S. 2)

Canada 3)

Germany 4)

UK 5)

France 6)

Spain 7)

Italy 8)

Switzerland 9)

China 10)

Japan 11)

India 12)

Australia 13)

South Korea 14)

Brazil 15)

Mexico 16)

Argentina 17)

South Africa 18)

Saudi Arabia 19) UAE |

Smoke Detector Market Report Segmentation Analysis

The global Smoke Detector Market

industry analysis is segmented by detector type, by Power Source, by End-user,

and by region.

The Photoelectric Smoke Detectors segment is anticipated to hold the

highest share of the global Smoke Detector Market during the projected

timeframe.

The photoelectric smoke detector

segment is projected to hold the largest share of the global smoke detector

market during the forecast period, primarily due to its high efficiency in

detecting slow-smoldering fires, common in both residential and commercial

settings. Utilizing light beam and sensor technology, these detectors trigger

an alarm when airborne particles scatter the light beam, enabling early

detection of fires that produce heavy smoke before bursting into flames.

As awareness of fire safety

increases across households and businesses, there is a growing preference for

photoelectric detectors over ionization-based models. This shift is driven by

their superior sensitivity and reduced likelihood of false alarms. Additionally,

fire safety regulations in various countries are increasingly mandating or

recommending photoelectric smoke detectors due to these advantages. The

combination of enhanced performance, regulatory support, and growing demand for

early-warning systems makes photoelectric technology the leading choice in the

evolving smoke detector market.

Technological developments, like

compatibility with smart home systems as well as advancements in the

development of dual-sensor detectors (a combination of photoelectric and

ionization technologies), have also contributed towards this growing adoption of

this segment. Growing emphasis on reduction of fire risk as well as enhancement

of early detection in both developed as well as developing countries is driving

market demand.

The Hardwired power source segment is anticipated to hold the highest

share of the market over the forecast period.

The hardwired power source

segment is expected to dominate the smoke detector market during the forecast

period, driven by its superior reliability, safety, and extensive application

in both new constructions and renovation projects. Unlike standalone battery-powered

units, hardwired smoke detectors are directly connected to a building’s

electrical system and typically include a backup battery to ensure

functionality during power outages. This dual-power setup enhances their

dependability, making them ideal for critical environments.

Hardwired detectors are

especially preferred in commercial, industrial, and modern residential

buildings, where building codes frequently mandate interconnected alarm

systems. These interconnected systems enable detectors to communicate with each

other—if one unit detects smoke, all alarms throughout the property are

activated. This synchronized response significantly improves alert speed and

coverage, offering greater protection and reducing emergency response times. As

a result, hardwired smoke detectors are becoming the standard for comprehensive

fire safety in a wide range of settings.

The Industrial application segment dominated the market in 2024 and is

predicted to grow at the highest CAGR over the forecast period.

The industrial applications

segment dominated the global smoke detector market in 2024 and is projected to

grow at the highest compound annual growth rate (CAGR) throughout the forecast

period. This growth is driven by stricter safety regulations, heightened fire

risk awareness, and rising demand for efficient fire detection systems in

large-scale facilities. Industries such as manufacturing, mining, chemicals,

energy, and oil & gas face elevated fire risks due to the presence of

flammable materials, complex machinery, and harsh operating environments.

As a result, there is a growing

need for advanced smoke detection technologies that can perform reliably in

challenging conditions. Industrial settings require robust detectors with

features like early fire detection, heat resistance, and seamless integration

with broader safety and automation systems. Regulatory mandates have further

compelled companies to invest in high-performance fire protection solutions.

Additionally, the high costs

associated with operational downtime, equipment damage, and potential loss of

life make reliable smoke detection essential. Increasingly, industries are

adopting intelligent, IoT-enabled detectors that offer real-time monitoring,

data analytics, and remote alerts, enhancing their capacity for proactive risk

management and disaster prevention.

The following segments are part of an in-depth analysis of the global

smoke detector market:

|

Market Segments |

|

|

By Detector Type

|

●

Photoelectric Smoke

Detectors ●

Ionization Smoke

Detectors ●

Dual-sensor Smoke

Detectors ●

Aspirating Smoke

Detector ●

Others |

|

By Power Source

|

●

Battery-powered

Smoke Detectors ●

Hardwired Smoke

Detectors ●

Wireless

Interconnected Smoke Detectors ●

Others |

|

By End-user |

●

Commercial ●

Industrial ●

Residential |

Smoke Detector Market

Share Analysis by Region

North America is projected to hold the largest share of the global

Smoke Detector Market over the forecast period.

