Urban Air Mobility Market Size and Forecast (2025 - 2033), Global and Regional Growth, Trend, Share and Industry Analysis Report Coverage: By Vehicle Type (Air Taxis, Air Metros, Air Ambulance, Last-Mile Delivery, Others), By Range (Intercity, Intracity), By Operation (Piloted, Autonomous, Hybrid), By End User (Ridesharing Companies, Scheduled Operators, E-Commerce Companies, Hospitals and Medical Agencies, Private Operators); and Geography

2025-07-15

Aerospace & Defense

Description

Urban Air Mobility Market Overview

The global urban air mobility (UAM) market was valued at USD 5.4 billion in 2025 and is projected to reach approximately USD 29.7 billion by 2033, expanding at a compound annual growth rate (CAGR) of 16.5% during the forecast period. This significant growth reflects the increasing interest in innovative transportation technologies that address the challenges of urban congestion, environmental sustainability, and rapid on-demand mobility.

Urban air mobility refers to the use of electric or hybrid-electric aircraft, such as eVTOL (electric vertical take-off and landing) vehicles, for transporting passengers or cargo within and between urban areas. Key drivers fueling market growth include the surge in urbanization, advancements in battery and propulsion technologies, and strong investment from both the government and private sectors. Cities across North America, Europe, and Asia-Pacific are piloting air mobility projects to reduce travel time and emissions. Supportive government regulations, smart city initiatives, and increasing demand for faster and more flexible transportation options are further contributing to the market expansion. Current market trends highlight strategic collaborations between aerospace firms and tech startups, rising prototypes of autonomous air taxis, and integration of urban air traffic management systems. The commercial segment is gaining traction, particularly for applications in air taxis, last-mile delivery drones, and medical emergency transport. Moreover, UAM is positioned as a key component of future multimodal urban transport systems, complementing ground mobility solutions.

Urban Air Mobility Market Drivers and Opportunities

Technological Advancements in eVTOL Aircraft and Battery Systems are anticipated to lift the Urban Air Mobility Market during the forecast period

One of the most significant enablers of urban air mobility is the rapid advancement in electric vertical take-off and landing (eVTOL) technology. Innovations in propulsion systems, lightweight composite materials, battery efficiency, and autonomous flight software are making eVTOL aircraft increasingly viable for commercial use. These aircraft are designed to be quieter, more efficient, and environmentally friendly compared to traditional helicopters or airplanes. Improvements in lithium-ion batteries and power-dense energy storage systems have enhanced flight duration and load capacity, addressing earlier limitations in range and payload. Autonomous navigation systems and artificial intelligence are further refining UAM safety and operational consistency, reducing the need for human pilots. Major aerospace companies and startups are actively investing in R&D and prototype testing to create scalable, cost-effective, and regulatory-compliant vehicles. These advancements are drastically reducing barriers to entry, increasing investor confidence, and accelerating the commercialization timeline for UAM market services. As technology continues to evolve, it will play a pivotal role in shaping the long-term growth and competitiveness of the global UAM market.

Government Support and Regulatory Initiatives drive the global Urban Air Mobility Market Industry

Strong government support and favorable regulatory frameworks are accelerating the adoption of urban air mobility solutions. Aviation authorities such as the Federal Aviation Administration (FAA), European Union Aviation Safety Agency (EASA), and other national bodies are actively working on policy development, safety standards, and air traffic management frameworks tailored for UAM operations. Initiatives like the FAA's “Innovate28” plan, which aims to support scaled UAM operations by 2028, are illustrative of this commitment. Governments are also funding pilot projects, testing zones, and public-private partnerships to drive innovation and assess UAM viability. In many countries, urban planners are integrating UAM into future smart city blueprints, ensuring that skyports, charging stations, and unmanned traffic management (UTM) systems are part of urban development. Public acceptance is another focus area, and regulators are working on community outreach and noise standardization to minimize resistance. These concerted efforts create a conducive ecosystem that supports testing, certification, and eventual large-scale deployment. This strong regulatory backing not only legitimizes the technology but also significantly derisks investment, catalyzing growth in the UAM market forecast.

Opportunity for the Urban Air Mobility Market

Integration with Smart City Infrastructure is a significant opportunity in the global Urban Air Mobility Market

Urban air mobility offers a unique opportunity to be embedded within the broader framework of smart city development. Cities globally are evolving into smart ecosystems where infrastructure, data, and technology interact seamlessly to improve urban living. Integrating UAM into this environment can significantly enhance its value proposition. For instance, smart cities are already implementing intelligent traffic systems, IoT-enabled infrastructure, and data-driven urban planning—all of which can be extended to include aerial mobility. Skyports can be co-located with existing transportation hubs like metro stations, parking garages, or commercial centers to offer multimodal transport options. Additionally, data collected from UAM operations can feed into urban analytics platforms to optimize flight schedules, minimize noise footprints, and ensure safety. Governments and municipalities are increasingly receptive to the concept of three-dimensional transportation planning, and this provides a ripe environment for deploying UAM services in harmony with other urban systems. This integrated approach opens up not just technological but also commercial and civic planning opportunities, which can lead to long-term, scalable adoption of urban air mobility.

Urban Air Mobility Market Scope

|

Report Attributes |

Description |

|

Market Size in 2025 |

USD 5.4 Billion |

|

Market Forecast in 2033 |

USD 29.7 Billion |

|

CAGR % 2025-2033 |

16.5% |

|

Base Year |

2024 |

|

Historic Data |

2020-2024 |

|

Forecast Period |

2025-2033 |

|

Report USP

|

Production, Consumption, company share, company heatmap, company production Capacity, growth factors, and more |

|

Segments Covered |

● By Vehicle Type ● By Range ● By Operation ● By End User |

|

Regional Scope |

● North America ● Europe ● APAC ● Latin America ● Middle East and Africa |

|

Country Scope |

1) U.S. 2) Canada 3) Germany 4) UK 5) France 6) Spain 7) Italy 8) Switzerland 9) China 10) Japan 11) India 12) Australia 13) South Korea 14) Brazil 15) Mexico 16) Argentina 17) South Africa 18) Saudi Arabia 19) UAE |

Urban Air Mobility Market Report Segmentation Analysis

The global Urban Air Mobility Market industry analysis is segmented by Vehicle Type, by Range, by Operation, by End User, and by region.

The Air Ambulance segment accounted for the largest market share in the global Urban Air Mobility Market

By Vehicle Type, the market is segmented into Air Taxis, Air Metros, Air Ambulance, Last-Mile Delivery, and Others. The Air Ambulance segment accounted for the largest market share, around 48.3%, in the global urban air mobility market. The dominance of this segment is driven by the increasing demand for rapid emergency medical response solutions, particularly in congested urban environments where ground ambulances face traffic delays. Air ambulances, utilizing eVTOL aircraft, are revolutionizing critical care by significantly reducing response time and facilitating quicker transport of patients, organs, and medical supplies. This capability is vital in densely populated metropolitan areas and remote or inaccessible zones where conventional medical transport is limited.

The Autonomous segment holds a major share in the Urban Air Mobility Market

By Operation, the market is segmented into Piloted, Autonomous, and Hybrid. The Autonomous segment holds the major share in the global UAM market. This segment is gaining momentum due to rapid advancements in AI, machine learning, and autonomous navigation technologies. The deployment of autonomous eVTOL aircraft can significantly reduce operational costs by eliminating the need for pilots, enhancing route flexibility, and allowing for 24/7 operations without human fatigue. The integration of unmanned traffic management (UTM) systems, combined with growing regulatory support for autonomous aviation, is making fully autonomous UAM a more achievable reality.

Ridesharing Companies end-user segment dominating in the Urban Air Mobility Market

By End User, the market is segmented into Ridesharing Companies, Scheduled Operators, E-Commerce Companies, Hospitals and Medical Agencies, and Private Operators. In 2025, the Ridesharing Companies segment will dominate the global urban air mobility market by end user. This dominance is fueled by major mobility service providers such as Uber, Lyft, and their global counterparts entering the aerial mobility space to diversify their offerings and solve last-mile and mid-range transportation challenges. Ridesharing companies have the infrastructure, user base, and logistics capabilities to integrate air taxis and other UAM services into existing multimodal mobility platforms.

The following segments are part of an in-depth analysis of the global Urban Air Mobility Market:

|

Market Segments |

|

|

By Vehicle Type |

● Air Taxis ● Air Metros ● Air Ambulance ● Last-Mile Delivery ● Others |

|

By Range |

● Intercity ● Intracity |

|

By Operation |

● Piloted ● Autonomous ● Hybrid |

|

By End User |

● Ridesharing Companies ● Scheduled Operators ● E-Commerce Companies ● Hospitals and Medical Agencies ● Private Operators |

Urban Air Mobility Market Share Analysis by Region

The North America Urban Air Mobility (UAM) Market region is projected to hold the largest share of the global urban air mobility market over the forecast period

North America UAM Market accounted for the largest share of 46.2% in the global urban air mobility (UAM) market and is expected to maintain its dominance throughout the forecast period. The region’s leadership is primarily attributed to robust government initiatives, strong technological infrastructure, and early adoption of electric vertical take-off and landing (eVTOL) aircraft for commercial and medical applications. The presence of major UAM players such as Joby Aviation, Archer Aviation, and Wisk Aero, along with support from regulatory bodies like the FAA, has accelerated the pace of innovation, certification, and pilot testing in the U.S. and Canada. In addition, high urban congestion, the demand for efficient intra-city travel, and growing investments from ridesharing and aerospace companies are driving rapid growth in the North American UAM market. Public-private partnerships, increased venture capital funding, and city-level airspace planning are all contributing to a favorable ecosystem for urban air mobility development. The region is also actively developing urban air infrastructure such as vertiports, autonomous navigation systems, and air traffic management solutions to support the commercialization of UAM services.

In contrast, the Asia Pacific UAM market is projected to register the highest CAGR during the forecast period, driven by rapid urbanization, expanding megacities, and increasing infrastructure investments in countries like China, South Korea, and Japan. Government-backed smart city initiatives, combined with technological advancements and strong interest from both domestic and international players, are positioning Asia Pacific as a high-growth region for urban air mobility solutions.

Urban Air Mobility Market Competition Landscape Analysis

The market is competitive, with several established players and new entrants offering a range of Urban air mobility solutions. Some of the key players operating in the market include Guangzhou EHang Intelligent Technology Co. Ltd., Airbus, Lilium GmbH, Joby Aero, Inc., and Embraer Group, among others.

Global Urban Air Mobility Market Recent Developments News:

- In June 2024: Lilium GmbH partnered with Bao’an District to develop high-end eVTOL infrastructure in China’s Greater Bay Area, leveraging local regulatory and industry expertise. This collaboration positions Lilium as a key player in Asia-Pacific’s advanced air mobility (AAM) sector, with plans for nationwide and regional expansion.

- In June 2024: Guangzhou EHang Intelligent Technology completed the first autonomous flight of its EH216-S eVTOL aircraft in Mecca, Saudi Arabia, partnering with Front End Limited Company. This demonstration highlights the transformative potential of pilotless urban air mobility in revolutionizing regional transportation networks.

The Global Urban Air Mobility Market is dominated by a few large companies, such as

● Airbus

● Lilium GmbH

● Guangzhou EHang Intelligent Technology Co., Ltd

● Eve Holding, Inc.

● Vertical Aerospace

● Textron Inc.

● Joby Aero, Inc.

● Embraer Group

● Hyundai Motor Company

● Archer Aviation Inc.

● The AIRO Group, Inc.

● Wingcopter GmbH

● BETA Technologies, Inc.

● Volocopter GmbH

● Uber Technologies, Inc.

● Safran Group

● Other Prominent Players

Frequently Asked Questions

1. Global Urban Air Mobility

Market Introduction and Market Overview

1.1.

Objectives

of the Study

1.2.

Global

Urban Air Mobility Market Scope and Market Estimation

1.2.1.

Global

Urban Air Mobility Market Overall Market Size (US$ Bn), Market CAGR (%), Market

forecast (2025 - 2033)

1.2.2.

Global

Urban Air Mobility Market Revenue Share (%) and Growth Rate (Y-o-Y) from 2021 -

2033

1.3.

Market

Segmentation

1.3.1.

Vehicle

Type of Global Urban Air Mobility Market

1.3.2.

Range

of Global Urban Air Mobility Market

1.3.3.

Operation

of Global Urban Air Mobility Market

1.3.4.

End-user

of Global Urban Air Mobility Market

1.3.5.

Region

of Global Urban Air Mobility Market

2.

Executive Summary

2.1.

Demand

Side Trends

2.2.

Key

Market Trends

2.3.

Market

Demand (US$ Bn) Analysis 2021 – 2024 and Forecast, 2025 – 2033

2.4.

Demand

and Opportunity Assessment

2.5.

Demand

Supply Scenario

2.6.

Market

Dynamics

2.6.1.

Drivers

2.6.2.

Limitations

2.6.3.

Opportunities

2.6.4.

Impact

Analysis of Drivers and Restraints

2.7. Emerging Trends for Urban

Air Mobility Market

2.8. Porter’s Five Forces

Analysis

2.9. PEST Analysis

2.10. Key Regulation

3. Global

Urban Air Mobility Market Estimates

& Historical Trend Analysis (2021 - 2024)

4.

Global Urban Air Mobility

Market Estimates & Forecast Trend

Analysis, by Vehicle Type

4.1.

Global

Urban Air Mobility Market Revenue (US$ Bn) Estimates and Forecasts, by Vehicle

Type, 2021 - 2033

4.1.1.

Air

Taxis

4.1.2.

Air

Metros

4.1.3.

Air

Ambulance

4.1.4.

Last-Mile

Delivery

4.1.5.

Others

5.

Global Urban Air Mobility

Market Estimates & Forecast Trend

Analysis, by Range

5.1.

Global

Urban Air Mobility Market Revenue (US$ Bn) Estimates and Forecasts, by Range,

2021 - 2033

5.1.1.

Intercity

5.1.2.

Intracity

6.

Global Urban Air Mobility

Market Estimates & Forecast Trend

Analysis, by Operation

6.1.

Global

Urban Air Mobility Market Revenue (US$ Bn) Estimates and Forecasts, by Operation,

2021 - 2033

6.1.1.

Piloted

6.1.2.

Autonomous

6.1.3.

Hybrid

7.

Global Urban Air Mobility

Market Estimates & Forecast Trend

Analysis, by End-user

7.1.

Global

Urban Air Mobility Market Revenue (US$ Bn) Estimates and Forecasts, by End-user,

2021 - 2033

7.1.1.

Ridesharing

Companies

7.1.2.

Scheduled

Operators

7.1.3.

E-Commerce

Companies

7.1.4.

Hospitals

and Medical Agencies

7.1.5.

Private

Operators

8. Global

Urban Air Mobility Market Estimates

& Forecast Trend Analysis, by region

1.1.

Global

Urban Air Mobility Market Revenue (US$ Bn) Estimates and Forecasts, by region,

2021 - 2033

1.1.1.

North

America

1.1.2.

Europe

1.1.3.

Asia

Pacific

1.1.4.

Middle

East & Africa

1.1.5.

Latin

America

9. North America Urban

Air Mobility Market: Estimates &

Forecast Trend Analysis

9.1. North America Urban Air

Mobility Market Assessments & Key Findings

9.1.1.

North

America Urban Air Mobility Market Introduction

9.1.2.

North

America Urban Air Mobility Market Size Estimates and Forecast (US$ Billion) (2021

- 2033)

9.1.2.1.

By Vehicle Type

9.1.2.2.

By Range

9.1.2.3.

By Operation

9.1.2.4.

By End-user

9.1.2.5. By Country

9.1.2.5.1. The U.S.

9.1.2.5.2. Canada

10. Europe Urban

Air Mobility Market: Estimates &

Forecast Trend Analysis

10.1. Europe Urban Air Mobility

Market Assessments & Key Findings

10.1.1. Europe Urban Air Mobility

Market Introduction

10.1.2. Europe Urban Air Mobility

Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

10.1.2.1.

By Vehicle Type

10.1.2.2.

By Range

10.1.2.3.

By Operation

10.1.2.4.

By End-user

10.1.2.5.

By

Country

10.1.2.5.1.

Germany

10.1.2.5.2.

Italy

10.1.2.5.3.

U.K.

10.1.2.5.4.

France

10.1.2.5.5.

Spain

10.1.2.5.6.

Switzerland

10.1.2.5.7. Rest

of Europe

11. Asia Pacific Urban

Air Mobility Market: Estimates &

Forecast Trend Analysis

11.1. Asia Pacific Market

Assessments & Key Findings

11.1.1.

Asia

Pacific Urban Air Mobility Market Introduction

11.1.2.

Asia

Pacific Urban Air Mobility Market Size Estimates and Forecast (US$ Billion) (2021

- 2033)

11.1.2.1.

By Vehicle Type

11.1.2.2.

By Range

11.1.2.3.

By Operation

11.1.2.4.

By End-user

11.1.2.5. By Country

11.1.2.5.1. China

11.1.2.5.2. Japan

11.1.2.5.3. India

11.1.2.5.4. Australia

11.1.2.5.5. South Korea

11.1.2.5.6. Rest of Asia Pacific

12. Middle East & Africa Urban

Air Mobility Market: Estimates &

Forecast Trend Analysis

12.1. Middle East & Africa

Market Assessments & Key Findings

12.1.1. Middle

East & Africa

Urban Air Mobility Market Introduction

12.1.2. Middle

East & Africa

Urban Air Mobility Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

12.1.2.1.

By Vehicle Type

12.1.2.2.

By Range

12.1.2.3.

By Operation

12.1.2.4.

By End-user

12.1.2.5. By Country

12.1.2.5.1. South

Africa

12.1.2.5.2. UAE

12.1.2.5.3. Saudi

Arabia

12.1.2.5.4. Rest

of MEA

13. Latin America

Urban Air Mobility Market: Estimates

& Forecast Trend Analysis

13.1. Latin America Market

Assessments & Key Findings

13.1.1. Latin America Urban Air

Mobility Market Introduction

13.1.2. Latin America Urban Air

Mobility Market Size Estimates and Forecast (US$ Billion) (2021 - 2033)

13.1.2.1.

By Vehicle Type

13.1.2.2.

By Range

13.1.2.3.

By Operation

13.1.2.4.

By End-user

13.1.2.5. By Country

13.1.2.5.1. Brazil

13.1.2.5.2. Mexico

13.1.2.5.3. Argentina

13.1.2.5.4. Rest

of LATAM

14.

Country

Wise Market: Introduction

15.

Competition

Landscape

15.1. Global Urban Air Mobility

Market Product Mapping

15.2. Global Urban Air Mobility

Market Concentration Analysis, by Leading Players / Innovators / Emerging

Players / New Entrants

15.3. Global Urban Air Mobility

Market Tier Structure Analysis

15.4. Global Urban Air Mobility

Market Concentration & Company Market Shares (%) Analysis, 2023

16.

Company

Profiles

16.1.

Airbus

16.1.1.

Company

Overview & Key Stats

16.1.2.

Financial

Performance & KPIs

16.1.3.

Product

Portfolio

16.1.4.

SWOT

Analysis

16.1.5.

Business

Strategy & Recent Developments

*

Similar details would be provided for all the players mentioned below

16.2.

Lilium GmbH

16.3.

Guangzhou EHang Intelligent Technology Co. Ltd

16.4.

Eve Holding, Inc.

16.5.

Vertical Aerospace

16.6.

Textron Inc.

16.7.

Joby Aero, Inc.

16.8.

Embraer Group

16.9.

Hyundai Motor Company

16.10.

Archer Aviation Inc.

16.11.

The AIRO Group, Inc.

16.12.

Wingcopter GmbH

16.13.

BETA Technologies, Inc.

16.14.

Volocopter GmbH

16.15.

Uber Technologies, Inc.

16.16.

Safran Group

16.17.

Other Prominent Players

17. Research

Methodology

17.1. External Transportations /

Databases

17.2. Internal Proprietary

Database

17.3. Primary Research

17.4. Secondary Research

17.5. Assumptions

17.6. Limitations

17.7. Report FAQs

18. Research

Findings & Conclusion

Our Research Methodology

"Insight without rigor is just noise."

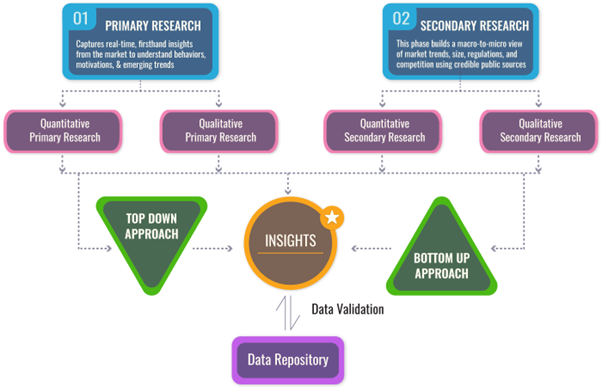

We follow a comprehensive, multi-phase research framework designed to deliver accurate, strategic, and decision-ready intelligence. Our process integrates primary and secondary research , both quantitative and qualitative , along with dual modeling techniques ( top-down and bottom-up) and a final layer of validation through our proprietary in-house repository.

PRIMARY RESEARCH

Primary research captures real-time, firsthand insights from the market to understand behaviors, motivations, and emerging trends.

1. Quantitative Primary Research

Objective: Generate statistically significant data directly from market participants.

Approaches:- Structured surveys with customers, distributors, and field agents

- Mobile-based data collection for point-of-sale audits and usage behavior

- Phone-based interviews (CATI) for market sizing and product feedback

- Online polling around industry events and digital campaigns

- Purchase frequency by customer type

- Channel performance across geographies

- Feature demand by application or demographic

2. Qualitative Primary Research

Objective: Explore decision-making drivers, pain points, and market readiness.

Approaches:- In-depth interviews (IDIs) with executives, product managers, and key decision-makers

- Focus groups among end users and early adopters

- Site visits and observational research for consumer products

- Informal field-level discussions for regional and cultural nuances

SECONDARY RESEARCH

This phase helps establish a macro-to-micro understanding of market trends, size, regulation, and competitive dynamics, sourced from credible and public domain information.

1. Quantitative Secondary Research

Objective: Model market value and segment-level forecasts based on published data.

Sources include:- Financial reports and investor summaries

- Government trade data, customs records, and regulatory statistics

- Industry association publications and economic databases

- Channel performance and pricing data from marketplace listings

- Revenue splits, pricing trends, and CAGR estimates

- Supply-side capacity and volume tracking

- Investment analysis and funding benchmarks

2. Qualitative Secondary Research

Objective: Capture strategic direction, innovation signals, and behavioral trends.

Sources include:- Company announcements, roadmaps, and product pipelines

- Publicly available whitepapers, conference abstracts, and academic research

- Regulatory body publications and policy briefs

- Social and media sentiment scanning for early-stage shifts

- Strategic shifts in market positioning

- Unmet needs and white spaces

- Regulatory triggers and compliance impact

DUAL MODELING: TOP-DOWN + BOTTOM-UP

To ensure robust market estimation, we apply two complementary sizing approaches:

Top-Down Modeling:- Start with broader industry value (e.g., global or regional TAM)

- Apply filters by segment, geography, end-user, or use case

- Adjust with primary insights and validation benchmarks

- Ideal for investor-grade market scans and opportunity mapping

- Aggregate from the ground up using sales volumes, pricing, and unit economics

- Use internal modeling templates aligned with stakeholder data

- Incorporate distributor-level or region-specific inputs

- Most accurate for emerging segments and granular sub-markets

DATA VALIDATION: IN-HOUSE REPOSITORY

We close the loop with proprietary data intelligence built from ongoing projects, industry monitoring, and historical benchmarking. This repository includes:

- Multi-sector market and pricing models

- Key trendlines from past interviews and forecasts

- Benchmarked adoption rates, churn patterns, and ROI indicators

- Industry-specific deviation flags and cross-check logic

- Catches inconsistencies early

- Aligns projections across studies

- Enables consistent, high-trust deliverables