North America is expected to hold

the largest share of the global smoke detector market during the forecast

period, driven by strict regulatory standards, widespread fire safety

awareness, and strong adoption of advanced detection technologies. Regulations

such as NFPA codes in the U.S. and similar mandates in Canada require smoke

detector installation across residential, commercial, and industrial spaces.

High consumer awareness and frequent upgrades to smart, IoT-integrated

detectors—offering real-time alerts and remote monitoring—are further fueling

demand.

The presence of major players

like Honeywell, Johnson Controls, and Kidde, with robust R&D and

distribution networks, strengthens regional market growth. Additionally, rising

urbanization, ongoing construction, and the growing popularity of wireless and

battery-powered detectors contribute to the market's expansion. Incentives from

insurance companies for fire safety compliance, alongside active government

fire prevention initiatives, continue to promote the adoption of smoke

detection systems across North America.

Smoke Detector Market

Competition Landscape Analysis

The market is

competitive, with several established players and new entrants offering a range

of Smoke detector products. Some of the key players Honeywell International

Inc., Siemens AG, Johnson Controls, Schneider Electric, Robert Bosch GmbH, BRK

Brands, Inc. and others.

Global Smoke Detector

Market Recent Developments News:

- In January 2023, Siemens introduced two advanced

aspirating smoke detectors, the FDA261 and FDA262, specifically designed

for challenging fire safety environments that require extensive coverage,

such as large data centers, e-commerce warehouses, and industrial

facilities. Each unit is capable of monitoring areas up to 6,700 m²,

making them the detectors with the largest coverage capacity currently

available on the market.

- In March 2025, First Alert, a leading U.S. fire

safety brand under Resideo, announced a strategic partnership with Google

Home to enhance life safety through smart home integration. The newly

launched First Alert Smart Smoke & Carbon Monoxide Alarm is now

compatible with the Nest Protect system. This allows Nest users to

seamlessly integrate or upgrade their existing setup using the Google Home

app for enhanced and unified protection.

- In July 2023, Hikvision India launched a new line

of Standalone Smoke and Gas Detectors, including two models in the

photoelectric smoke detector range—HF-S2E Eco and NP-FY200—along with a

Carbon Monoxide Gas Detector, model HF-GM100, targeting the Indian market.

The Global Smoke Detector Market is dominated by a few large companies,

such as

●

Honeywell

International Inc.

●

Siemens AG

●

Johnson Controls

●

Schneider Electric

●

Robert Bosch GmbH

●

BRK Brands, Inc.

●

Hochiki Corporation

●

Nest Labs

●

Kidde

●

United Technologies

Corporation

●

ABB Ltd.

●

Panasonic Corporation

●

Huawei Technologies

Co., Ltd.

●

X-Sense

●

Mircom Technologies

Ltd.

● Other Prominent Players

Frequently Asked Questions

- Global Smoke Detector Market Introduction and Market Overview

- Objectives of the Study

- Global Smoke Detector Market Scope and Market Estimation

- Global Smoke Detector Market Overall Market Size (US$ Bn), Market CAGR (%), Market forecast (2025 - 2033)

- Global Smoke Detector Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 - 2033

- Market Segmentation

- Detector Type of Global Smoke Detector Market

- Power Source of Global Smoke Detector Market

- End-user of Global Smoke Detector Market

- Region of Global Smoke Detector Market

- Executive Summary

- Demand Side Trends

- Key Market Trends

- Market Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

- Demand and Opportunity Assessment

- Demand Supply Scenario

- Market Dynamics

- Drivers

- Limitations

- Opportunities

- Impact Analysis of Drivers and Restraints

- Emerging Trends for Smoke Detector Market

- Pricing Analysis

- Porter’s Five Forces Analysis

- PEST Analysis

- Key Regulation

- Global Smoke Detector Market Estimates & Historical Trend Analysis (2021 - 2024)

- Global Smoke Detector Market Estimates & Forecast Trend Analysis, by Detector Type

- Global Smoke Detector Market Revenue (US$ Bn) Estimates and Forecasts, by Detector Type, 2021 - 2033

- Photoelectric Smoke Detectors

- Ionization Smoke Detectors

- Dual-sensor Smoke Detectors

- Aspirating Smoke Detector

- Others

- Global Smoke Detector Market Revenue (US$ Bn) Estimates and Forecasts, by Detector Type, 2021 - 2033

- Global Smoke Detector Market Estimates & Forecast Trend Analysis, by Power Source

- Global Smoke Detector Market Revenue (US$ Bn) Estimates and Forecasts, by Power Source, 2021 - 2033

- Battery-powered Smoke Detectors

- Hardwired Smoke Detectors

- Wireless Interconnected Smoke Detectors

- Others

- Global Smoke Detector Market Revenue (US$ Bn) Estimates and Forecasts, by Power Source, 2021 - 2033

- Global Smoke Detector Market Estimates & Forecast Trend Analysis, by End-user

- Global Smoke Detector Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2021 - 2033

- Commercial

- Industrial

- Residential

- Global Smoke Detector Market Revenue (US$ Bn) Estimates and Forecasts, by End-user, 2021 - 2033

- Global Smoke Detector Market Estimates & Forecast Trend Analysis, by region

- Global Smoke Detector Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America

- Europe

- Asia Pacific

- Middle East & Africa

- Latin America

- Global Smoke Detector Market Revenue (US$ Bn) Estimates and Forecasts, by region, 2021 - 2033

- North America Smoke Detector Market: Estimates & Forecast Trend Analysis

- North America Smoke Detector Market Assessments & Key Findings

- North America Smoke Detector Market Introduction

- North America Smoke Detector Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Detector Type

- By Power Source

- By End-user

- By Country

- The U.S.

- Canada

- North America Smoke Detector Market Assessments & Key Findings

- Europe Smoke Detector Market: Estimates & Forecast Trend Analysis

- Europe Smoke Detector Market Assessments & Key Findings

- Europe Smoke Detector Market Introduction

- Europe Smoke Detector Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Detector Type

- By Power Source

- By End-user

- By Country

- Germany

- Italy

- K.

- France

- Netherland

- Rest of Europe

- Europe Smoke Detector Market Assessments & Key Findings

- Asia Pacific Smoke Detector Market: Estimates & Forecast Trend Analysis

- Asia Pacific Market Assessments & Key Findings

- Asia Pacific Smoke Detector Market Introduction

- Asia Pacific Smoke Detector Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Detector Type

- By Power Source

- By End-user

- By Country

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Asia Pacific Market Assessments & Key Findings

- Middle East & Africa Smoke Detector Market: Estimates & Forecast Trend Analysis

- Middle East & Africa Market Assessments & Key Findings

- Middle East & Africa Smoke Detector Market Introduction

- Middle East & Africa Smoke Detector Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Detector Type

- By Power Source

- By End-user

- By Country

- UAE

- Saudi Arabia

- South Africa

- Rest of MEA

- Middle East & Africa Market Assessments & Key Findings

- Latin America Smoke Detector Market: Estimates & Forecast Trend Analysis

- Latin America Market Assessments & Key Findings

- Latin America Smoke Detector Market Introduction

- Latin America Smoke Detector Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

- By Detector Type

- By Power Source

- By End-user

- By Country

- Brazil

- Mexico

- Argentina

- Rest of LATAM

- Latin America Market Assessments & Key Findings

- Country Wise Market: Introduction

- Competition Landscape

- Global Smoke Detector Market Product Mapping

- Global Smoke Detector Market Concentration Analysis, by Leading Players / Innovators / Emerging Players / New Entrants

- Global Smoke Detector Market Tier Structure Analysis

- Global Smoke Detector Market Concentration & Company Market Shares (%) Analysis, 2023

- Company Profiles

- Honeywell International Inc.

- Company Overview & Key Stats

- Financial Performance & KPIs

- Product Portfolio

- SWOT Analysis

- Business Strategy & Recent Developments

- Honeywell International Inc.

* Similar details would be provided for all the players mentioned below

- Siemens AG

- Johnson Controls

- Schneider Electric

- Robert Bosch GmbH

- BRK Brands, Inc.

- Hochiki Corporation

- Nest Labs

- Kidde

- United Technologies Corporation

- ABB Ltd.

- Panasonic Corporation

- Huawei Technologies Co., Ltd.

- X-Sense

- Mircoms Technologies Ltd.

- Other Prominent Players

- Research Methodology

- External Transportations / Databases

- Internal Proprietary Database

- Primary Research

- Secondary Research

- Assumptions

- Limitations

- Report FAQs

- Research Findings & Conclusion

Our Research Methodology

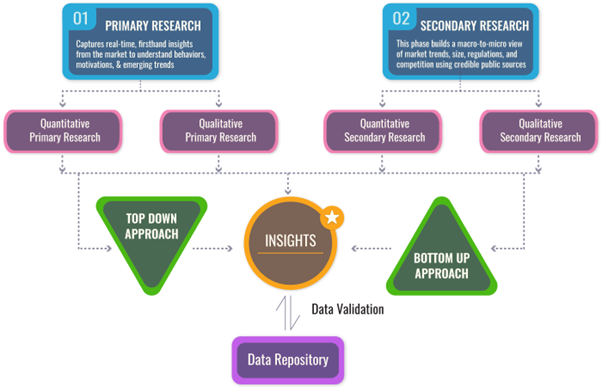

"Insight without rigor is just noise."

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables